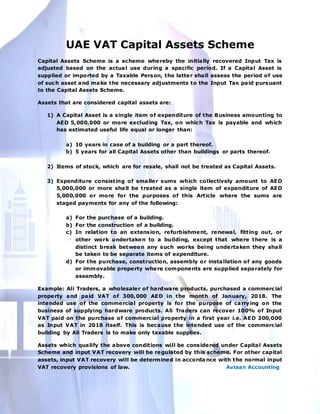

The UAE VAT Capital Assets Scheme allows for the adjustment of initially recovered input tax based on the actual use of capital assets over a specific period. A capital asset is defined as an expenditure of AED 5,000,000 or more with an estimated useful life of at least 10 years for buildings or 5 years for other assets, with exceptions for stock and smaller expenditures. Input VAT recovery for qualifying assets is governed by this scheme, while other assets are subject to standard input VAT recovery rules.

![Tax guide-2012[1]](https://cdn.slidesharecdn.com/ss_thumbnails/tax-guide-20121-130314215142-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)