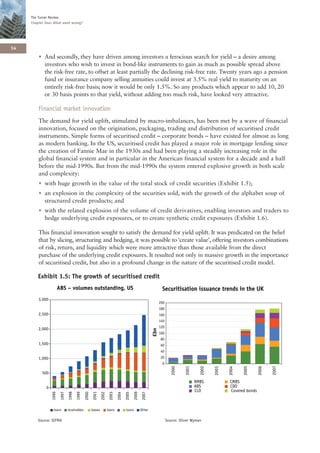

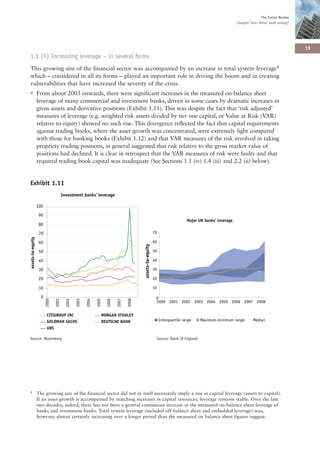

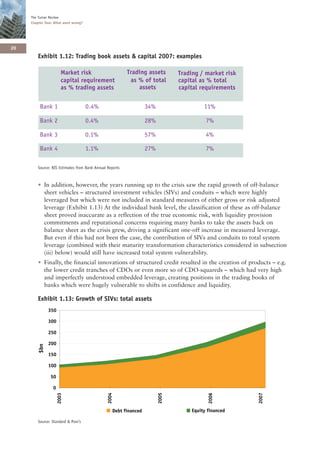

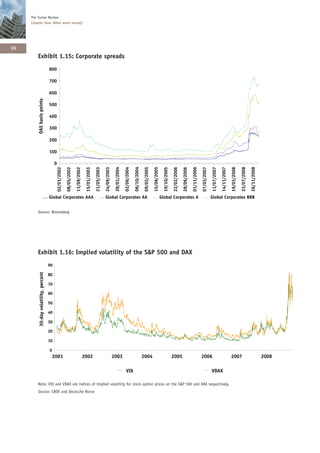

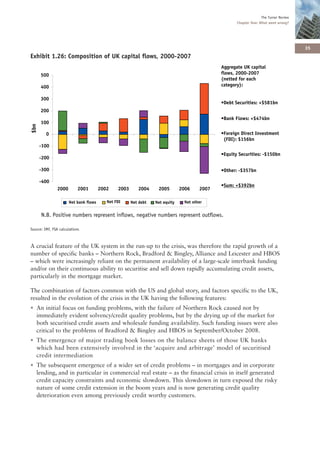

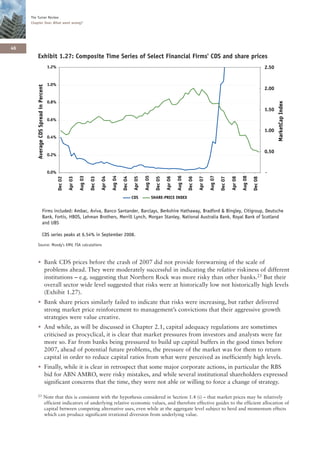

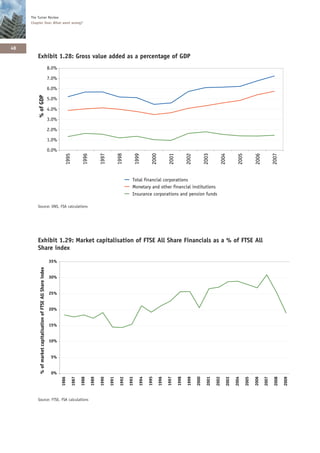

Downloaded 23 times

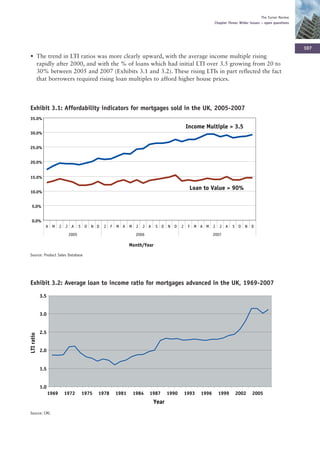

This document summarizes the key findings and recommendations from The Turner Review, which analyzes the causes of the global banking crisis that began in 2008 and proposes reforms to create a more stable banking system. The review finds that macroeconomic trends, financial innovation, excessive leverage, procyclicality, and misplaced reliance on mathematical models all contributed to the crisis. It recommends fundamental changes like increasing and improving bank capital requirements, implementing countercyclical policies, expanding regulatory coverage, and enhancing supervision, regulation and risk management. The review argues these reforms are necessary to reduce the probability and severity of future financial crises.

![! [Day] ppt_fi governance changes_prmia_april 18 2011](https://cdn.slidesharecdn.com/ss_thumbnails/daypptfigovernancechangesprmiaapril182011-110505132100-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Banks less safe with contingency plans [really]](https://cdn.slidesharecdn.com/ss_thumbnails/bankslesssafewithcontingencyplansreally-110412132931-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![The Financial Crisis Impact On Risk Management [Tom Day] Handouts](https://cdn.slidesharecdn.com/ss_thumbnails/thefinancialcrisisimpactonriskmanagementtomdayhandouts-12925434893975-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)