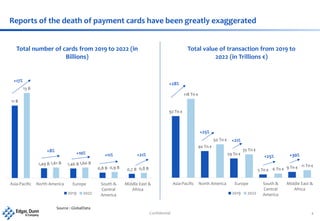

The document presents insights on the evolving global payment landscape, highlighting key trends such as the rise of digital commerce, retail innovation, and the influence of fintech on traditional banks. It discusses the significant growth projections for payment cards and transaction values across regions from 2019 to 2022. Additionally, it emphasizes the importance of customer experience and regulation in shaping payment security and innovation.