Top Ten GCC Banks

•

1 like•314 views

- The top 10 GCC banks have demonstrated strong growth over the past year, with total assets growing 16% to $743 billion. QNB Group from Qatar was the fastest growing at 30%. - GCC banks have been largely insulated from turmoil in emerging markets due to strong economic fundamentals in the region from hydrocarbon exports and government spending. - The report predicts continued strong performance from leading GCC banks due to high oil prices, economic growth, large infrastructure projects, and support for the banking system.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Top Ten GCC Banks

Similar to Top Ten GCC Banks (20)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

Top Ten GCC Banks

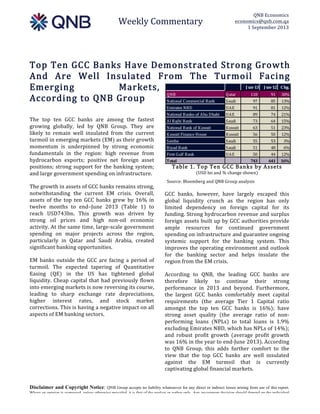

- 1. Weekly Commentary QNB Economics economics@qnb.com.qa 1 September 2013 Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a complimentary basis. It may not be reproduced in whole or in part without permission from QNB Group. J un-‐13 J un-‐12 Chg. QNB Qatar 118 91 30% National Commercial Bank Saudi 97 85 13% Emirates NBD UAE 91 81 12% National Banko of Abu Dhabi UAE 89 74 21% Al Rajhi Bank Saudi 73 64 15% National Bank of Kuwait Kuwait 63 51 23% Kuwait Finance House Kuwait 56 50 12% Samba Saudi 55 53 3% Riyad Bank Saudi 51 48 6% First Gulf Bank UAE 50 44 12% Total 743 641 16% Top Ten GCC Banks Have Demonstrated Strong Growth And Are Well Insulated From The Turmoil Facing Emerging Markets, According to QNB Group The top ten GCC banks are among the fastest growing globally, led by QNB Group. They are likely to remain well insulated from the current turmoil in emerging markets (EM) as their growth momentum is underpinned by strong economic fundamentals in the region: high revenue from hydrocarbon exports; positive net foreign asset positions; strong support for the banking system; and large government spending on infrastructure. The growth in assets of GCC banks remains strong, notwithstanding the current EM crisis. Overall, assets of the top ten GCC banks grew by 16% in twelve months to end–June 2013 (Table 1) to reach USD743bn. This growth was driven by strong oil prices and high non-‐oil economic activity. At the same time, large-‐scale government spending on major projects across the region, particularly in Qatar and Saudi Arabia, created significant banking opportunities. EM banks outside the GCC are facing a period of turmoil. The expected tapering of Quantitative Easing (QE) in the US has tightened global liquidity. Cheap capital that had previously flown into emerging markets is now reversing its course, leading to sharp exchange rate depreciations, higher interest rates, and stock market corrections. This is having a negative impact on all aspects of EM banking sectors. Table 1. Top Ten GCC Banks by Assets (USD bn and % change shown) Source: Bloomberg and QNB Group analysis GCC banks, however, have largely escaped this global liquidity crunch as the region has only limited dependency on foreign capital for its funding. Strong hydrocarbon revenue and surplus foreign assets built up by GCC authorities provide ample resources for continued government spending on infrastructure and guarantee ongoing systemic support for the banking system. This improves the operating environment and outlook for the banking sector and helps insulate the region from the EM crisis. According to QNB, the leading GCC banks are therefore likely to continue their strong performance in 2013 and beyond. Furthermore, the largest GCC banks comfortably meet capital requirements (the average Tier 1 Capital ratio amongst the top ten GCC banks is 16%); have strong asset quality (the average ratio of non-‐ performing loans (NPLs) to total loans is 1.9% excluding Emirates NBD, which has NPLs of 14%); and robust profit growth (average profit growth was 16% in the year to end-‐June 2013). According to QNB Group, this adds further comfort to the view that the top GCC banks are well insulated against the EM turmoil that is currently captivating global financial markets.

- 2. Weekly Commentary QNB Economics economics@qnb.com.qa 1 September 2013 Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a complimentary basis. It may not be reproduced in whole or in part without permission from QNB Group. QNB Group, the largest GCC bank by assets, is the only Qatari bank in the top ten list and was the fastest growing bank with total assets expanding by 30% in the 12 months to end-‐June 2013. This asset growth was driven by the strategic acquisition of NSGB in Egypt, and higher international stakes. At the end of 2012, 79% of QNB’s assets were in Qatar. Therefore, strong growth in Qatar’s economy (forecast to be 6.5% in 2013) has also supported growth in QNB Group’s assets. Growth is expected to accelerate as the government rolls out its large infrastructure investment program in time to meet requirements for the 2022 World Cup. With a strong net foreign asset position (high and rising international reserves and a large sovereign wealth fund) and high hydrocarbon revenue, Qatar is well insulated from capital flight risks faced by other emerging markets. This will enable it to comfortably roll out its infrastructure development plan, supporting the economy and the banking sector. Qatar’s economic growth and project pipeline presents major opportunities for QNB and the wider banking sector to boost growth of domestic credit and investment as well as profits. Profits of Qatari banks are rising along with assets; reaching USD2.4bn in the first half of 2013, 9% higher than the same period in 2012. This equates to high returns of 2.4% on average assets and 15.2% on average equity. This is being achieved while asset quality remains high across the banking sector: NPLs were as low as 1.7% of total loans at end-‐ 2012. They have been kept down by strong government support: the government stepped in to purchase bad real estate loans and equity portfolios from banks in the aftermath of the 2008-‐09 financial crisis. Additionally, banks are well capitalized with Tier 1 capital at 18% of risk weighted assets at end-‐2012. A total of 4 of the banks in the GCC top ten are from Saudi Arabia. Assets at these banks have grown 10% in the 12 months to end-‐June 2013. This was driven by both corporate and retail loan growth. On the corporate side, high oil production and prices has boosted revenue, supporting government spending on major infrastructure projects. More recently, USD22bn of contracts were awarded in July for the Riyadh Metro. Such projects have provided banks with considerable financing opportunities, driving asset growth. Retail loan growth has been propelled by the new and fast-‐growing mortgage loan sector. The current program of project spending totals USD500bn, including large-‐scale housing construction, which will continue to support lending, mortgages and asset growth going forward. Again, hydrocarbon revenue and an extremely strong net foreign asset position provide ample resources for the Saudi authorities to meet spending plans, supporting the economy and the banking sector. Further insulating the banking sector, the top Saudi banks are highly capitalized (average Tier 1 capital ratio of 17%) with low NPLs (1.5% of total loans on average) and strong profit growth (8.2%). The low interest rate environment, strong competition and high liquidity has compressed net interest margins. However, non-‐interest income has supported profit growth, such as fee income from credit expansion, off-‐balance-‐sheet items and a surge in trading on the Tadawul stock exchange. The 3 UAE banks in the GCC top ten witnessed a sharp pickup in activity over the last year, especially in the real estate and services sector in Dubai. Profits at the largest UAE bank, Emirates NBD (Dubai), grew 40% in the first half of 2013 compared with the first half of 2012. However, return on average equity remains low (8.2%) as the bank continues to suffer from high NPLs (14%), the legacy of Dubai’s real estate debt crisis in 2009. A number of the other banks in Dubai face similar issues to Emirates NBD. At the end of 2012, Moody’s downgraded 4 Dubai-‐based banks (Emirates NBD, Mashreqbank, Commercial Bank of Dubai and Dubai Islamic Bank) owing to elevated NPLs (15%-‐17%) and low provisioning for bad loans, despite improvements in the Dubai operating environment. The largest Abu Dhabi-‐ based banks, National Bank of Abu Dhabi and First Gulf Bank, have already returned to high

- 3. Weekly Commentary QNB Economics economics@qnb.com.qa 1 September 2013 Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a complimentary basis. It may not be reproduced in whole or in part without permission from QNB Group. profitability (return on average equity around 16%) as they were less exposed to the crash in the Dubai real estate market and benefited from stronger state support. The UAE banking system has a strong track record of systemic support, most recently during the last financial crisis when liquidity and capital facilities were provided to distressed banks. Such implicit guarantees help protect the banking system from capital flight risks. The 2 Kuwaiti banks in the top ten list have performed strongly with asset growth of 17% in the 12 months to end-‐June 2013. The asset growth was mainly driven by National Bank of Kuwait. Corporate lending has accelerated as the government’s USD110bn development plan has gathered pace. However, in Kuwait, consumer loan growth has been particularly strong, driven by public sector wage increases and transfers. Oil revenue and a strong net foreign asset position should ensure continued support to the economy and banking sector in Kuwait, mainly through government wages and transfers and to a lesser extent on government spending. The ongoing deleveraging in nonbank financial institutions will continue to hold back growth in the banking sector as credit to these institutions shrinks. Overall, the GCC provides a strong macroeconomic operating environment for the banking sector to flourish. High hydrocarbon prices support revenue streams for project spending and surplus foreign assets. This should continue to support lending and asset growth for the top GCC banks, according to QNB Group, and is likely to keep the GCC well insulated from the turmoil gripping EM banking sectors.