Monthly Economic Monitoring of Ukraine No 231, April 2024

Ample GCC Liquidity Will Continue to Finance Growth

1. QNB Economics

economics@qnb.com.qa

23 June 2013

Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report.

Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend on the individual

circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a complimentary basis. It may not be

reproduced in whole or in part without permission from QNB Group.

1

Ample GCC Liquidity Will Continue to Finance Growth,

According to QNB

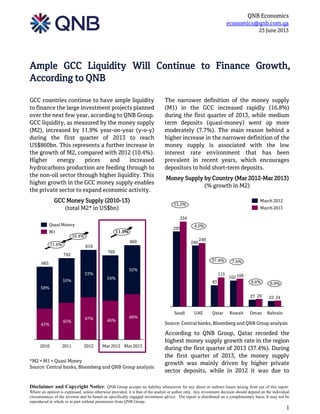

GCC countries continue to have ample liquidity

to finance the large investment projects planned

over the next few year, according to QNB Group.

GCC liquidity, as measured by the money supply

(M2), increased by 11.9% year-on-year (y-o-y)

during the first quarter of 2013 to reach

US$860bn. This represents a further increase in

the growth of M2, compared with 2012 (10.4%).

Higher energy prices and increased

hydrocarbons production are feeding through to

the non-oil sector through higher liquidity. This

higher growth in the GCC money supply enables

the private sector to expand economic activity.

GCC Money Supply (2010-13)

(total M2* in US$bn)

*M2 = M1 + Quasi Money

Source: Central banks, Bloomberg and QNB Group analysis

The narrower definition of the money supply

(M1) in the GCC increased rapidly (16.8%)

during the first quarter of 2013, while medium

term deposits (quasi-money) went up more

moderately (7.7%). The main reason behind a

higher increase in the narrower definition of the

money supply is associated with the low

interest rate environment that has been

prevalent in recent years, which encourages

depositors to hold short-term deposits.

Money Supply by Country (Mar 2012-Mar 2013)

(% growth in M2)

Source: Central banks, Bloomberg and QNB Group analysis

According to QNB Group, Qatar recorded the

highest money supply growth rate in the region

during the first quarter of 2013 (37.4%). During

the first quarter of 2013, the money supply

growth was mainly driven by higher private

sector deposits, while in 2012 it was due to

11.6%

11.9%

10.4%

58%

42%

819

2012

53%

47%

742

2011

46%

48%

54%

769

Mar 2013

52%

Mar 2012

860

55%

45%

2010

665

M1

Quasi Money

2227

102

83

240

295

2429

109115

249

334

Kuwait

37.4%

4.0%

6.9%9.6%

7.6%

13.2%

BahrainOmanQatarUAESaudi

March 2013

March 2012

2. QNB Economics

economics@qnb.com.qa

23 June 2013

foreign currency deposits from the public sector.

According to QNB Group, this reflects a

significant shift in trend, compared with the

traditional source of money supply growth in

Qatar, which may indicate a higher growth

contribution from the non-oil sector.

According to QNB Group, Saudi Arabia has the

largest money supply in the region. Broad

money (M2) expanded by 13.4% y-o-y in the

Kingdom, reflecting a significant increase in

demand deposits (18.9%). Saudi Arabia has a

different money supply make up as compared to

other GCC countries, with a predominance of

short-term deposits. As a result, the narrower

definition of the money supply (M1) accounts

for three quarters of broad money.

Money Supply growth in the UAE witnessed a

major recovery in the first quarter of 2013.

Broad money (M2) grew by 4.0% during the first

quarter of 2013. This recovery can be attributed

to the significant pick up in real estate activity

in recent months and the overall gain in

investor confidence.

Investment projects planned or currently

underway in the GCC are estimated by the

Middle East Economic Digest (MEED) at

US$2.2trn. With huge project financing needs

coming up over the next decade, GCC countries

will need to further supplement overall bank

liquidity with additional sources of funding. The

corporate debt markets have emerged as a good

funding option in recent years. During the year

up to June 2013, debt issuance in the GCC region

reached a record level of US$34.6bn, compared

to US$36.6bn for the full year 2012, according to

data from Bloomberg. The GCC countries have

also started developing their own domestic debt

capital markets as in Qatar.

According to QNB Group, these financial

developments will widen the overall funding

sources for GCC countries to finance non-oil

growth, even as domestic banks provide a core

source of funding, while reducing the

dependence on foreign financing going forward.