Download to read offline

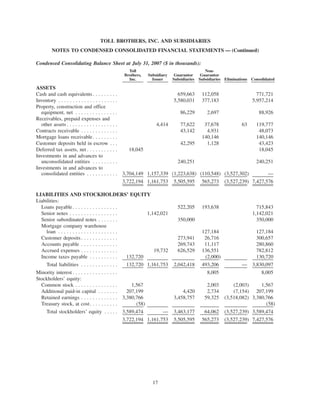

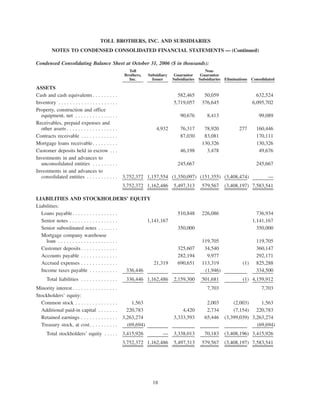

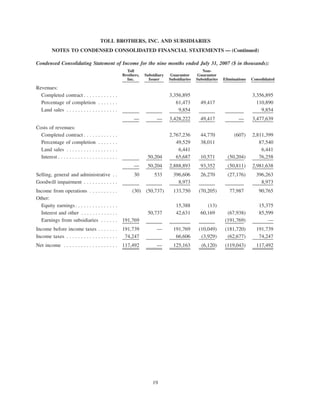

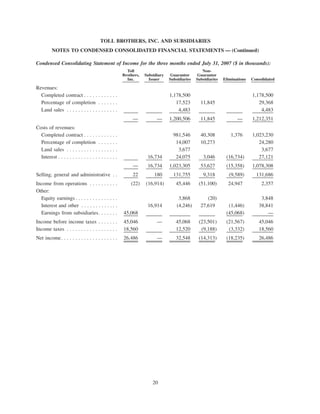

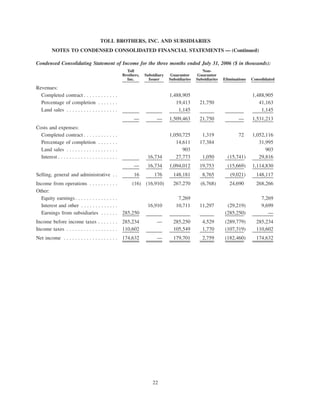

This document is Toll Brothers Inc.'s quarterly report filed with the SEC for the quarter ended July 31, 2007. It includes: - Condensed consolidated balance sheets showing the company's assets (including $5.96 billion in inventory), liabilities (including $3.83 billion in total liabilities), and stockholders' equity as of July 31, 2007 and October 31, 2006. - Notes to the condensed consolidated financial statements providing additional information about the company's accounting policies, commitments and contingencies, stock-based compensation, and earnings per share calculations. - Management's discussion and analysis of the company's financial condition and results of operations for the quarter, including information on revenues, operating