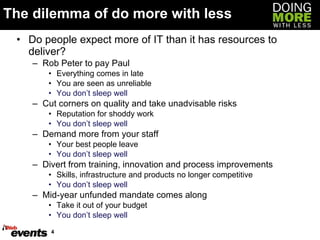

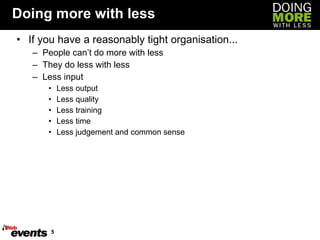

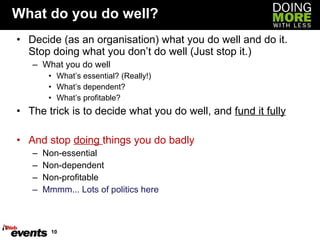

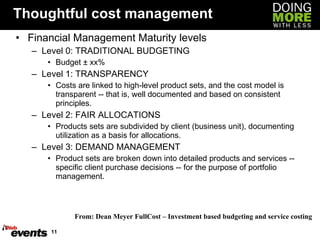

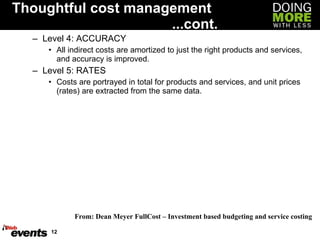

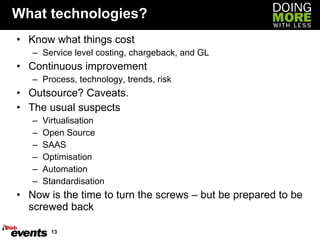

The document discusses the dilemma organizations face when asked to "do more with less". It argues that cutting costs indiscriminately through across-the-board reductions will lead to doing less with less, lower quality work, and set the organization up for random failures. Instead, it recommends organizations thoughtfully decide what few things they do well and fund those fully, while stopping activities they do poorly. The document also advises treating the IT budget as a prepaid account for business units to draw from based on their needs, rather than viewing IT departments as cost centers.

![Cut the outputs not the inputs In summary People do less with less Across the board cuts set the organisation up for random failure Decide what you do well and do it. Stop doing what you don’t do well Exercise thoughtful cost management Know what “services” cost and where they contribute Your budget is a pre-paid account [email_address]](https://image.slidesharecdn.com/terrywhite-12815279537248-phpapp01/85/Terry-White-15-320.jpg)