Tax code dec_6_2010

•

0 likes•507 views

The newly approved Tax Code in Ukraine is set to gradually lower the corporate tax rate from 25% to 16% by 2014 and cut the VAT rate to 17% in 2014. It also grants tax exemptions to various industries. While benefiting large businesses, it may negatively impact small private entrepreneurs. The Tax Code approval facilitates drafting of the 2011 budget in line with IMF requirements and bodes well for endorsement of other IMF-backed reforms. The overall impact on the economy is expected to be neutral to positive, with gains for large companies offsetting effects on small businesses. Budget revenue impacts are seen as insignificant.

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (20)

Similar to Tax code dec_6_2010

Similar to Tax code dec_6_2010 (20)

More from Yaroslav Vedmid

More from Yaroslav Vedmid (19)

Tax code dec_6_2010

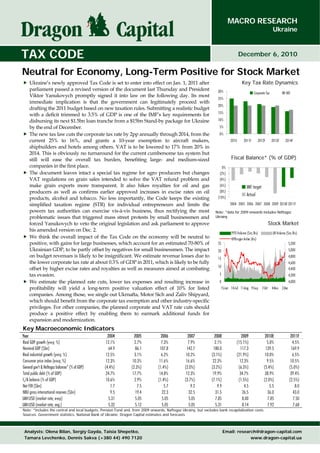

- 1. MACRO RESEARCH Ukraine TAX CODE December 6, 2010 Neutral for Economy, Long-Term Positive for Stock Market Ukraine’s newly approved Tax Code is set to enter into effect on Jan. 1, 2011 after Key Tax Rate Dynamics parliament passed a revised version of the document last Thursday and President 30% Corporate Tax VAT Viktor Yanukovych promptly signed it into law on the following day. Its most 25% immediate implication is that the government can legitimately proceed with 20% drafting the 2011 budget based on new taxation rules. Submitting a realistic budget with a deficit trimmed to 3.5% of GDP is one of the IMF’s key requirements for 15% disbursing its next $1.5bn loan tranche from a $15bn Stand-by package for Ukraine 10% by the end of December. 5% The new tax law cuts the corporate tax rate by 2pp annually through 2014, from the 0% current 25% to 16%, and grants a 10-year exemption to aircraft makers, 2010 2011F 2012F 2013F 2014F shipbuilders and hotels among others. VAT is to be lowered to 17% from 20% in 2014. This is obviously no turnaround for the current cumbersome tax system but still will ease the overall tax burden, benefiting large- and medium-sized Fiscal Balance* (% of GDP) companies in the first place. 0% The document leaves intact a special tax regime for agro producers but changes (2%) VAT regulations on grain sales intended to solve the VAT refund problem and (4%) make grain exports more transparent. It also hikes royalties for oil and gas (6%) IMF target producers as well as confirms earlier approved increases in excise rates on oil (8%) (10%) Actual products, alcohol and tobacco. No less importantly, the Code keeps the existing simplified taxation regime (STR) for individual entrepreneurs and limits the 2004 2005 2006 2007 2008 2009 2010E 2011F powers tax authorities can exercise vis-à-vis business, thus rectifying the most Note: *data for 2009 onwards includes Naftogaz problematic issues that triggered mass street protests by small businessmen and Ukrainy forced Yanukovych to veto the original legislation and ask parliament to approve Stock Market his amended version on Dec. 2. PFTS Volume ($m; lhs) UX Volume ($m; lhs) We think the overall impact of the Tax Code on the economy will be neutral to KP-Dragon Index (rhs) positive, with gains for large businesses, which account for an estimated 70-80% of 25 5,200 Ukrainian GDP, to be partly offset by negatives for small businessmen. The impact 20 5,000 on budget revenues is likely to be insignificant. We estimate revenue losses due to 15 4,800 the lower corporate tax rate at about 0.3% of GDP in 2011, which is likely to be fully 4,600 10 offset by higher excise rates and royalties as well as measures aimed at combating 4,400 tax evasion. 5 4,200 We estimate the planned rate cuts, lower tax expenses and resulting increase in 0 4,000 profitability will yield a long-term positive valuation effect of 10% for listed 15-Jun 14-Jul 11-Aug 9-Sep 7-Oct 4-Nov 2-Dec companies. Among those, we single out Ukrnafta, Motor Sich and Zaliv Shipyard, which should benefit from the corporate tax exemption and other industry-specific privileges. For other companies, the planned corporate and VAT rate cuts should produce a positive effect by enabling them to earmark additional funds for expansion and modernization. Key Macroeconomic Indicators Year 2004 2005 2006 2007 2008 2009 2010E 2011F Real GDP growth (y-o-y; %) 12.1% 2.7% 7.3% 7.9% 2.1% (15.1%) 5.0% 4.5% Nominal GDP ($bn) 64.9 86.1 107.8 142.7 180.0 117.3 139.5 169.9 Real industrial growth (y-o-y; %) 12.5% 3.1% 6.2% 10.2% (3.1%) (21.9%) 10.0% 6.5% Consumer price index (e-o-p; %) 12.3% 10.3% 11.6% 16.6% 22.3% 12.3% 9.5% 10.5% General gov’t & Naftogaz balances* (% of GDP) (4.4%) (2.3%) (1.4%) (2.0%) (3.2%) (6.3%) (5.4%) (5.0%) Total public debt (% of GDP) 24.7% 17.7% 14.8% 12.3% 19.9% 34.7% 38.9% 39.4% C/A balance (% of GDP) 10.6% 2.9% (1.4%) (3.7%) (7.1%) (1.5%) (2.0%) (2.5%) Net FDI ($bn) 1.7 7.5 5.7 9.2 9.9 4.5 5.5 8.0 NBU gross international reserves ($bn) 9.5 19.4 22.3 32.5 31.5 26.5 36.0 43.0 UAH:USD (market rate; e-o-p) 5.31 5.05 5.05 5.05 7.85 8.00 7.85 7.50 UAH:USD (market rate; avg.) 5.32 5.12 5.05 5.05 5.31 8.14 7.92 7.68 Note: *includes the central and local budgets, Pension Fund and, from 2009 onwards, Naftogaz Ukrainy, but excludes bank recapitalization costs. Sources: Government statistics, National Bank of Ukraine, Dragon Capital estimates and forecasts Analysts: Olena Bilan, Sergiy Gayda, Taisia Shepetko, Email: research@dragon-capital.com Tamara Levchenko, Dennis Sakva (+380 44) 490 7120 www.dragon-capital.ua

- 2. December 6, 2010 TAX CODE OVERVIEW The Verkhovna Rada last Thursday approved the final version of the Tax Code Parliament approved a revised incorporating amendments submitted by President Viktor Yanukovych after he Tax Code with presidential vetoed the original document. It took Yanukovych only one day to sign the new bill amendments… into law with the official enactment date of Jan. 1, 2011. The Code keeps intact the existing simplified taxation regime (STR) for individual entrepreneurs but it is to be revised later on. The document, unlike its previous version, also limits the powers tax authorities can exercise vis-à-vis business, thus rectifying the most problematic issues that triggered mass street protests by small businessmen in the past two weeks. The most important changes introduced by the Code include: …that overhauls tax legislation • The corporate income tax rate will be reduced gradually from the current 25% to 16% in 2014, with light industry companies, hotels, aircraft producers, shipbuilders and producers of agricultural machinery to enjoy a 10-year exemption. • The VAT rate will be cut by 3pp to 17% in 2014. The Code specifies eligibility criteria for automatic VAT refunding and imposes fines on the government for delaying such refunds. • The document leaves intact a special tax regime for agricultural producers and hikes royalties for oil and gas as well as confirms earlier approved hikes in excise rates on oil products, alcohol and tobacco. • A number of minor taxes were scrapped. We summarize these and other major changes below. Tax Current status Adopted changes Corporate profit tax 25% 23% from 2011 21% from 2012 19% from 2013 16% from 2014 10-year tax holidays for the light industry, hotels, aircraft makers, shipbuilders and producers of agricultural machinery; 5-year tax holidays for small businesses and startups VAT 20% 17% from 2014; automatic VAT refunding for eligible companies; the government faces fines in case of delaying refunds; ; zero rate for agro producers and exporters (excluding trading companies) Personal income tax 15% 15% for monthly incomes below 10x minimum wage (UAH 9,220 as of Dec. 1); 17% for monthly incomes above 10x minimum wage Excise taxes on oil products No changes in Tax Code but parliament earlier approved 38-40% hikes effective 2011 Excise taxes on alcohol and tobacco No changes in Tax Code but parliament earlier approved a 7% increase effective 2011 (not applied to beer producers) Oil royalties 40% hike from 2011 Gas royalties 18.5% hike from 2011 Simplified Taxation Regime (STR) for small businesses No changes in rates and thresholds; costs of goods and services purchased from entrepreneurs using STR (except IT services) by companies subject to general taxation regime are no longer tax deductible Fixed agricultural tax, special VAT regime for agro producers* No changes Tax on interest earned on bank deposits 5% from 2015 Property tax Progressive rate ranging from 0% to 2.7% of the minimum wage per square meter applied depending on taxable property area from 2012 Tax Code: Key Changes to Existing Taxation Regime Note: *agro producers retain VAT in their bank account to use for CAPEX and production needs. Source: Verkhovna Rada Tax Code: Neutral for Economy; Long-Term Positive for Stock Market 2

- 3. December 6, 2010 IMPACT ON ECONOMY: NEUTRAL Ukraine’s current corporate and VAT rates (25% and 20% respectively) are moderate The Code cuts tax rates and by regional standards. With the rate cuts envisaged by the Code, the country will streamlines tax legislation… boast one of the lowest tax rates in Europe by 2014. This is obviously no turnaround for the current cumbersome tax system but still will ease the overall tax burden, benefiting large- and medium-sized companies in the first place. Moreover, the enactment of the Code as a systematic collection of taxation rules as well as planned abolition of a number of small taxes will also streamline the existing legislation. 40% 30% 30% 25% 20% 20% 15% 10% 10% 5% 0% 0% Czech Rep. Malta Bulgaria Romania Ukraine Austria Ukraine Hungary Russia Estonia Italy Greece UK Germany France Norway Malta Czech Rep. Denmark Switzerland Portugal Finland Ukraine Romania Austria Bulgaria Estonia Ukraine Ireland Cyprus Luxembourg Netherlands Spain UK Russia Germany Greece France Italy Hungary Sweden Belgium Switzerland Portugal Norway Denmark Finland Luxembourg Ireland Cyprus Spain Netherlands Belgium Sweden Corporate Income Tax Rates in Europe (%) VAT Rates in Europe (%) Sources: AGN International, Dragon Capital estimates In contrast to CEE peers, the Ukrainian economy is dominated by large businesses …benefiting large companies, which account for an estimated 70-80% of GDP. This implies the corporate tax which dominate the economy… reduction should produce a positive effect on the economy in the longer term by enabling companies to release additional funds for expansion and modernization. 80% 80% 0% 70% 70% (2%) 60% 60% (4%) 50% 50% (6%) 40% 40% (8%) 30% 30% 2009 2010E 2011F 20% 20% (10%) 10% 10% (12%) 0% 0% (14%) Czech Rep. Slovak Rep. Ukraine** UK Greece France Italy Germany Russia Portugal Spain Latvia Lithuania Croatia Slovenia Estonia Romania Poland Turkey Bulgaria Hungary Lithuania Slovenia Poland Croatia Estonia Czech Rep Slovak Rep Romania Latvia Ukraine* Bulgaria Turkey Hungary Share of Small and Medium-Sized Enterprises in GDP (2008; %) Fiscal Deficit: Ukraine vs. European Countries (% of GDP) Note: *unofficial estimate for Ukraine; **IMF-set ceilings for 2010 and 2011. Sources: Finance Ministry, Pension Fund, State Treasury, European Commission, Eurostat, IMF, Dragon Capital estimates Yet, the above gains may partly be offset by negative impact on private …but adversely affecting private entrepreneurs. Despite preserving the STR, the Code includes a provision that makes entrepreneurs the costs of goods and services purchased from STR businesses (except IT services) non-deductible for companies subject to the general taxation regime. While this will limit the scope for tax evasion, which the earlier arrangement allowed, it will also hampers B2B activity between large companies and private entrepreneurs. That said, we think the overall impact of the Tax Code on the economy will be The overall impact is neutral to neutral to positive, with gains for large businesses to be counterbalanced by positive, no significant effect on negatives for small businessmen. The impact on budget revenues is likely to be budget revenues insignificant. We estimate revenue losses due to the lower corporate tax rate at about 0.3% of GDP in 2011, which is likely to be fully offset by higher excise rates and royalties as well as measures aimed at limiting tax evasion. Tax Code: Neutral for Economy; Long-Term Positive for Stock Market 3

- 4. December 6, 2010 Approval of the Code paves the way for the government to proceed with drafting the Approval of the Tax Code 2011 budget based on new taxation rules. Submitting a realistic budget with a deficit brightens the prospects to trimmed to 3.5% of GDP — which is expected to be achieved primarily via spending receive the next IMF tranche… cuts — is one of the IMF’s key requirements for disbursing its next $1.5bn loan tranche by the end of December. The Fund also wants the authorities to reinstate penalties for overdue utilities payments and initiate pension reforms including many unpopular measures such as a gradual increase in the retirement age for women. On a related note, the revised Tax Code was endorsed by a solid majority of 268 …with voting results boding lawmakers, including 20 deputies from the opposition Our Ukraine and Yulia well for the endorsement of Tymoshenko Bloc factions. It is important that the bill would have secured the IMF-required pension required majority of at least 226 votes even without the 26-strong Communist faction. legislation The ruling party’s effective independence from Communists, gained recently thanks to defectors from the opposition, bodes well for the IMF-required approval of unpopular pension legislation later this month as the old-guard leftists are almost certain to reject it. IMPACT ON STOCK MARKET: POSITIVE LONG-TERM GAINS In terms of impact on individual companies, particularly large and medium-sized Long-term positive valuation businesses, the planned rate cuts, lower tax expenses and resulting increase in for stocks estimated at 10% on profitability should yield a long-term positive valuation effect of 10%, with exporters average standing to gain a marginally lower 9% as they won’t be influenced materially by the VAT reduction. We analyze the impact on selected listed companies in more detail in the next chapter. The Tax Code also introduces several changes regarding stock market operations, Dividend tax for individuals particularly taxation of dividends. Starting next year, the dividend tax for private cut to 5% individuals will be cut to 5% from 15%, with the rate paid by non-residents left unchanged at 15% and domestic corporates to continue paying the standard income tax rate. Moreover, in case dividends are paid to individuals and parent companies, the company distributing them will be exempt from income tax on such payouts (advance income tax is to be charged when dividends are paid and subtracted from the income tax balance in future periods). Although the beneficiaries of most local companies are offshore-registered corporate entities, the reduced dividend tax for individuals may serve as a long-term incentive for shareholders to increase dividend payouts, as only a handful of private companies in Ukraine presently pay dividends. The government left income earned by non-residents on government securities tax- Income on government exempt. This provision covers both pure sovereign and municipal bonds as well debt securities remains tax- with government guarantees. The same applies to Ukrainian residents purchasing exempt… government-issued/guaranteed securities on the primary or secondary markets. The Code also requires including interest accrued on purchased securities in total Delays in interest payments… taxable income for the period when such interest payment was or was expected to be made according to conditions of the appropriate security issue. This may have negative implications in case of non-timely payment of interest, leading to increased taxable income and tax expenses for the investor. Tax Code: Neutral for Economy; Long-Term Positive for Stock Market 4

- 5. December 6, 2010 According to the Tax Code, the so called “30-day rule”, when in the event of 30 …and the “30-day rule” may calendar days prior to the sale of securities or derivatives, and for the next 30 calendar overstate taxable income days after such sale, the taxpayer purchases a package of identical securities or derivatives, then investment loss that may result from such sale shall be disregarded in determining the overall financial result of operations with investment assets. The value of purchased securities for tax purposes is determined by its purchase price, but not lower than the price of the sold package. This may have negative implications in case of inability to offset incurred losses with income on identical frequently traded securities, implying additional taxable income and tax expenses. Exceptions include block trades with over 25% stakes, share buyback, and purchase of securities during a private placement. Both the abovementioned delays in interest payments and the “30- day rule” may have negative implications for local market activity but we see agreement between local stock exchanges and market players in order to revise these regulations. IMPACT ON SELECTED LISTED COMPANIES: NEUTRAL FOR UNAF, POSITIVE FOR MSICH, SZLV Starting from Jan. 1, 2011, VAT will not be levied on agricultural producers selling New VAT rules for agro grain, meaning they will neither pay the tax to state budget (as was the case before) producers, distribution nor keep it in their bank accounts to reinvest in operations. However, they will still companies and traders… pay VAT on purchased materials and services used in production (COGS). Thus, the abolition of VAT on grain sales is unlikely to bring crop prices down. Grain traders buying crops directly from producers and exporting them will therefore not deal with VAT at all. Intermediaries, however, will have to pay VAT on grain purchased from producers and sold to exporters. Such mechanism should stimulate traders and exporters to buy grain directly from …to facilitate grain exports producers rather than deal with VAT refund credits from the state. This should help to make the market more transparent and facilitate grain export procedures, thereby carrying positive implications for listed grain producers such as Astarta Holding [Buy; FV $37.53], MHP [Hold; FV $23.60], Kernel Holding [Under Review], Ukrros [Buy; FV $0.87], Mriya Agro Holding [Under Review], Agroton [Not Rated], Sintal Agriculture [Not Rated], MCB Agricole [Not Rated], Landkom [Not Rated] and Dakor Agro Holding [Not Rated]. The Tax Code increases the base royalty rate for oil from $26/bbl to $36/bbl for Oil royalties to increase 40%, reservoirs above 5,000 m and from $9.7/bbl to $13.6/bbl for those below 5,000 m. A gas royalties 18.5% correction coefficient, calculated by dividing the imported oil price by $71/bbl, will be applied to the base rate. The base rate for natural gas was increased from $25/tcm to $30/tcm for above-5,000 m deposits and from $12.6/tcm to $14.9/tcm for deeper than 5,000 m extraction. The correction coefficient will be calculated by dividing the average price of imported gas by $179.5/tcm. For companies supplying gas to households, the royalties will grow to $7.4/tcm (above 5,000 m) and $5.9/tcm (below 5,000 m). The higher royalties will obviously have a negative impact on oil and gas producers by denting their net sales. At the same time, the law closes the legal loophole that has so far enabled Ukrnafta Ukrnafta: no more loopholes [Hold; FV $54.5] to sell oil at below market prices. The company presently sells oil to sell oil at 20% discount with an approx. 20% discount to the price of imported crude, and eliminating it will provide for an additional $216m of revenues annually (assuming a $75/bbl average for 2011), thus more than offsetting the planned increase in royalties. Tax Code: Neutral for Economy; Long-Term Positive for Stock Market 5

- 6. December 6, 2010 In addition, the Code provides for a hike in excise taxes on gasoline (+38% to EUR Higher gasoline tax will likely 182/t) and diesel fuel (+38-40% to EUR 42-90/t). It also introduces an LNG excise tax be passed on to final of EUR 40/t. The proposed tax increases imply additional cash outflows on gasoline consumers purchases as well as growth in working capital for companies such as Galnaftogaz [Buy; FV $0.025]. However, we expect fuel traders and retailers to fully pass higher costs on to end consumers, implying a UAH 0.5/liter increase in the gasoline retail price, as domestic demand for fuel has been quite inelastic. The legislation grants 10-year tax holidays for the light industry, hotels, aircraft Income tax holidays to benefit makers and shipbuilders. This bodes well for Motor Sich [Buy; FV $449], the leading Motor Sich, Zaliv Shipyard CIS producer of aircraft engines, and Zaliv Shipyard [Buy; FV $0.042], Ukraine’s and Clubhouse Group leading producer of large-capacity ships. We estimate potential income tax savings for those companies at $500m and $40m, respectively, over 2011-20. We plan to update our model on those companies accordingly and put our recommendation on Motor Sich under review for upgrade. This provision is also beneficial for hotel operator Clubhouse Group [Not Rated]. In more good news for shipbuilders, the Tax Code reinstates an earlier regulation VAT privileges bode well for (suspended in 2008) that allowed shipbuilders to pay VAT on imported goods with Zaliv Shipyard 720-day promissory notes. Since 2008 shipyards, whose production cycle is highly capital-intensive, have been required to pay VAT on imports with cash only, which depleted their cash flows and working capital, and the situation was exacerbated by the government delaying VAT refunds. The Code also confirms the earlier approved tax preferences for aircraft producers Additional tax preferences for which exempted eligible companies, including Motor Sich, from the land tax as well Motor Sich confirmed as VAT on imported goods purchased for production purposes. According to Motor Sich CEO Vyacheslav Bohuslayev, those tax breaks imply a 7% cost saving for the company, or $300m in total over 2010-16. Tax Code: Neutral for Economy; Long-Term Positive for Stock Market 6

- 7. December 6, 2010 MACROECONOMIC INDICATORS Year 2004 2005 2006 2007 2008 2009 2010E 2011F Real Sector Real GDP (% y-o-y) 12.1% 2.7% 7.3% 7.9% 2.1% (15.1%) 5.0% 4.5% Household Consumption (% y-o-y) 13.1% 20.6% 15.9% 17.1% 11.6% (14.1%) 2.5% 5.0% Gross Fixed Capital Formation (% y-o-y) 20.5% 3.9% 21.2% 20.0% 1.9% (48.1%) 8.0% 12.0% Nominal GDP (UAH bn) 345 441 544 721 950 915 1,105 1,304 Nominal GDP ($bn) 65 86 108 143 180 117 139 170 GDP per Capita (at F/X rate; $) 1,372 1,836 2,310 3,077 3,897 2,552 3,043 3,721 Real Industrial Output (% y-o-y) 12.5% 3.1% 6.2% 10.2% (3.1%) (21.9%) 10.0% 6.5% Real Agricultural Output (% y-o-y) 19.9% 0.0% 2.5% (6.5%) 17.1% 0.1% (1.5%) 0.5% Prices Consumer Price Index (e-o-p; % y-o-y) 12.3% 10.3% 11.6% 16.6% 22.3% 12.3% 9.5% 10.5% Consumer Price Index (avg.; % y-o-y) 9.0% 13.5% 9.1% 12.8% 25.2% 15.9% 9.2% 8.9% Producer Price Index (e-o-p; % y-o-y) 24.1% 9.6% 15.6% 23.3% 23.0% 14.3% 18.0% 9.0% Producer Price Index (avg.; % y-o-y) 20.5% 16.7% 9.6% 19.5% 35.5% 6.5% 19.0% 13.6% GDP Deflator (% y-o-y) 15.1% 24.5% 14.8% 22.7% 29.1% 13.0% 15.0% 13.0% External Sector Current Account Balance ($bn) 6.9 2.5 (1.6) (5.3) (12.8) (1.8) (2.8) (4.3) Current Account Balance (% of GDP) 10.6% 2.9% (1.4%) (3.7%) (7.1%) (1.5%) (2.0%) (2.5%) Merchandise Trade Balance ($bn) 3.7 (1.1) (5.2) (10.6) (16.1) (4.7) (8.4) (10.6) Goods Exports (FOB; $bn) 33.4 35.0 38.9 49.8 67.7 40.4 51.4 59.8 Exports Growth (y-o-y; %) 42.6% 4.8% 11.2% 28.0% 35.9% (40.3%) 27.2% 16.3% Goods Imports (FOB; $bn) 29.7 36.2 44.1 60.4 83.8 45.0 59.8 70.4 Imports Growth (y-o-y; %) 23.7% 21.8% 22.1% 36.9% 38.7% (46.2%) 32.7% 17.7% Services Trade Balance ($bn) 1.2 1.8 2.1 2.4 1.7 2.6 4.5 5.0 Net Income Balance ($bn) (0.6) (1.0) (1.7) (0.7) (1.5) (2.4) (2.0) (2.0) Net Current Transfers ($bn) 2.6 2.8 3.2 3.5 3.1 2.7 3.0 3.3 Capital and Financial Accounts Balance ($bn) (4.2) 8.0 3.7 15.8 9.7 (11.9) 8.0 6.0 Net FDI Inflow ($bn) 1.7 7.5 5.7 9.2 9.9 4.5 5.5 8.0 Gross External Debt ($bn) 30.6 38.8 54.5 80.0 101.7 103.3 109.9 114.3 Gross External Debt (% of GDP) 47.1% 44.4% 50.6% 56.0% 56.5% 88.1% 78.8% 67.3% Public Finances Central Budget Revenues (% of GDP) 1), 3) 20.4% 23.8% 24.5% 23.0% 24.4% 22.9% 22.6% 23.0% Central Budget Expenditures (% of GDP) 1), 3) 23.3% 25.6% 25.2% 24.4% 25.7% 26.8% 27.2% 27.4% Central Budget Balance (% of GDP) 1), 3) (3.0%) (1.8%) (0.7%) (1.4%) (1.3%) (3.8%) (4.5%) (4.4%) General Government Balance (% of GDP) 2), 3) (4.4%) (2.3%) (1.4%) (2.0%) (3.2%) (6.3%) (5.4%) (5.0%) Naftogaz Balance (% of GDP) 2), 3) na na na na na (2.5%) (1.0%) 0.0% Total Public Debt ($bn) 3) 16.1 15.5 15.9 17.6 24.6 39.8 54.7 68.6 Total Public Debt (% of GDP) 3) 24.7% 17.7% 14.8% 12.3% 19.9% 34.7% 38.9% 39.4% External Public Debt ($bn) 3) 12.1 11.7 12.7 13.8 18.6 26.6 33.4 42.9 Debt to IMF ($bn) 3) 1.6 1.2 0.9 0.4 4.7 12.9 16.2 22.2 Monetary & Banking Indicators Monetary Base (% y-o-y) 34.1% 53.9% 17.5% 46.0% 31.6% 4.4% 15.0% 20.0% Money Supply (M2, % y-o-y) 32.8% 53.9% 34.3% 50.8% 31.0% (5.4%) 20.4% 20.6% Credit Rates (avg.; UAH; % p.a.) 17.9% 16.4% 15.1% 13.9% 17.5% 20.9% 16.4% 15.3% Deposit Rates (avg.; UAH; % p.a.) 7.8% 8.5% 7.9% 8.2% 10.0% 13.8% 11.8% 9.3% Total Credits (e-o-p; UAH bn) 88.6 143.4 245.2 426.9 733.9 719.0 731.9 819.7 Credits Growth (%; y-o-y) 30.6% 61.9% 71.0% 74.1% 71.9% (2.0%) 1.8% 12.0% Total Credits (% of GDP) 25.7% 32.5% 45.1% 59.2% 77.3% 78.6% 66.3% 62.8% Total Deposits (e-o-p; UAH bn) 83.0 132.7 184.4 280.2 357.8 328.0 395.0 475.0 Deposits Growth (%; y-o-y) 35.2% 60.0% 38.9% 51.9% 27.7% (8.3%) 20.4% 20.3% Total Deposits (% of GDP) 24.0% 30.1% 33.9% 38.9% 37.7% 35.9% 35.8% 36.4% Forex Gross F/X Reserves ($bn) 9.5 19.4 22.3 32.5 31.5 26.5 36.0 46.0 Gross F/X Reserves (months of current year imports) 3.1 5.3 5.0 5.4 3.8 5.7 6.0 6.4 UAH:USD (market rate; e-o-p) 5.32 5.05 5.05 5.05 7.85 8.00 7.85 7.50 UAH:USD (market rate; avg.) 5.32 5.12 5.05 5.05 5.31 8.14 7.92 7.68 Notes: 1)Excluding social security funds, Naftogaz Ukrainy and bank rehabilitation costs; 2)The general government balance includes the central and local budgets and the Pension Fund, but excludes bank recapitalization costs; 3)SDRs are treated as deficit financing item and included in debt statistics. Sources: SSC, Finance Ministry, NBU, Dragon Capital estimates and forecasts Tax Code: Neutral for Economy; Long-Term Positive for Stock Market 7

- 8. December 6, 2010 RESEARCH 36D Saksahanskoho, Director, Research 01 033 Kyiv, Ukraine Andriy Bespyatov, PhD, CFA Tel.: (+380 44) 490 7120 bespyatov@dragon-capital.com Fax: (+380 44) 490 7121 Economics Electricity, Oil & Gas www.dragon-capital.ua Olena Bilan Dennis Sakva bilan@dragon-capital.com sakva@dragon-capital.com Managing Director Tomáš Fiala Politics Fixed Income fiala@dragon-capital.com Viktor Luhovyk Olga Slyvynska luhovyk@dragon-capital.com slyvynska@dragon-capital.com SALES AND TRADING Olena Bilan Banking & Insurance bilan@dragon-capital.com EQUITIES Anastasia Tuyukova Igor Buinyi tuyukova@dragon-capital.com buinyi@dragon-capital.com Managing Director, Equities Sales and Trading Metals & Mining Editing Dmytro Tarabakin Sergiy Gayda Viktor Luhovyk tarabakin@dragon-capital.com gayda@dragon-capital.com luhovyk@dragon-capital.com Oleksandr Makarov Managing Director, makarov@dragon-capital.com Research Assistants International Equity Sales Volodymyr Skepskiy Peter Bobrinsky Chemicals, Food & Agriculture, skepskiy@dragon-capital.com bobrinsky@dragon-capital.com FMCG Nadiya Syhydyuk Tamara Levchenko syhydyuk@dragon-capital.com Director, Equity Sales levchenko@dragon-capital.com Vikentiy Chebotarov Andriy Dmytrenko, CFA chebotarov@dragon-capital.com dmytrenko@dragon-capital.com Manufacturing, Real Estate, Telecommunications Director, Trading and Domestic Sales Taisiya Shepetko Denis Matsuyev shepetko@dragon-capital.com matsuyev@dragon-capital.com International Sales Fyodor Bagnenko bagnenko@dragon-capital.com FIXED INCOME Managing Director, Fixed Income Dray Simpson simpson@dragon-capital.com Director, Fixed Income Trading Ivo Suchy suchy@dragon-capital.com Fixed Income Trading Oleksandr Ublinskykh ublinskykh@dragon-capital.com Fixed Income Sales Kostyantyn Kucherenko kucherenko@dragon-capital.com Armen Bagirian bagirian@dragon-capital.com Svitlana Rusakova rusakova@dragon-capital.com DISCLAIMER This report has been prepared by Dragon Capital for information purposes only and is not an offer or solicitation to deal in any security. The opinions, forecasts and estimates in this report reflect our good-faith judgment as of the date of publication, and may change without notice. Although the information in this report comes from sources we believe to be reliable, and although we have made every effort to ensure its accuracy at the time of publication, we make no warranty, express or implied, of this report's usefulness in predicting the future performance, or in estimating the current or future value, of any security. Nor should this report be regarded as a complete description of the securities or markets referred to herein. Any opinions expressed herein may differ from opinions on the same subject expressed by other business departments of Dragon Capital as a result of employing different assumptions or methodology. Any investment decision made on the basis of this report shall be made at the investor's sole discretion, and under no circumstances shall Dragon Capital or any of its employees or related parties be liable in any way for any action, or failure to act, by any party, on the basis of this report. Nor shall Dragon Capital or any of its employees or related parties be liable in any way for any loss or damages arising from such action or failure to act. Dragon Capital does and seeks to do business with companies covered in its research reports. Investors should therefore be aware of a potential conflict of interest. Additional information on securities or companies discussed in this report is available upon request. This report may not be reproduced without the prior written permission of Dragon Capital; when quoting, please cite Dragon Capital. Tax Code: Neutral for Economy; Long-Term Positive for Stock Market 8