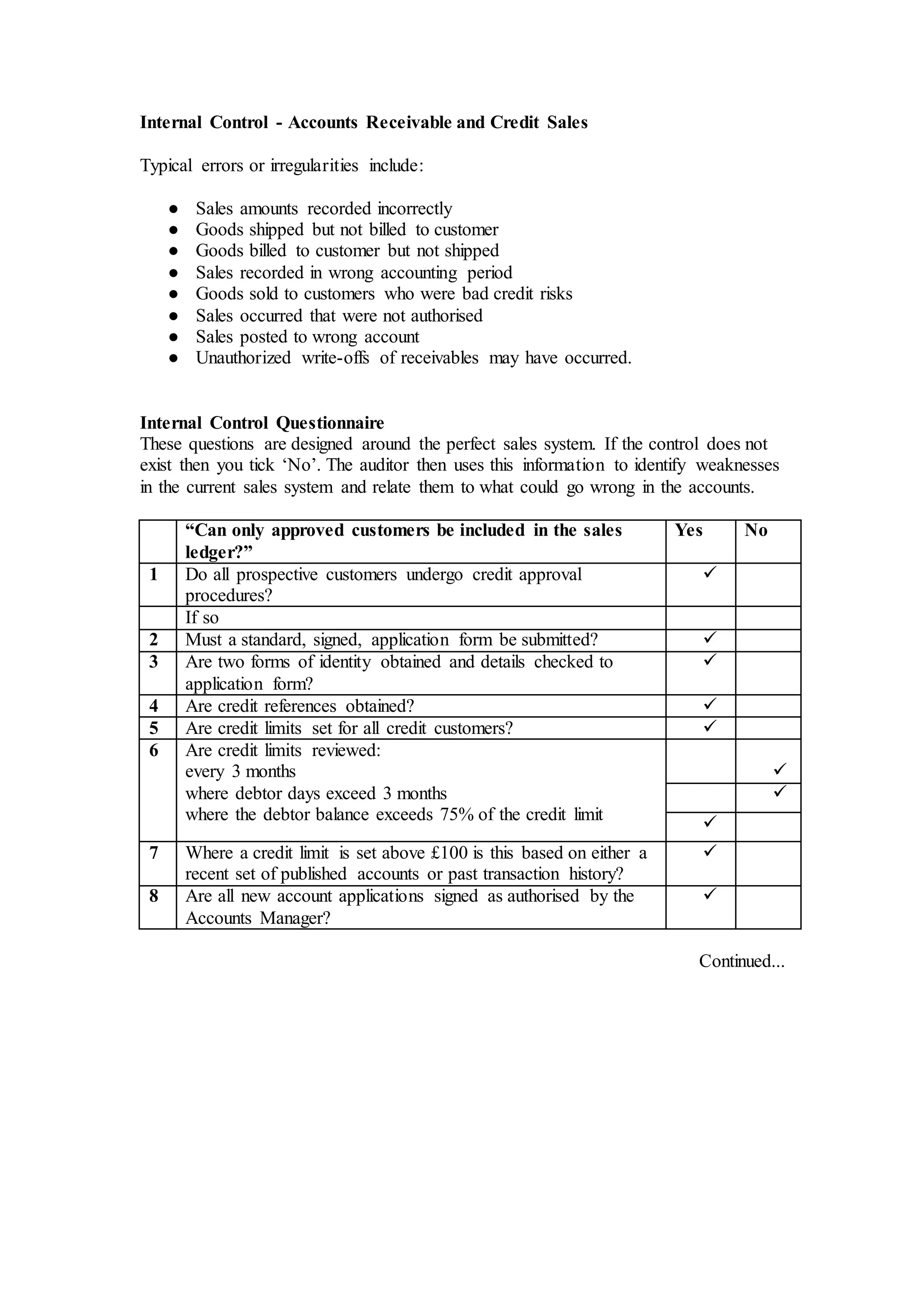

Typical errors in accounts receivable and credit sales include incorrectly recorded sales amounts, goods shipped but not billed, goods billed but not shipped, and sales recorded in the wrong period. An internal control questionnaire identifies controls over credit approval of customers, order acceptance, goods delivery, invoicing, and cash receipt posting to ensure accurate financial reporting. Weaknesses identified include a lack of goods monitoring, weak goods checking, a lack of segregation of duties, and easy vault access. Recommendations include implementing documents to check goods availability, having both the loader and deliverer check goods, properly segregating duties among staff, and restricting vault access.