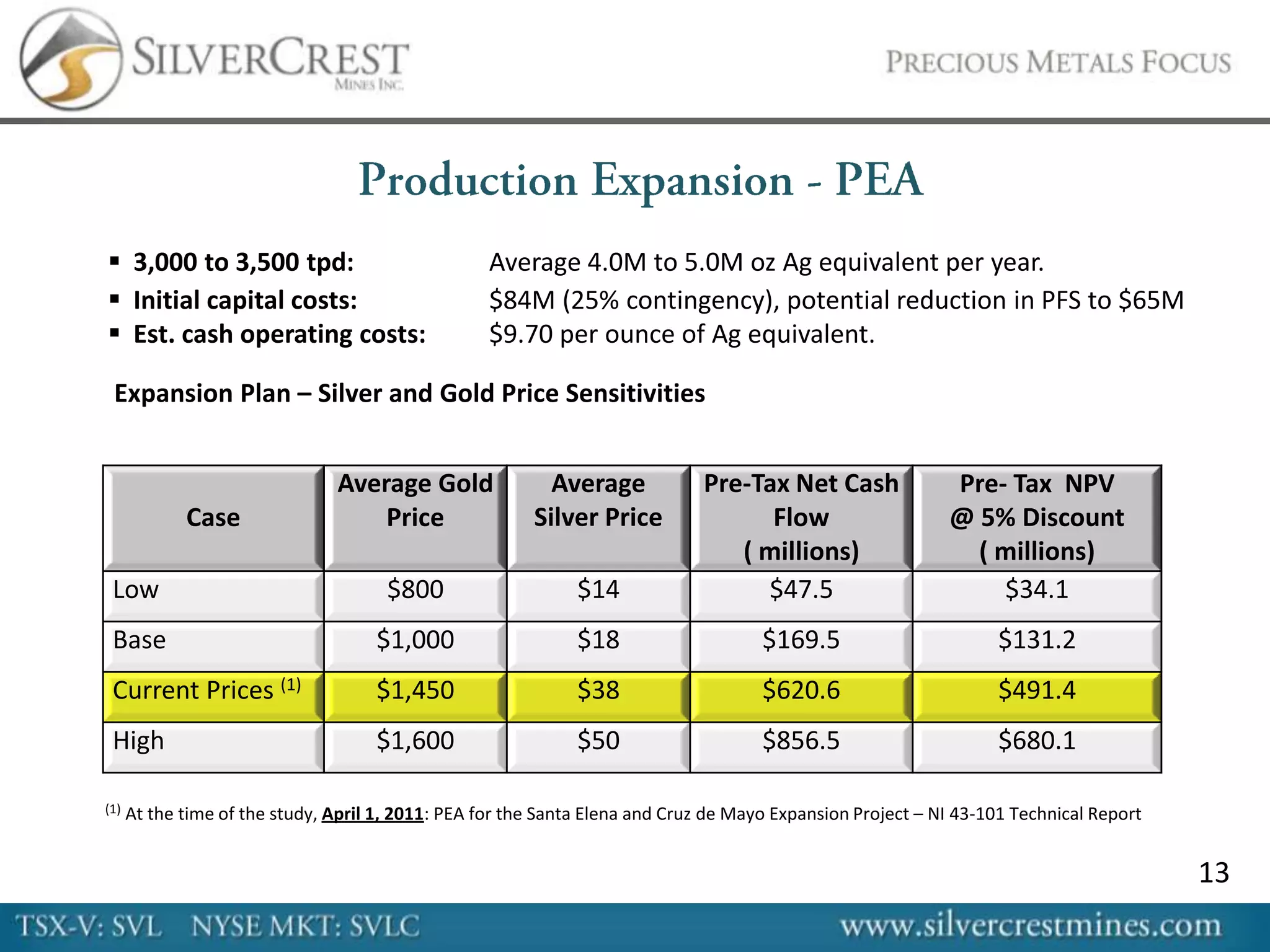

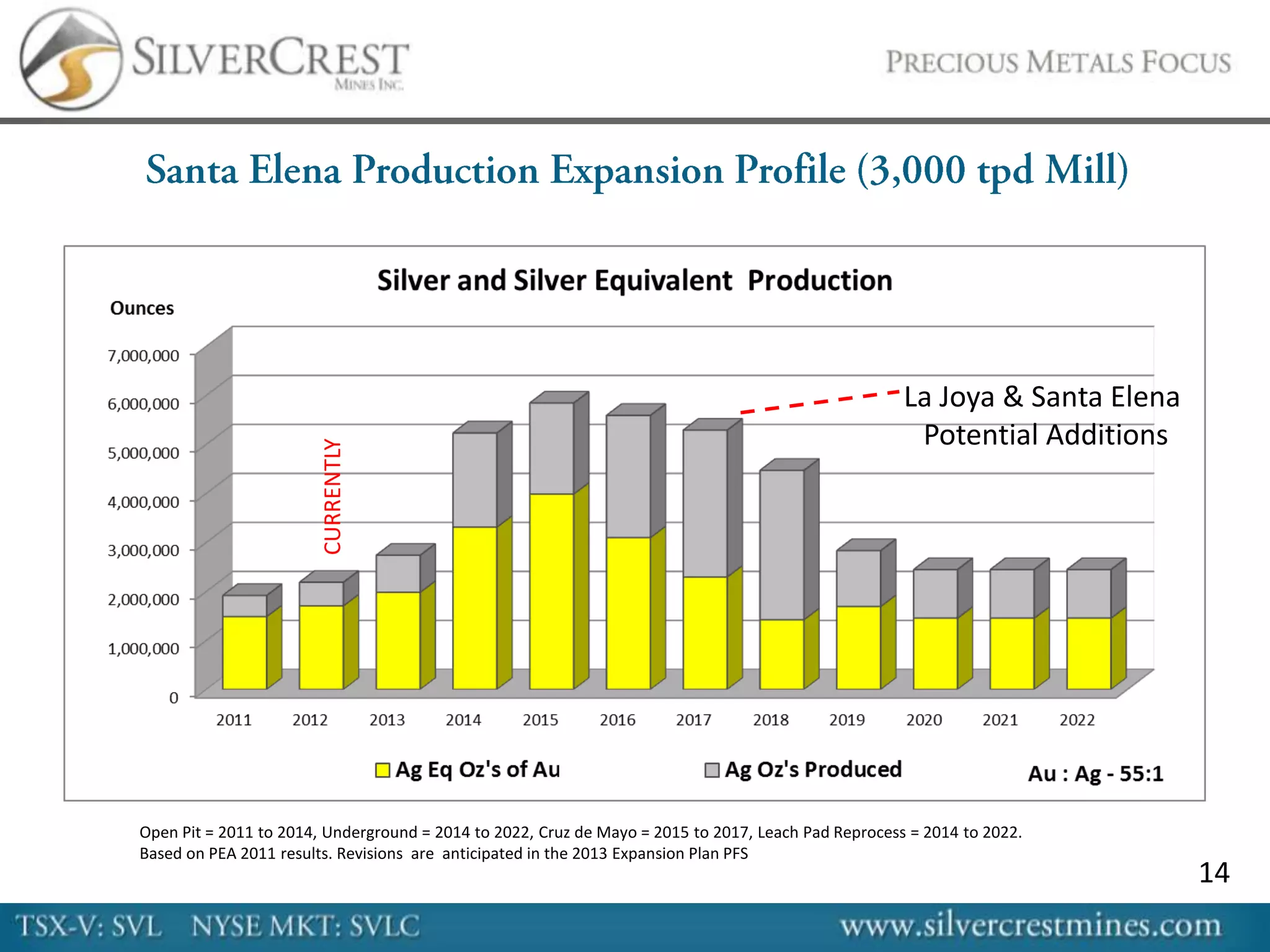

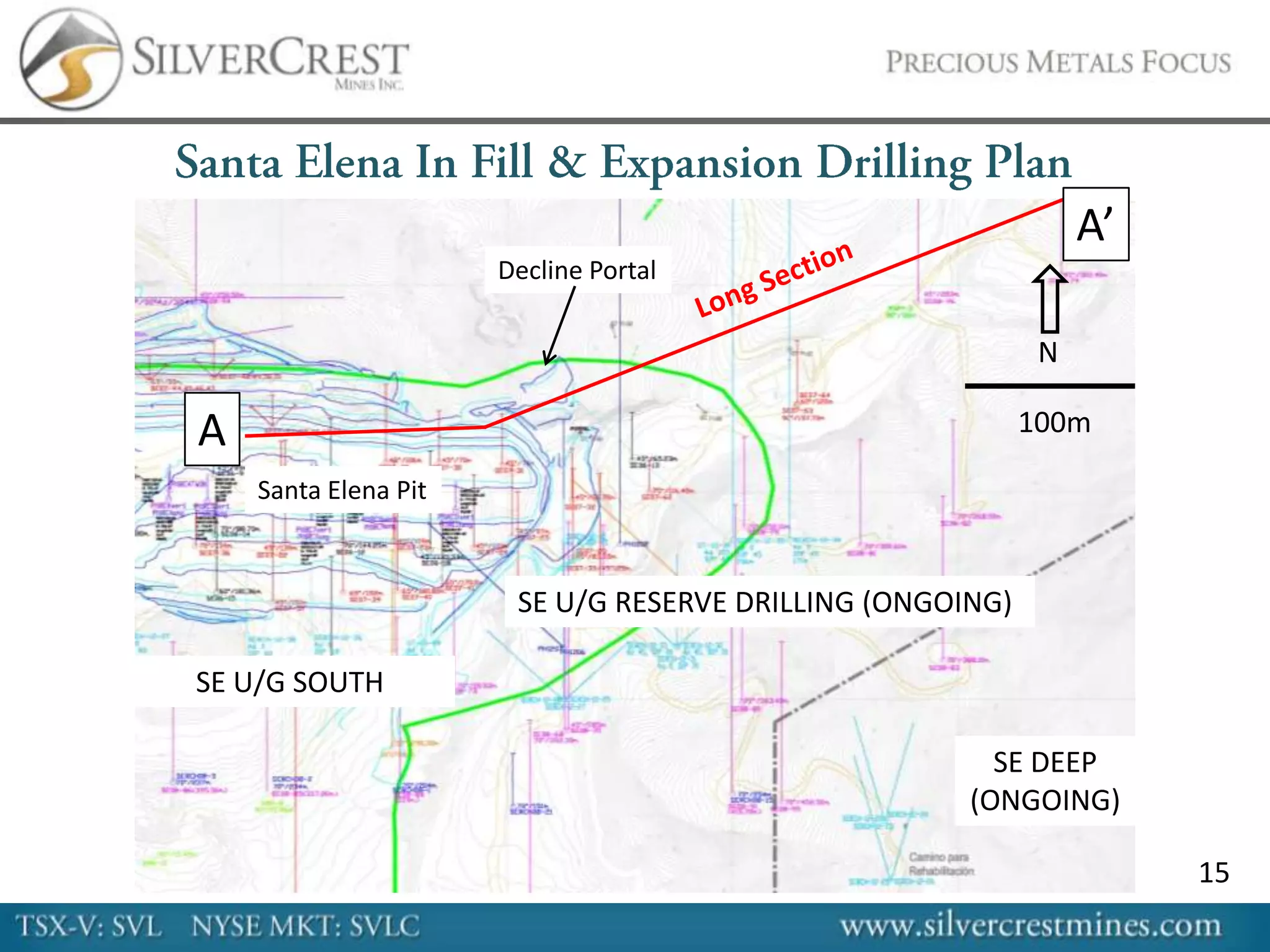

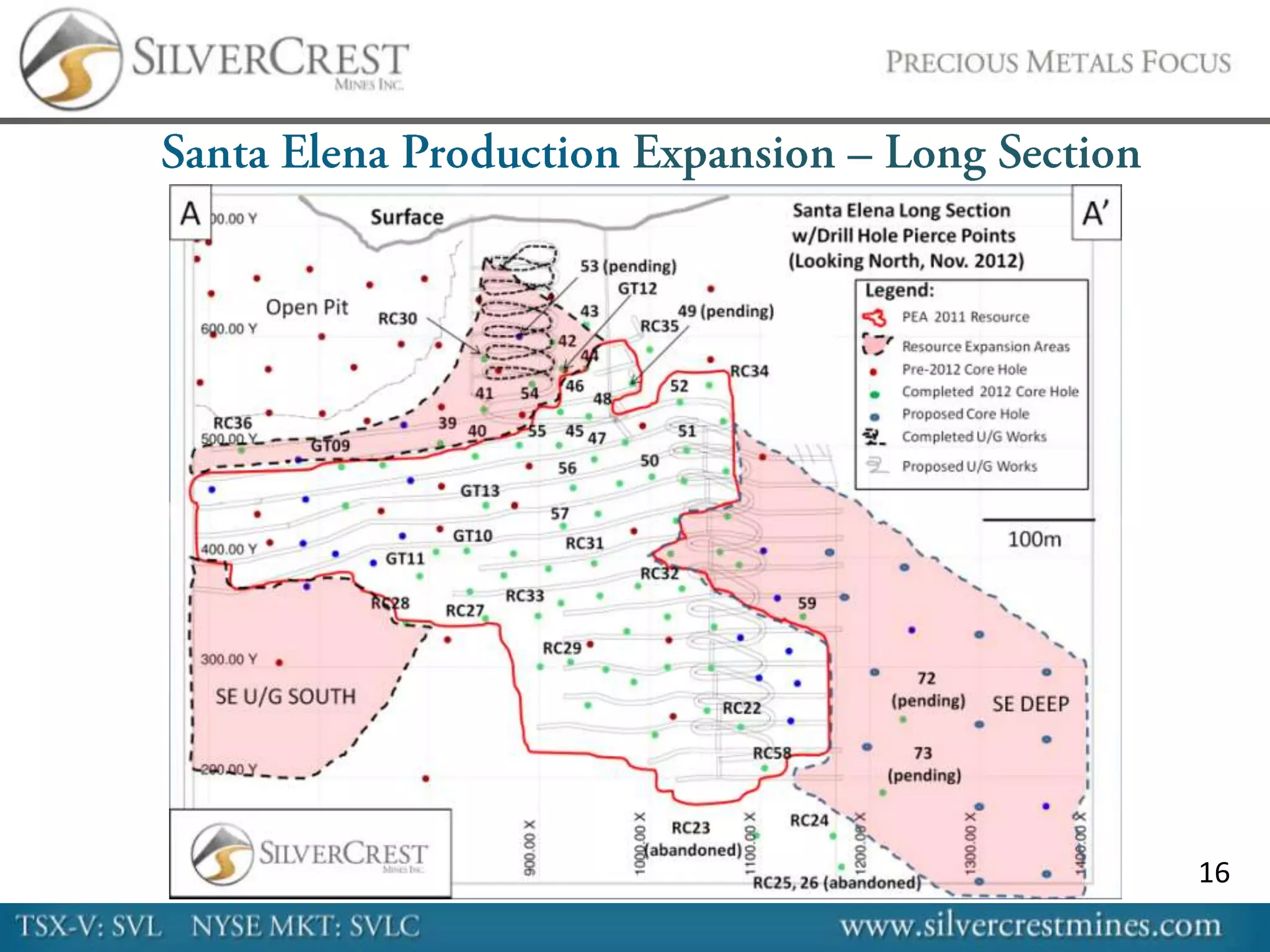

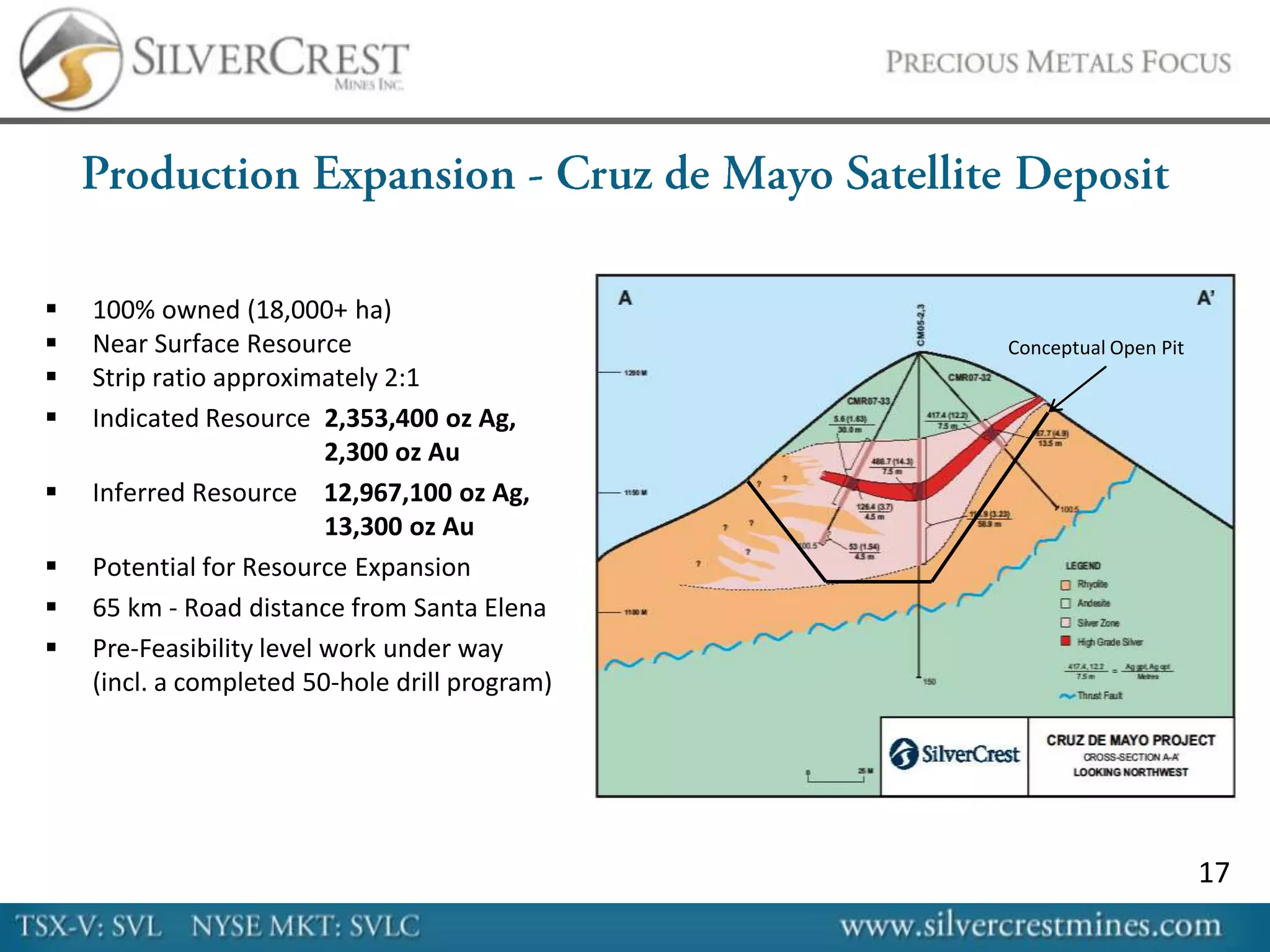

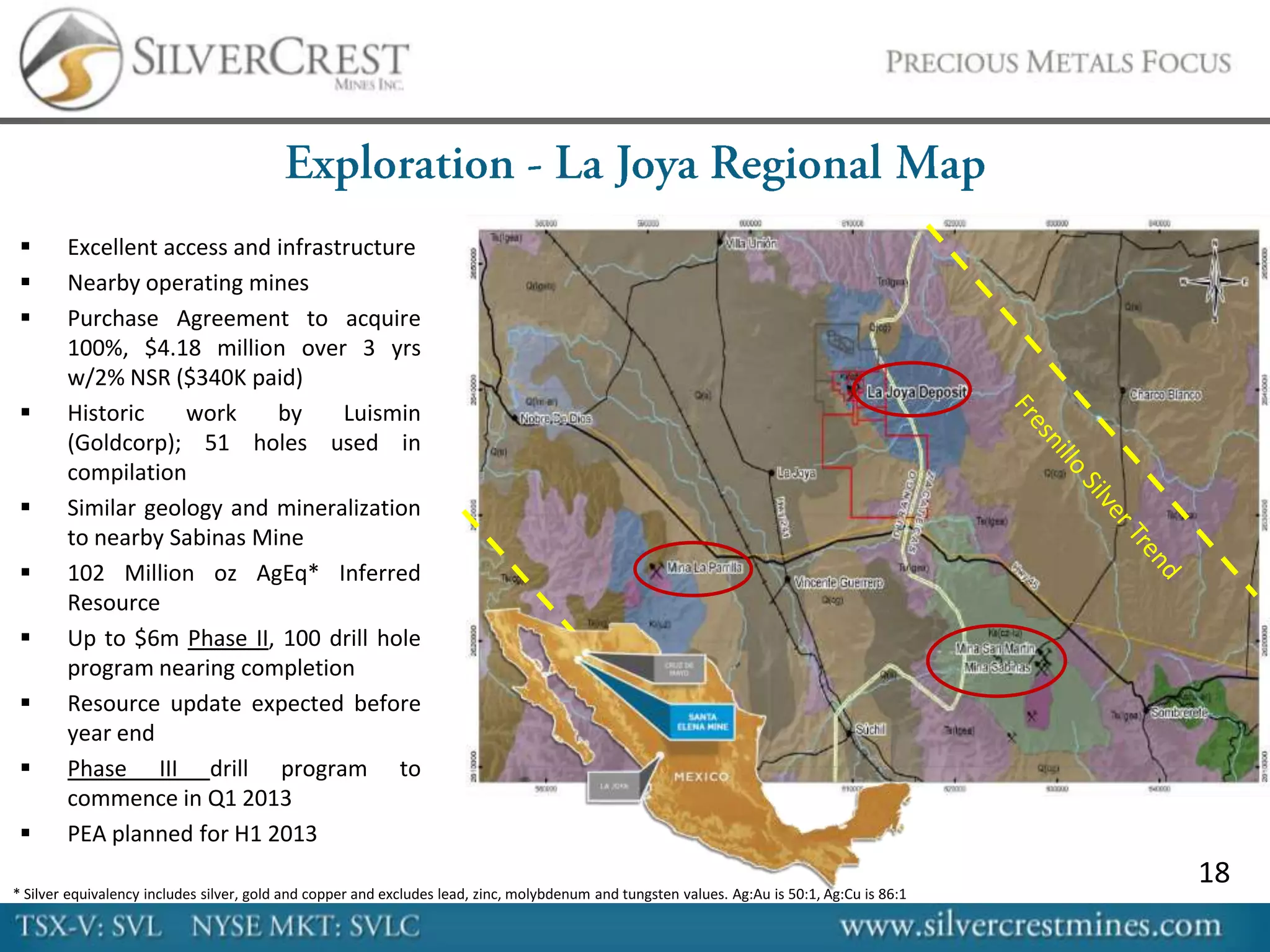

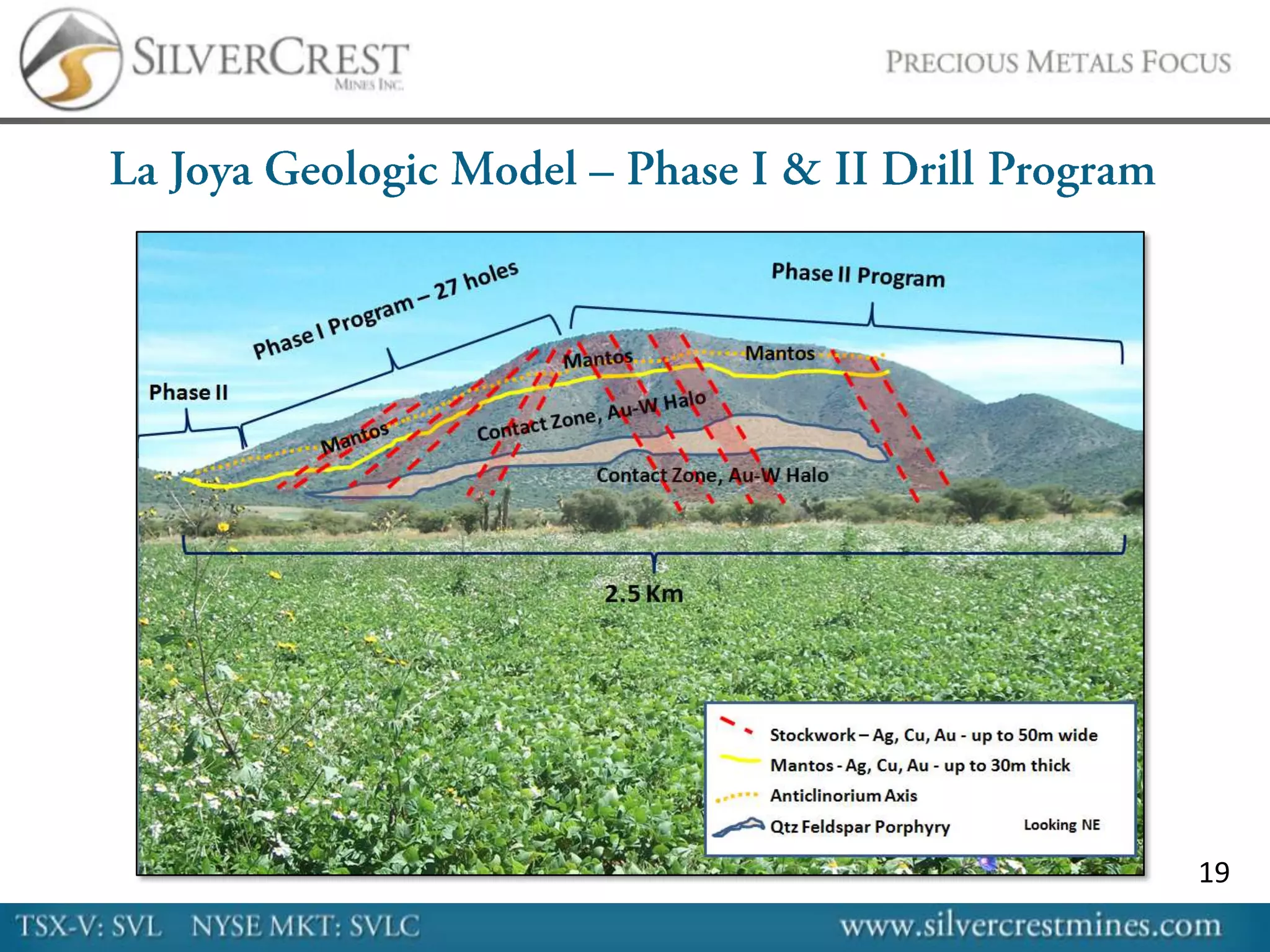

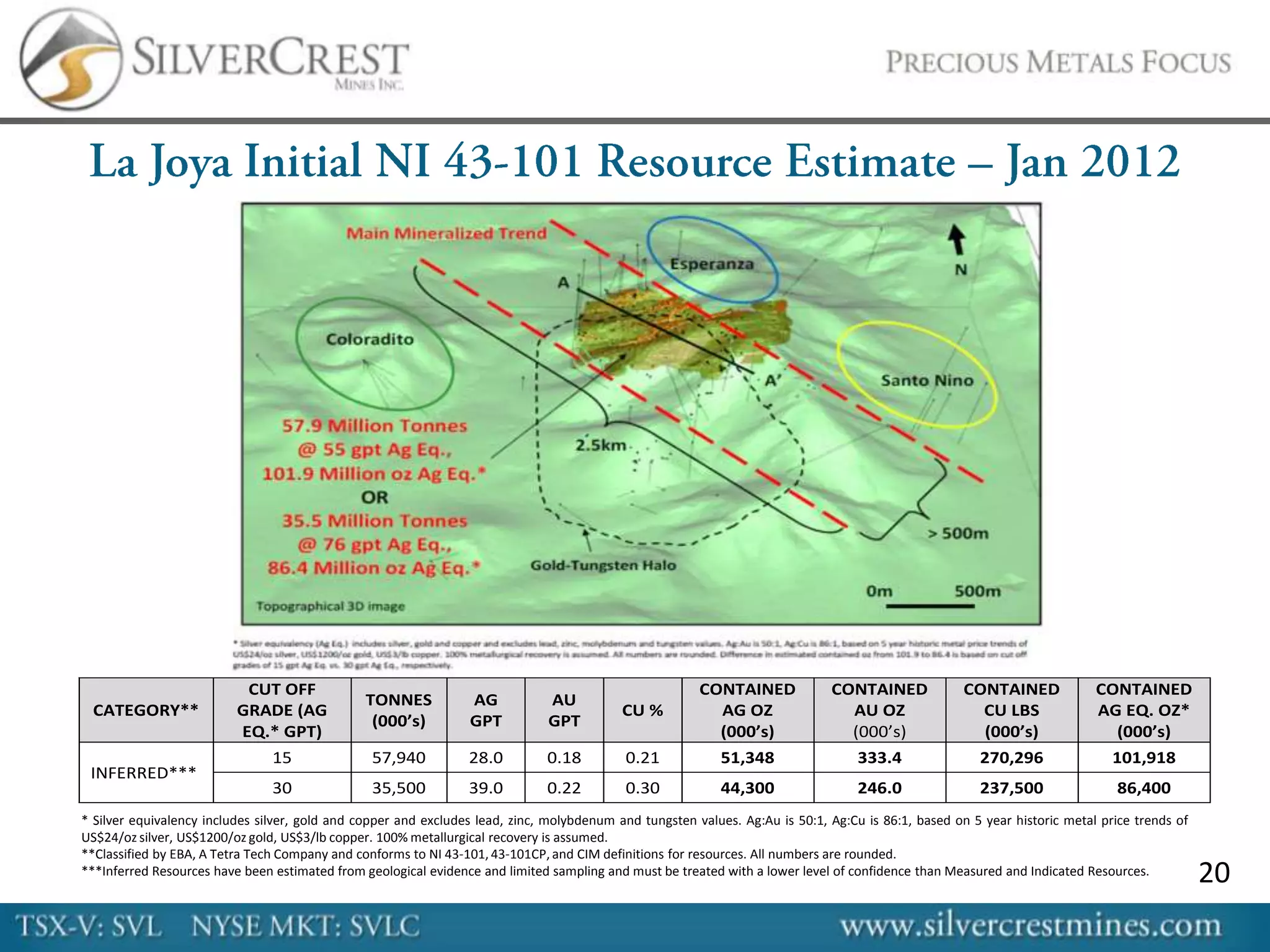

This presentation discusses a mining company's operations and mineral properties. It provides forward-looking statements about anticipated results and developments at the company's operations and properties. These statements concern future production, exploration, development plans and economic returns, which are subject to various risks and uncertainties that could cause actual results to differ materially from expectations. The document also provides summaries of the company's current resource estimates across its properties.

![Silvercrest january 2013 [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/silvercrestjanuary2013compatibilitymode-130123141613-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)