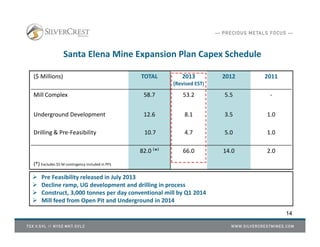

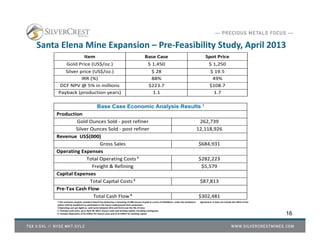

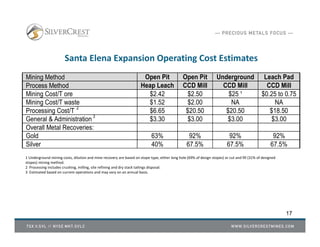

This corporate presentation from September 2013 outlines the company's financial performance, operational updates, and forward-looking statements regarding its mining activities, including risks that may affect future results. It includes a description of properties such as Santa Elena and La Joya, total reserves, production figures, and management team expertise. Investors are cautioned against relying solely on forward-looking statements due to inherent risks and uncertainties in the mining industry.

![Silvercrest january 2013 [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/silvercrestjanuary2013compatibilitymode-130123141613-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)