Downloaded 49 times

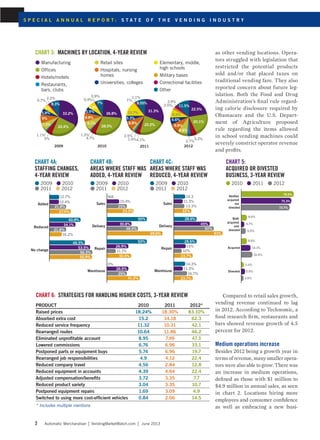

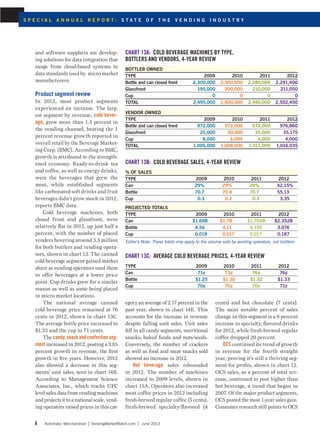

The vending industry saw a revival in 2012, with overall revenue growing to $19.31 billion, a rise attributed to increasing consumer confidence and strategic price hikes by operators. Technological investment and the introduction of micro markets were pivotal in enhancing profitability, while operators faced challenges from new legislation related to health regulations in schools. Despite positive growth, vending revenue still lagged behind retail sales, with many operators expressing concern over future regulatory constraints.