Download as PDF, PPTX

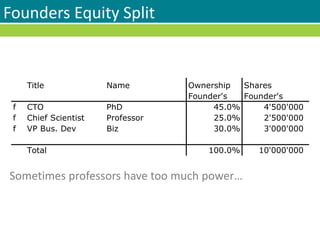

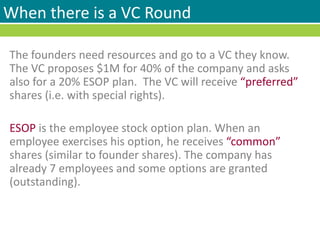

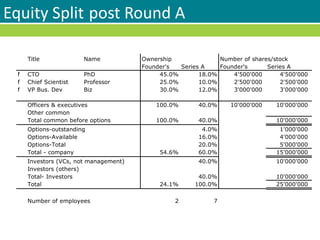

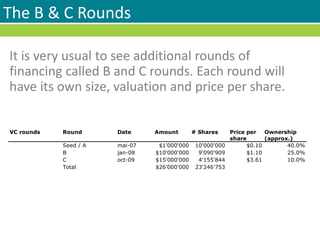

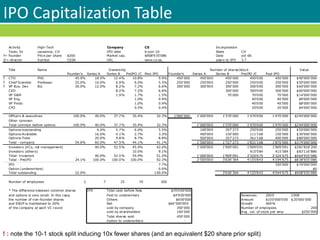

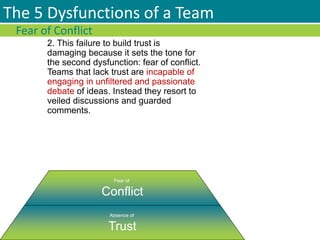

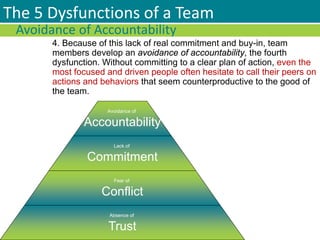

The document discusses equity distribution among founders in startups, exploring factors such as past contributions, future commitments, and contributions of intellectual property from academic institutions. It provides a detailed case study on equity splits during various financing rounds, including seed, Series A, B, and C rounds, and their implications on founder and employee stock ownership. Further, it examines the importance of trust and team dynamics in achieving effective collaboration among startup team members.