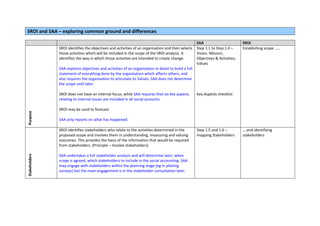

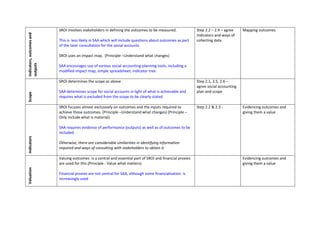

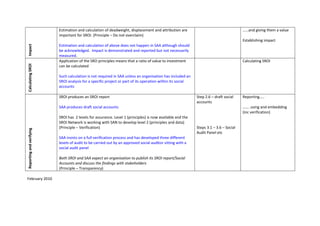

The document compares Social Return on Investment (SROI) and Social Accounting and Audit (SAA), which are both approaches to understanding and accounting for social impact. While they have many similarities in principles and methods, some key differences are that SROI focuses on outcomes and financial valuation, while SAA requires reporting on internal issues and outputs. SROI can be used to forecast impact, while SAA reports on past performance. SROI involves stakeholders primarily in defining outcomes, while SAA engages stakeholders more broadly. SROI calculates ratios and estimates factors like deadweight, while SAA demonstrates but does not necessarily measure impact. Both aim for transparency through reporting and assurance of reports.