Downloaded 40 times

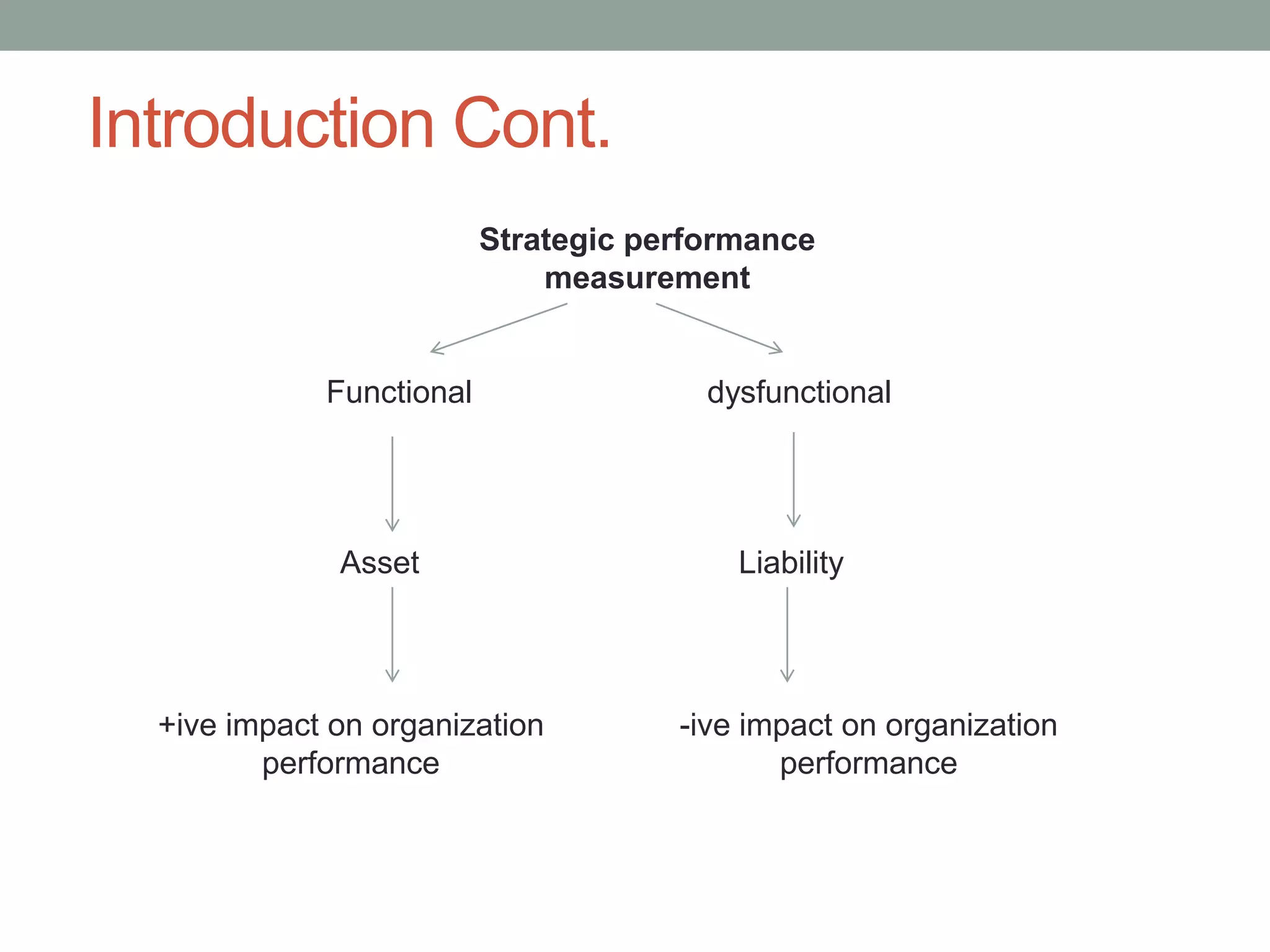

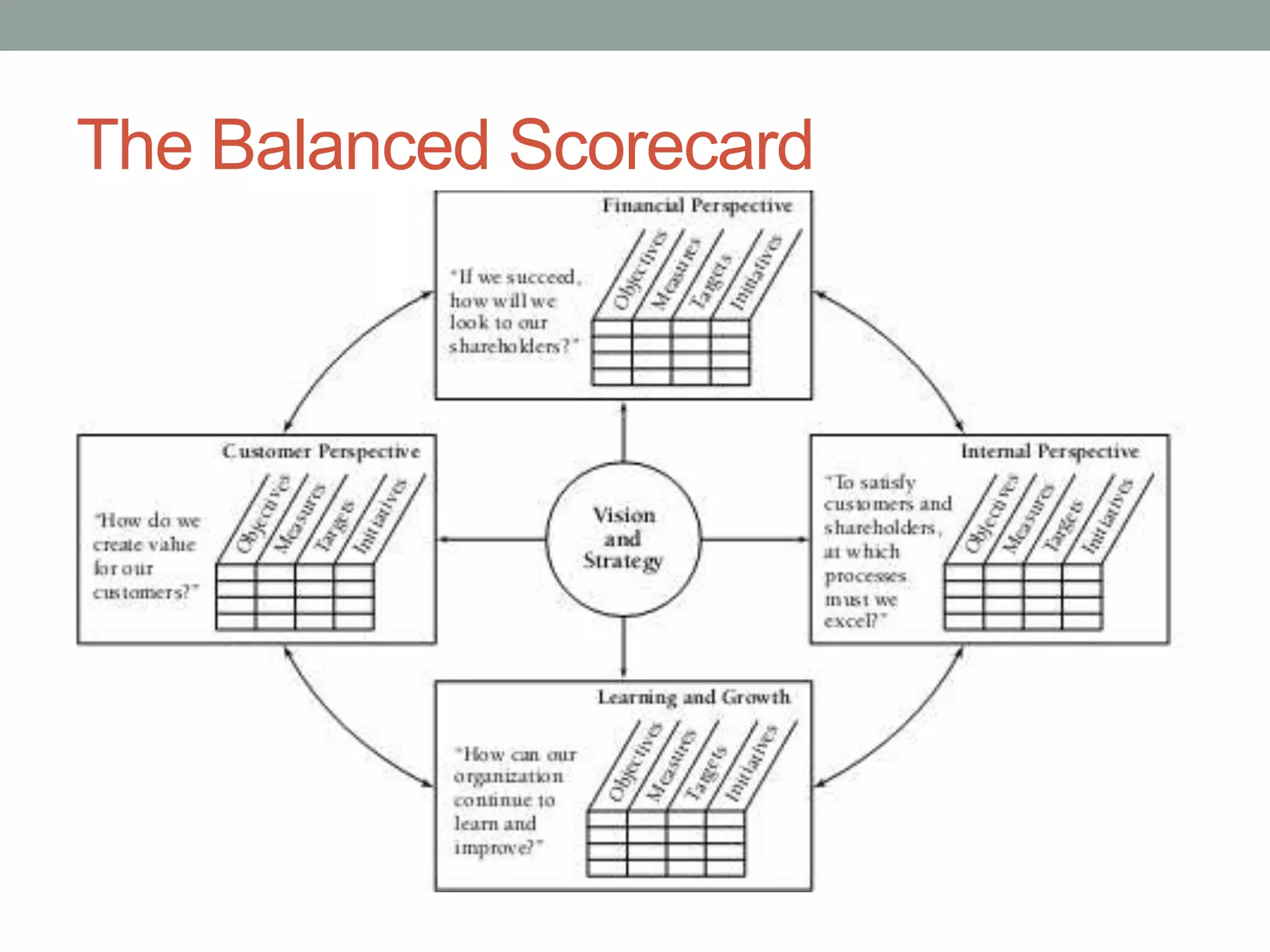

This document discusses strategic performance measurement systems and four related papers. The introduction defines strategic performance measurement and explains its importance for aligning organizations with long-term goals. Four papers are then summarized that examine: 1) How performance measurement can play an active role in strategy reviews, 2) Using non-financial indicators to improve strategic alignment and learning, 3) How flexible performance systems can effectively implement strategic changes, and 4) How non-financial indicators can create organizational rigidity if overused. The discussion analyzes themes across the papers regarding the multiple roles of performance measurement in implementing, reforming and communicating strategy. It emphasizes defining the intended roles and characteristics of a performance system upfront to ensure consistency with organizational aims.

![Factors influencing[1]](https://cdn.slidesharecdn.com/ss_thumbnails/factorsinfluencing1-111211095358-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)