Downloaded 34 times

![REFERENCE

[1] Musa, J.D, Software Reliability Engineering McGraw-

Hill, 1998

[2] Musa, J.D., Iannino, A., Okumoto, k., 1987. “Software

Reliability: Measurement Prediction Application”. McGraw-

Hill, New York.

[3] Pham. H., 2003. “Handbook of Reliability Engineering”,

Springer

[4] Balakrishnan.N., Clifford Cohen; Order Statistics and

Inference; Academic Press inc.;1991.

[5] K.Ramchand H Rao, Dr. R.Satya Prasad, Dr.

R.R.L.Kantham, Assessing Software Reliability Using SPC

: An Order Statistics Approach, International Journal of

Computer Science, Engineering and Applications

(IJCSEA) Vol.1, No.4, August 2011 13](https://image.slidesharecdn.com/priyanka2-140519114557-phpapp02/75/SOFTWARE-PROCESS-MONITORING-AND-AUDIT-13-2048.jpg)

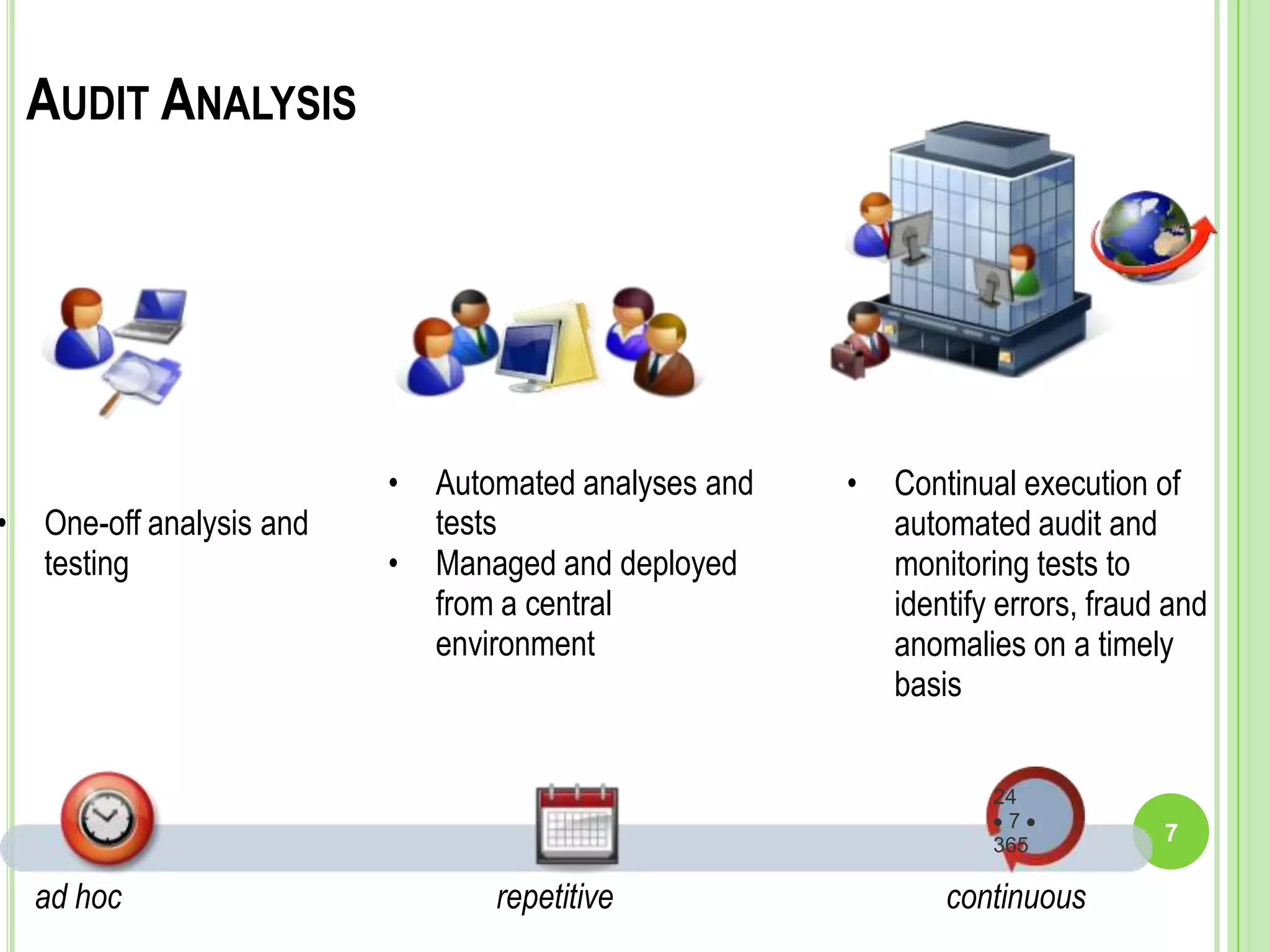

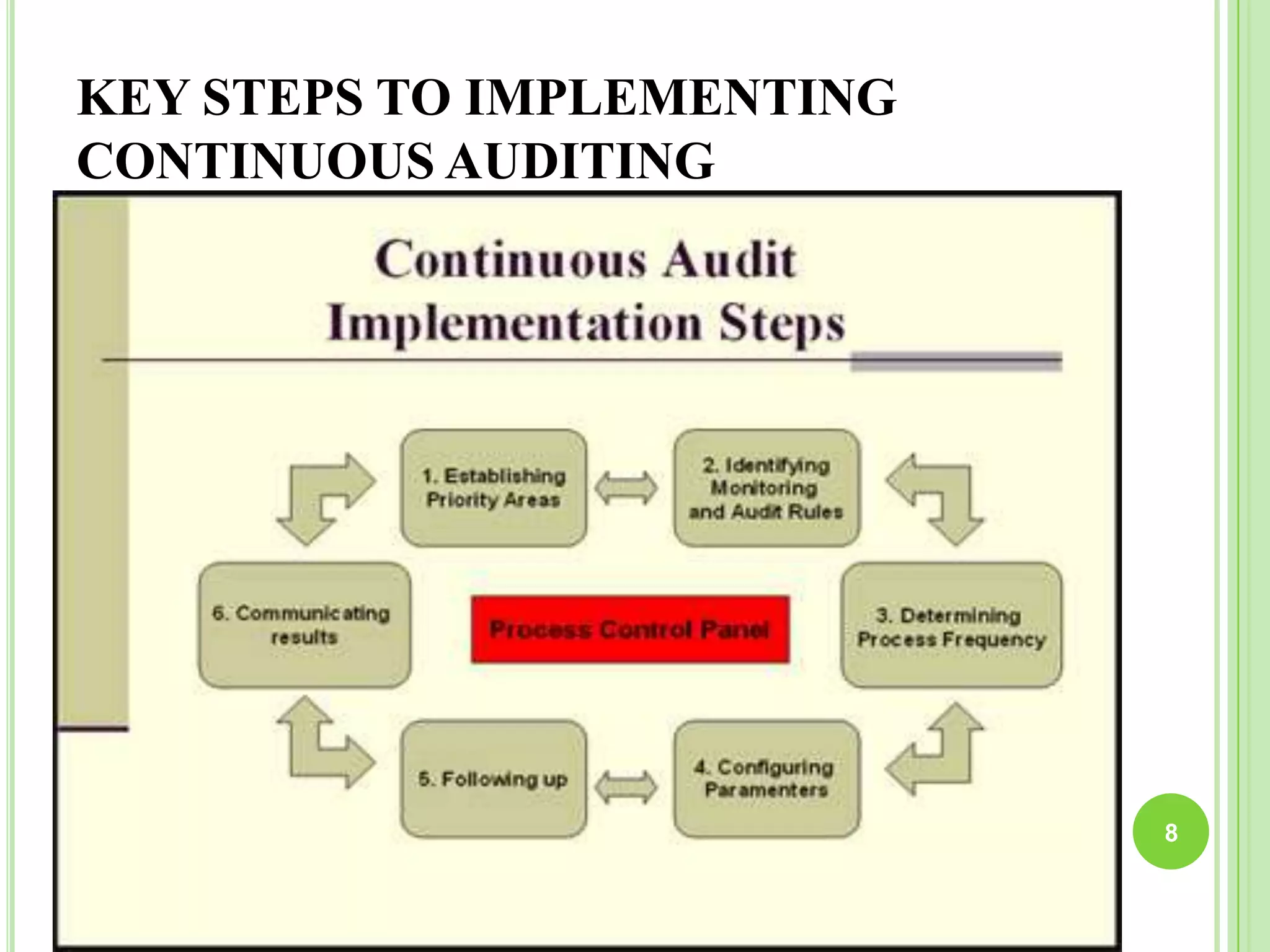

This document provides an overview of process monitoring and auditing. It defines monitoring as ongoing checking and measuring that can identify needs for a more formal audit. An audit is a systematic, disciplined evaluation of processes and controls to understand performance against standards and identify improvement areas. Key characteristics of audits are that they are formal, independent reviews following professional standards. The document outlines audit planning, testing, validation, reporting, and follow-up of corrective actions. It also discusses pre-audit, onsite audit, and post-audit activities and describes internal, external, and certification types of audits.

![BCMS-Internal-Auditor-Course-ppt [Autosaved].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/bcms-internal-auditor-course-pptautosaved-250116213343-632d8a6a-thumbnail.jpg?width=640&height=640&fit=bounds)