Download as PDF, PPTX

![Together We Build a Better Future 18

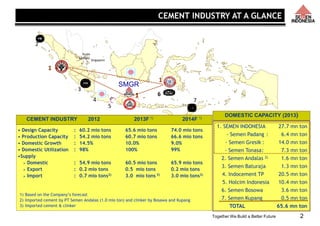

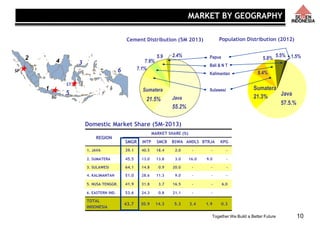

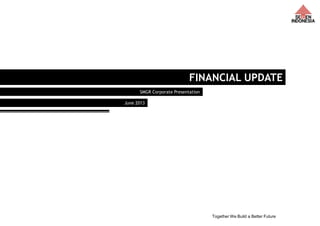

Description

(Rp bn)

1Q

2012

1Q

2013

Change

(%)

Net Revenue 4.284 5,584 29.4

Cost of Revenue 2,362 3,058 29.5

Gross Profit 1,922 2,484 29.3

Operating Expenses 669 879 31.6

Operating Income 1,254 1,605 28.0

EBITDA 1,410 1,862 32.0

Net Income 1,011 1,236 22.3

EPS (Rp) 170 208 22.3

Ratio (%) Formula

1Q

2012

1Q

2013

Ebitda margin Ebitda / Revenue 32.9 33.6

Interest coverage (x) Ebitda / Interest expense 258.3 24.7

Cost ratio [COGS + Opex] / Revenue 70,7 71,2

Total debt to equity *) Total debt / Total equity 48.5 44.0

Total debt to asset *) Total debt / Total asset 29,7 31.7

*) Total debt calculated from interest bearing debt

FINANCIAL HIGHLIGHT – 1Q 2013](https://image.slidesharecdn.com/smgrcorppresentationjuni2013-160613051914/85/Smgr-corp-presentation_juni_2013-19-320.jpg)

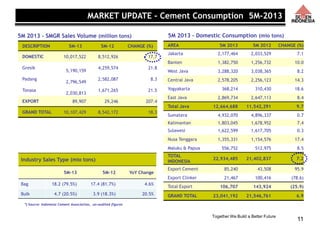

![Together We Build a Better Future 28

Outstanding

performance

Experienced

management

team

Conservative

capital

structure and

financial

policies

Robust cash flow

generation

Outstanding

business

performance

Favorable

industry

outlook

Outstanding business performance

– Leading cement player in Indonesia with over 43.% market share based on

sales volume for 4M-2013 and approximately 41% share of total installed

cement capacity (Source: Indonesia Cement Association (“ASI”))

– Strategically plants location is close to key markets throughout the country

– As of Dec 2012, acquired Thang Long Cement Company, Vietnam by 70%

share with installed capacity 2.3 mio tons per annum

– Substantial growth opportunities through expansion and optimization

– Superior distribution network and strong brands recognition

– Long-term access to raw materials for cement production and coal for fuel

consumption

– Concerns on environmental and Corporate Social Responsibility programs to

ensure sustainable growth.

Favourable industry outlook

– Cement consumption pretty much in-line with Indonesian economic growth

– Real estate and infrastructure projects and declining interest rates key

demand drivers

– High barriers to entry (plant, distribution and brand investment costs)

– Disciplined investment on supply side

Robust cash flow generation

– Historically strong revenue, margin and price trends

– High plant utilization and strong focus on cost and revenue management

Conservative capital structure and financial policies

– [Investment grade-like credit metrics]

– Conservative capital structure policy; low use of leverage

– Access to capital markets for expansion initiatives

Experienced management team

– Experienced and successful management team

Strengths of SMGR

SMGR’s COMPARATIVE & COMPETITIVE ADVANTAGE DRIVES SMGR TO BE

THE MARKET LEADER IN INDONESIA](https://image.slidesharecdn.com/smgrcorppresentationjuni2013-160613051914/85/Smgr-corp-presentation_juni_2013-29-320.jpg)

This document provides an overview of Indonesia's cement industry and Semen Indonesia's position within it. It notes that cement production capacity in Indonesia is expected to almost double to 108 million tons by 2017, driven by new plants from both domestic and foreign players. Semen Indonesia currently has the largest market share in Indonesia at 43.7% and will also be expanding capacity. The key drivers of future domestic cement demand are expected to be national economic growth, infrastructure expansion, and increasing per capita consumption as Indonesia's per capita consumption is still relatively low compared to other countries.