Downloaded 35 times

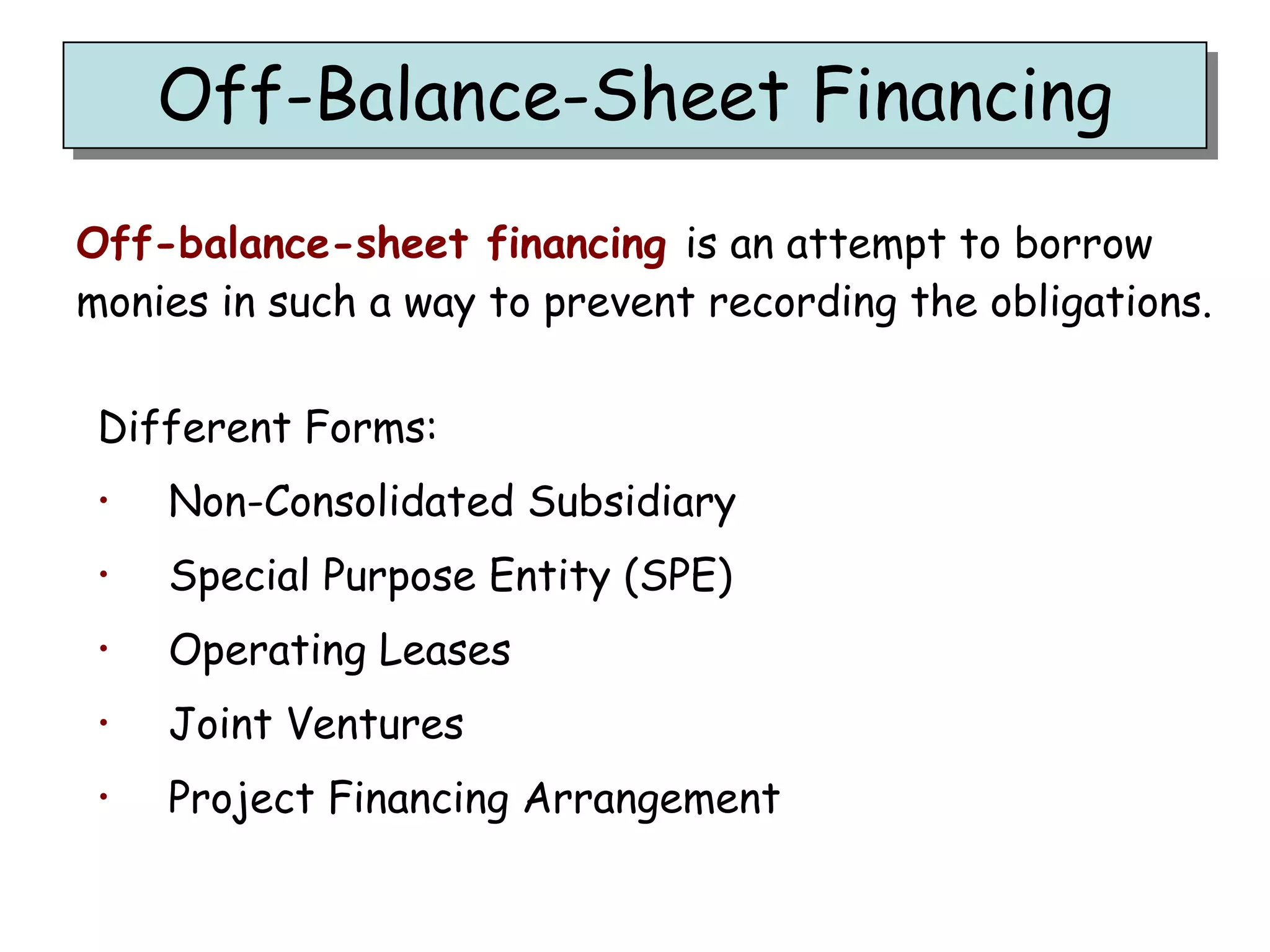

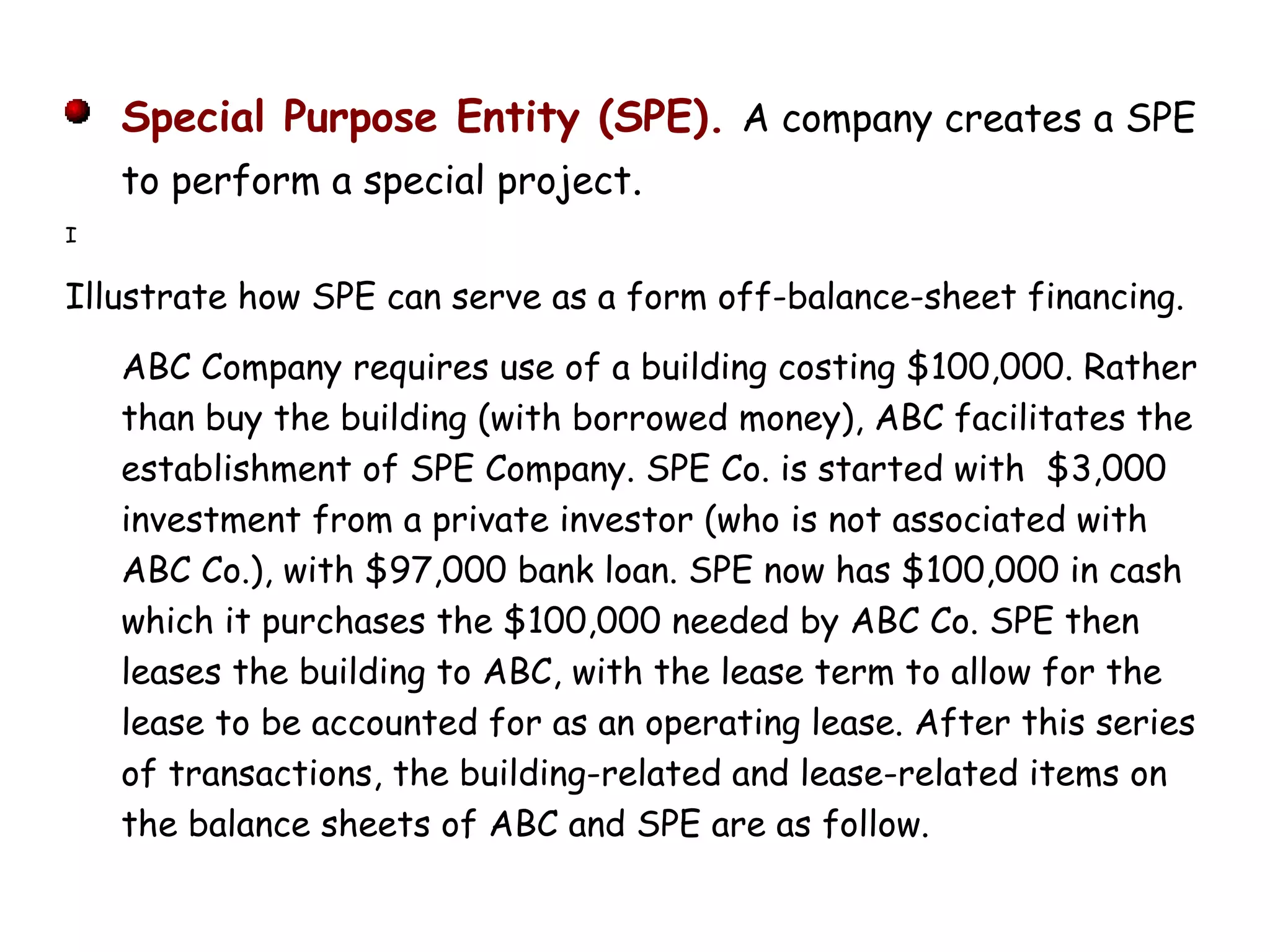

Off-balance sheet financing allows companies to borrow money without recording the associated obligations on their balance sheet. This is accomplished through various structures like non-consolidated subsidiaries, special purpose entities (SPEs), operating leases, and joint ventures. SPEs in particular allow companies to keep assets and liabilities off their books by transferring them to an independent entity, even if the company remains responsible for the SPE's debts. In response to Enron and other accounting scandals, the FASB issued new rules focusing on risk and rewards to better determine when SPEs should be consolidated with their parent company.