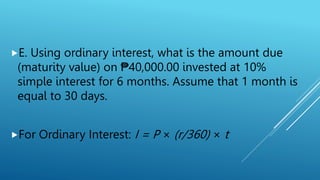

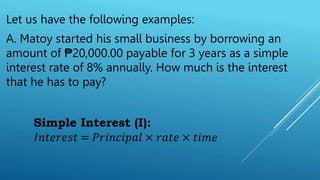

The document defines terms related to simple interest such as principal, rate, time, and interest. It then provides examples of calculating simple interest for various scenarios:

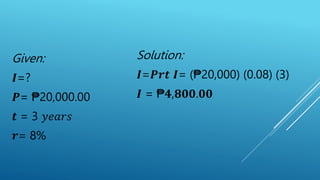

1) Calculating the interest on a 3-year, ₱20,000 loan at 8% annual interest.

2) Finding the maturity value of ₱200,000 deposited in a bank for 5 years at 1% annual interest.

3) Determining the maturity value of a ₱2,200,000 loan over 5 years at 6.75% annual interest.

4) Calculating the mortgage amount for a ₱4,000,000 home requiring a 25% down payment.

![Given:

𝑭 = ? 𝑷 =

₱200,000.00

𝒓 = 1% 𝒕 = 5 𝑦𝑒

𝑎𝑟𝑠

Solution: 𝑭 = 𝑷 (𝟏 + 𝒓𝒕)

𝑭 = ₱200,000 [1 + (0.01) (5)]

𝑭 = ₱𝟐𝟏𝟎,𝟎𝟎𝟎.𝟎𝟎](https://image.slidesharecdn.com/simpleinterest-230501111202-354c6de4/85/simple-interest-pptx-9-320.jpg)

![C. Dereck borrowed ₱2,200,000.00 payable for 5

years to purchase a pick-up truck. A bank offered him

a car loan with simple interest rate of 6.75% per year.

What is the maturity value of the loan?

Given:

𝑭 = ? 𝑷 = ₱2,200,000.00

𝒓 = 6.5% 𝒕 = 5 𝑦𝑒𝑎𝑟𝑠

Solution: 𝑭= 𝑷 (𝟏 + 𝒓𝒕) 𝑭= ₱2,200,000

[1+(0.065)(5)] 𝑭= ₱𝟐,𝟗𝟏𝟓,𝟎𝟎𝟎.𝟎𝟎](https://image.slidesharecdn.com/simpleinterest-230501111202-354c6de4/85/simple-interest-pptx-10-320.jpg)