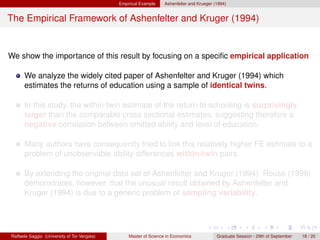

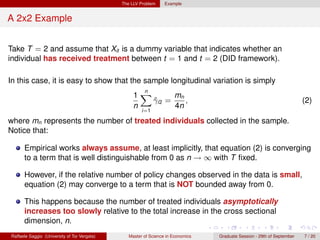

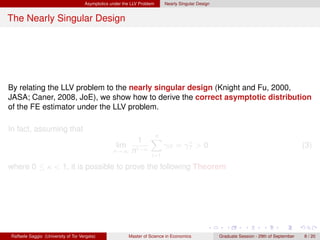

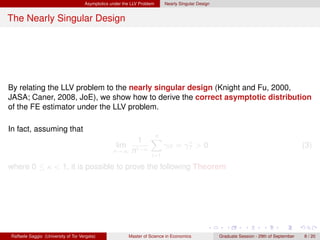

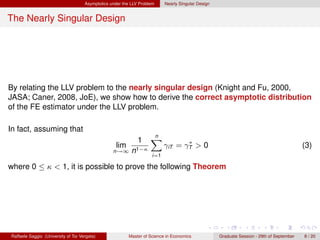

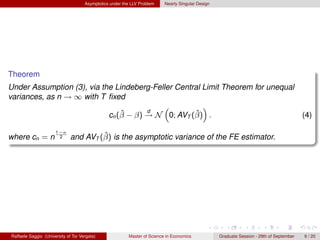

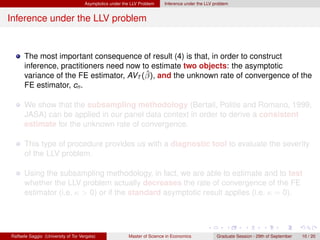

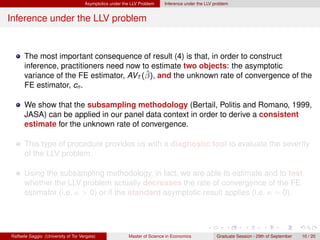

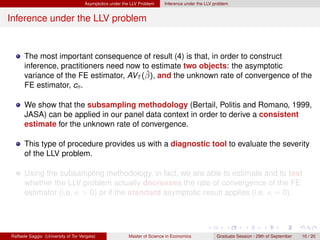

This thesis evaluates fixed effects linear panel data models, focusing on cases of low longitudinal variation of explanatory variables, which complicates the inference processes. It aims to formalize the impact of low longitudinal variation on the fixed effects estimator's asymptotic distribution and proposes a shrinkage estimator with reduced variance for better reliability in parameter estimation. The study highlights that while the fixed effects estimator remains consistent, the model's asymptotic properties can become complex due to low longitudinal variation.

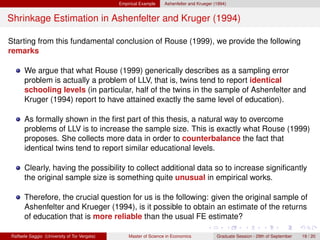

![Shrinkage Estimation Ridge regression

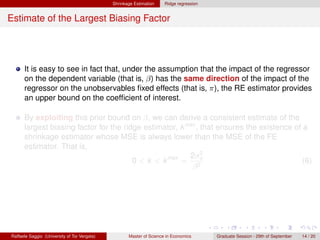

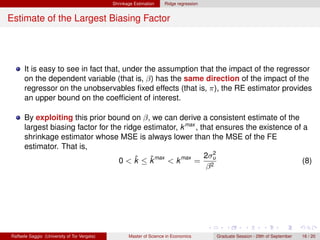

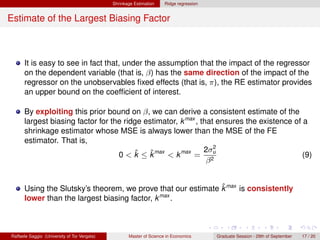

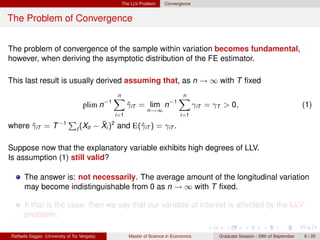

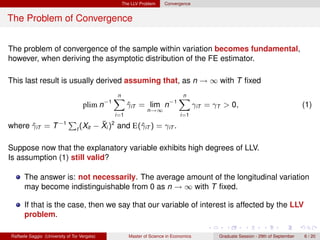

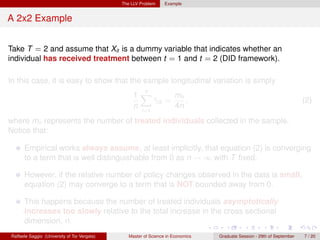

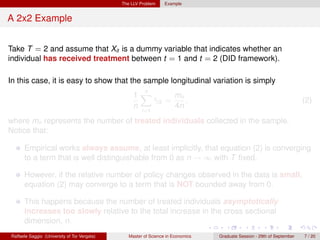

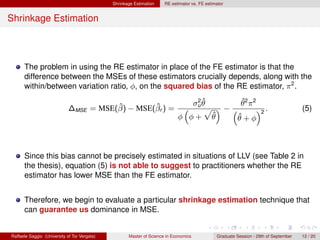

The Ordinary Ridge Estimator for FE Linear Panel Data Models

We demonstrate how, by applying the Ordinary Ridge Regression (ORR)

framework to our FE linear panel data context, it is possible to construct a

shrinkage estimator whose MSE always dominates, under appropriate

conditions, the MSE of the FE estimator.

In order to fully understand this last result, recall that when evaluating the ORR

estimator, Hoerl and Kennard (1970a, pp. 84) write: “[...] it would appear to be

impossible to choose a value of k = 0 (i.e. the ridge constant) and thus to achieve

a smaller mean square error without being able to assign an upper bound to β".

The crucial remark of this thesis is that the linear panel data framework does

provide, under appropriate conditions, this upper bound on β.

This boundedness assumption can be derived from the alternative linear panel

data estimators (i.e. the RE estimator, the BG estimator and the POLS estimator).

Raffaele Saggio (University of Tor Vergata) Master of Science in Economics Graduate Session - 29th of September 13 / 20](https://image.slidesharecdn.com/slidestvdef-12942276284925-phpapp02/85/Shrinkage-Estimation-of-Linear-Panel-Data-Models-Under-Nearly-Singular-Design-53-320.jpg)

![Shrinkage Estimation Ridge regression

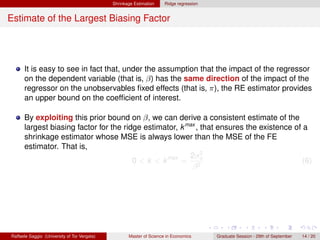

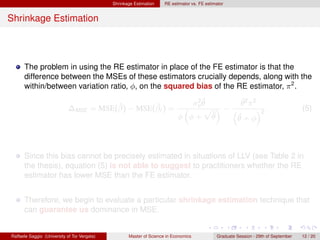

The Ordinary Ridge Estimator for FE Linear Panel Data Models

We demonstrate how, by applying the Ordinary Ridge Regression (ORR)

framework to our FE linear panel data context, it is possible to construct a

shrinkage estimator whose MSE always dominates, under appropriate

conditions, the MSE of the FE estimator.

In order to fully understand this last result, recall that when evaluating the ORR

estimator, Hoerl and Kennard (1970a, pp. 84) write: “[...] it would appear to be

impossible to choose a value of k = 0 (i.e. the ridge constant) and thus to achieve

a smaller mean square error without being able to assign an upper bound to β".

The crucial remark of this thesis is that the linear panel data framework does

provide, under appropriate conditions, this upper bound on β.

This boundedness assumption can be derived from the alternative linear panel

data estimators (i.e. the RE estimator, the BG estimator and the POLS estimator).

Raffaele Saggio (University of Tor Vergata) Master of Science in Economics Graduate Session - 29th of September 13 / 20](https://image.slidesharecdn.com/slidestvdef-12942276284925-phpapp02/85/Shrinkage-Estimation-of-Linear-Panel-Data-Models-Under-Nearly-Singular-Design-54-320.jpg)

![Shrinkage Estimation Ridge regression

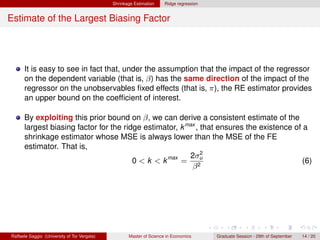

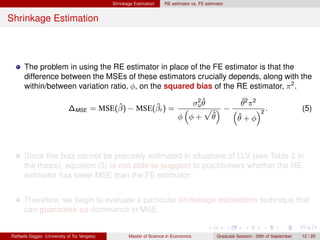

The Ordinary Ridge Estimator for FE Linear Panel Data Models

We demonstrate how, by applying the Ordinary Ridge Regression (ORR)

framework to our FE linear panel data context, it is possible to construct a

shrinkage estimator whose MSE always dominates, under appropriate

conditions, the MSE of the FE estimator.

In order to fully understand this last result, recall that when evaluating the ORR

estimator, Hoerl and Kennard (1970a, pp. 84) write: “[...] it would appear to be

impossible to choose a value of k = 0 (i.e. the ridge constant) and thus to achieve

a smaller mean square error without being able to assign an upper bound to β".

The crucial remark of this thesis is that the linear panel data framework does

provide, under appropriate conditions, this upper bound on β.

This boundedness assumption can be derived from the alternative linear panel

data estimators (i.e. the RE estimator, the BG estimator and the POLS estimator).

Raffaele Saggio (University of Tor Vergata) Master of Science in Economics Graduate Session - 29th of September 13 / 20](https://image.slidesharecdn.com/slidestvdef-12942276284925-phpapp02/85/Shrinkage-Estimation-of-Linear-Panel-Data-Models-Under-Nearly-Singular-Design-55-320.jpg)

![Shrinkage Estimation Ridge regression

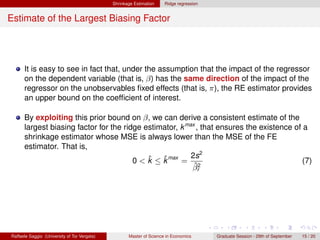

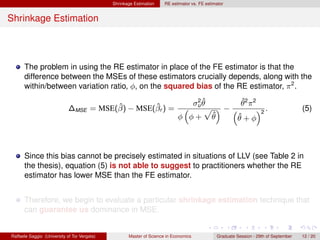

The Ordinary Ridge Estimator for FE Linear Panel Data Models

We demonstrate how, by applying the Ordinary Ridge Regression (ORR)

framework to our FE linear panel data context, it is possible to construct a

shrinkage estimator whose MSE always dominates, under appropriate

conditions, the MSE of the FE estimator.

In order to fully understand this last result, recall that when evaluating the ORR

estimator, Hoerl and Kennard (1970a, pp. 84) write: “[...] it would appear to be

impossible to choose a value of k = 0 (i.e. the ridge constant) and thus to achieve

a smaller mean square error without being able to assign an upper bound to β".

The crucial remark of this thesis is that the linear panel data framework does

provide, under appropriate conditions, this upper bound on β.

This boundedness assumption can be derived from the alternative linear panel

data estimators (i.e. the RE estimator, the BG estimator and the POLS estimator).

Raffaele Saggio (University of Tor Vergata) Master of Science in Economics Graduate Session - 29th of September 13 / 20](https://image.slidesharecdn.com/slidestvdef-12942276284925-phpapp02/85/Shrinkage-Estimation-of-Linear-Panel-Data-Models-Under-Nearly-Singular-Design-56-320.jpg)