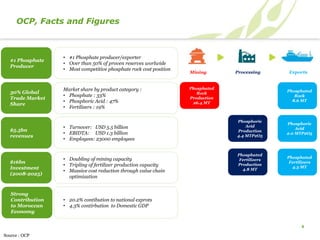

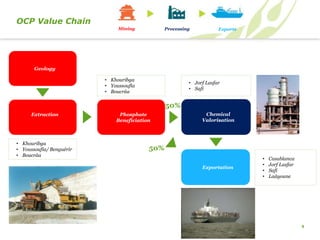

OCP is the world's leading phosphate producer and exporter, controlling approximately 30% of the global phosphate trade market. A $16 billion investment program from 2008-2025 aims to double OCP's mining capacity, triple fertilizer production capacity, and optimize costs across the phosphate value chain. Key elements of the investment plan include expanding mines and building new beneficiation plants, slurry pipelines to transport phosphate rock, and developing world-class chemical platforms at Jorf Lasfar and Safi to increase integrated fertilizer production. This will position OCP to continue meeting rising global demand for phosphate-based fertilizers needed to sustainably increase agricultural productivity and address the growing global food demand.