Downloaded 97 times

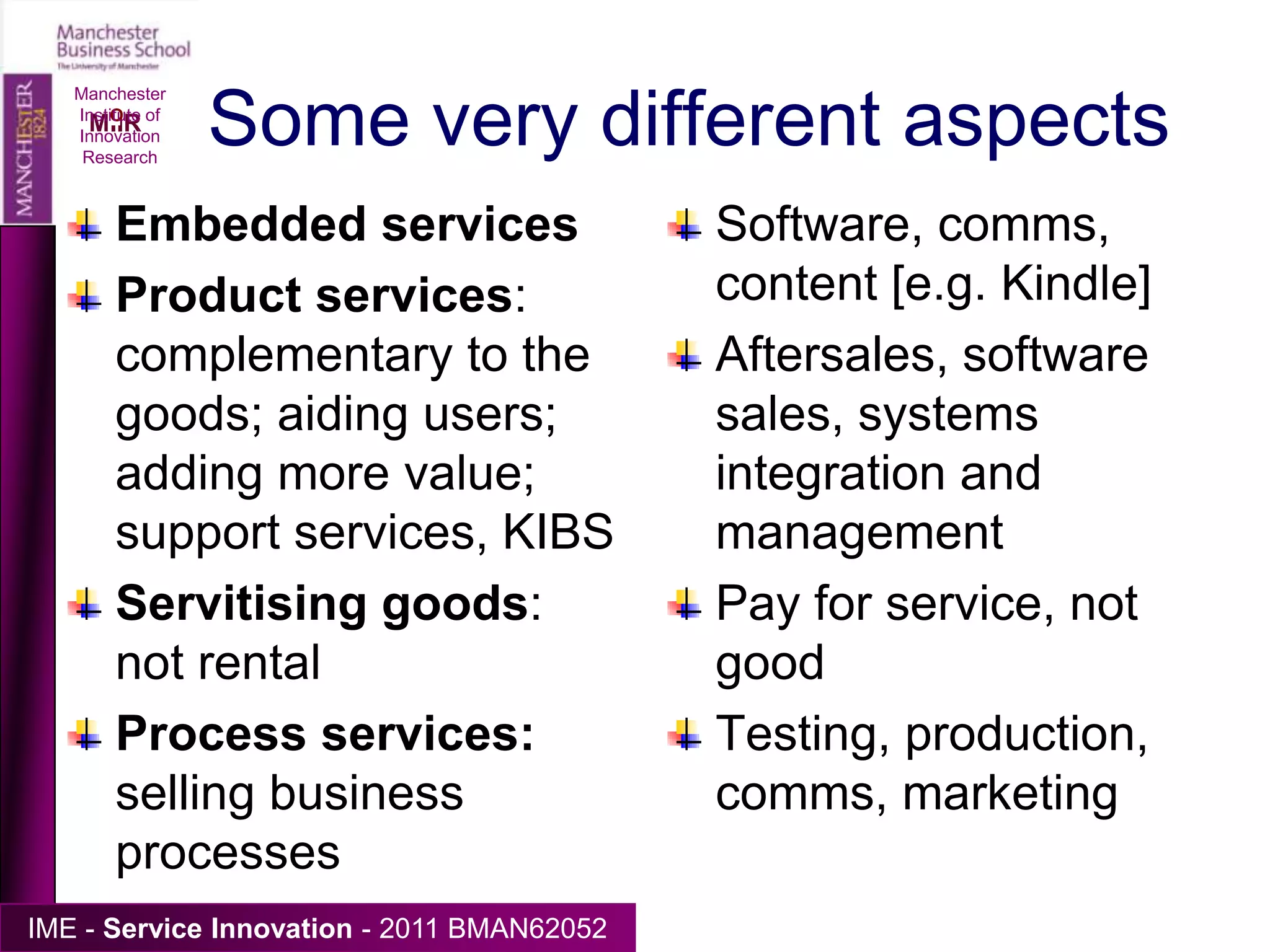

![Some very different aspectsEmbedded servicesProduct services: complementary to the goods; aiding users; adding more value; support services, KIBSServitising goods: not rentalProcess services: selling business processesSoftware, comms, content [e.g. Kindle]Aftersales, software sales, systems integration and managementPay for service, not goodTesting, production, comms, marketingManchester Institute of Innovation Research](https://image.slidesharecdn.com/2011serinnbman620528digital-110322082840-phpapp02/75/servicisation-and-digital-convergence-2011-12-2048.jpg)

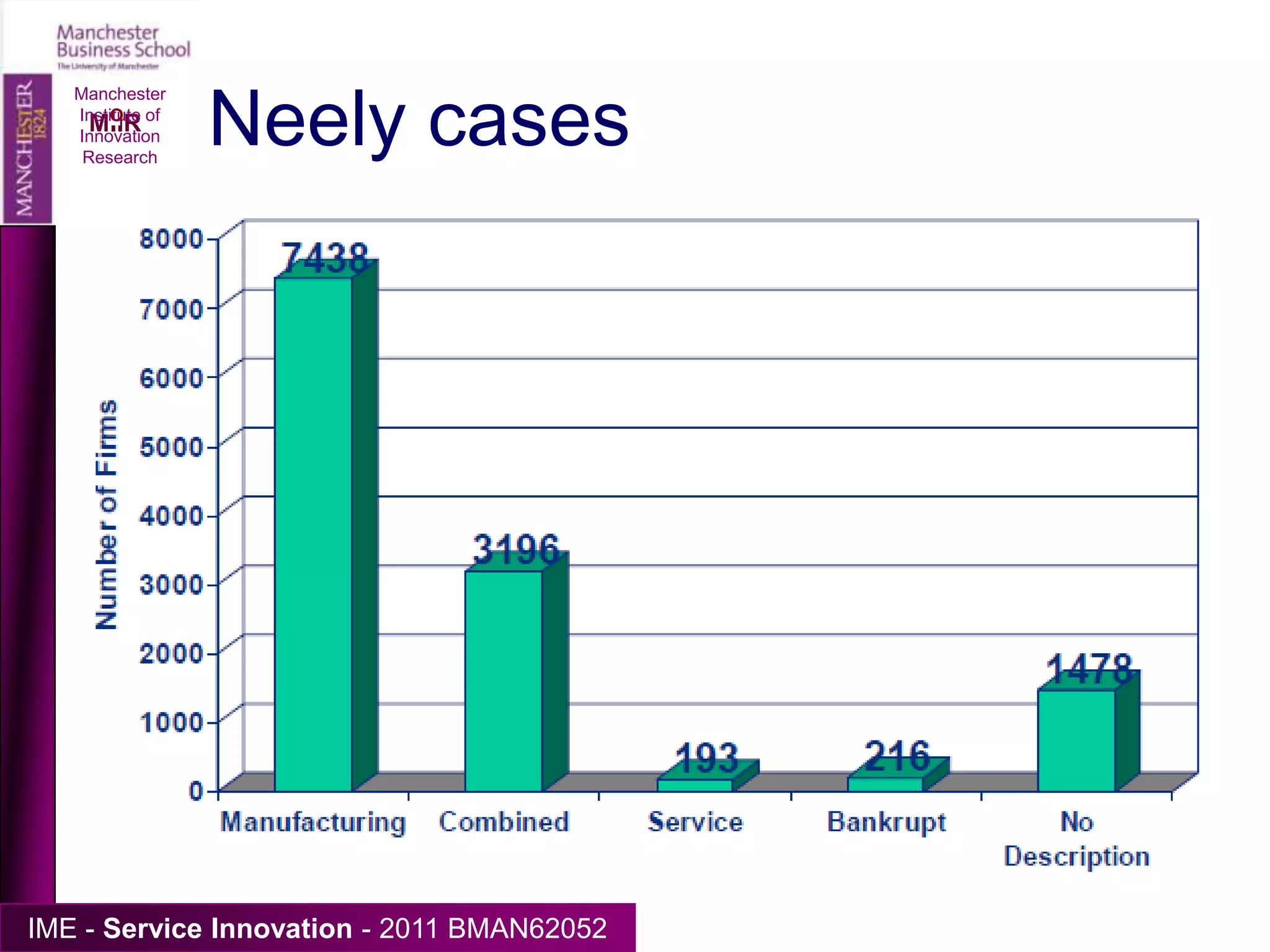

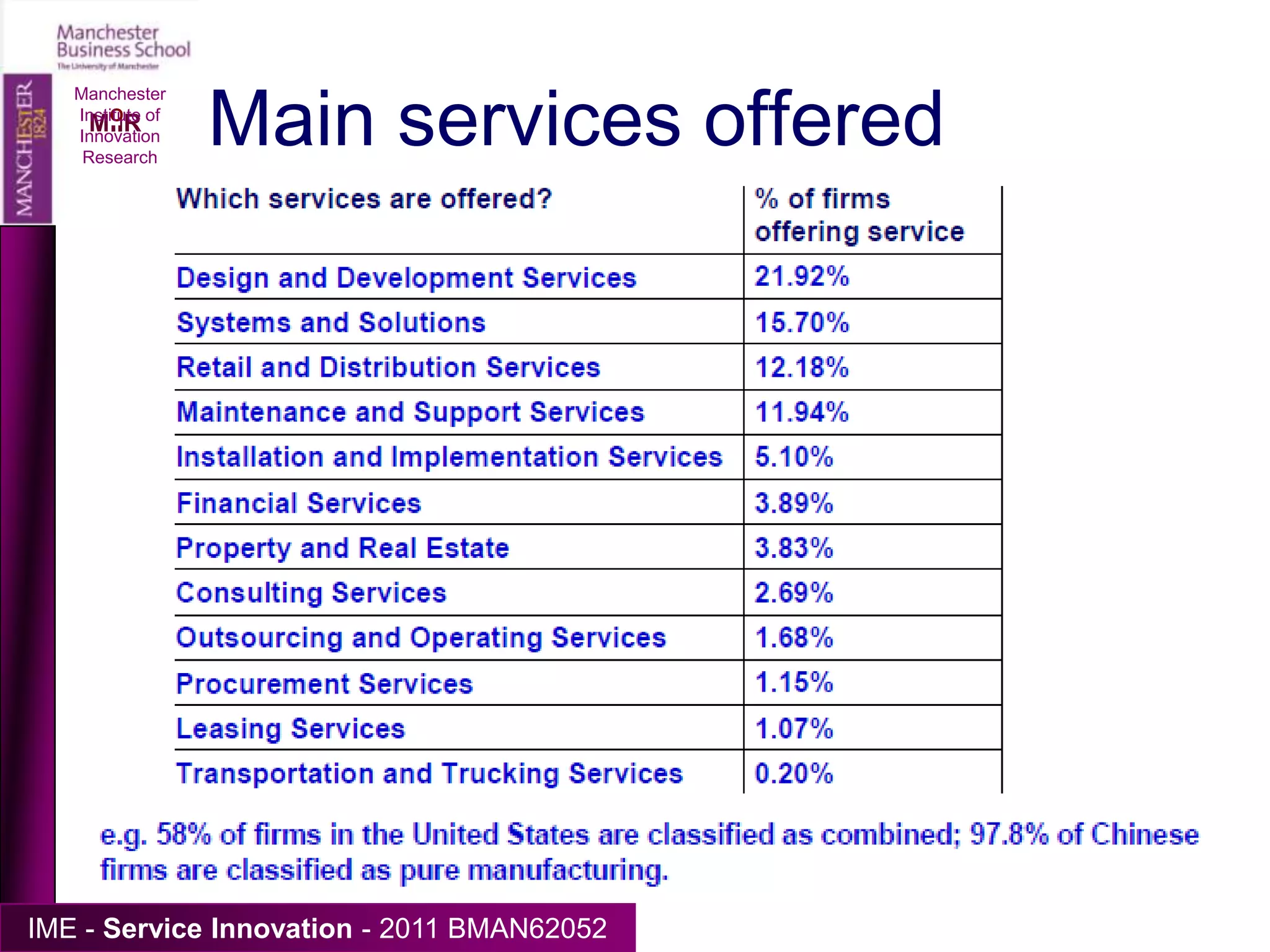

![Large-scale analysis is rareManchester Institute of Innovation ResearchAn exception: Andy Neely ‘The Servitization of Manufacturing: An Analysis of Global Trends’Data from OSIRIS [44,000 listed companies from around the world].](https://image.slidesharecdn.com/2011serinnbman620528digital-110322082840-phpapp02/75/servicisation-and-digital-convergence-2011-23-2048.jpg)

![Companies with primary or secondary US SIC codes in the range 10-39 inclusive, extractive & manufacturing, and over 100 employees [n=12,521].1.Pure manufacturingPetroChina principally engaged in a broad range of petroleum & natural gas-related activities.2.Some combination of manufacturing & serviceSiemens -predominantly electronics & electrical engineering, but provides wide variety of consulting, maintenance & other services.3.Pure serviceThe Brink's Company: security industry firm - services offered include armoured-car transportation, automated teller machine (ATM) servicing, currency & deposit processing, coin sorting & wrapping, & arranging secure air transportation of valuables.Three models](https://image.slidesharecdn.com/2011serinnbman620528digital-110322082840-phpapp02/75/servicisation-and-digital-convergence-2011-24-2048.jpg)

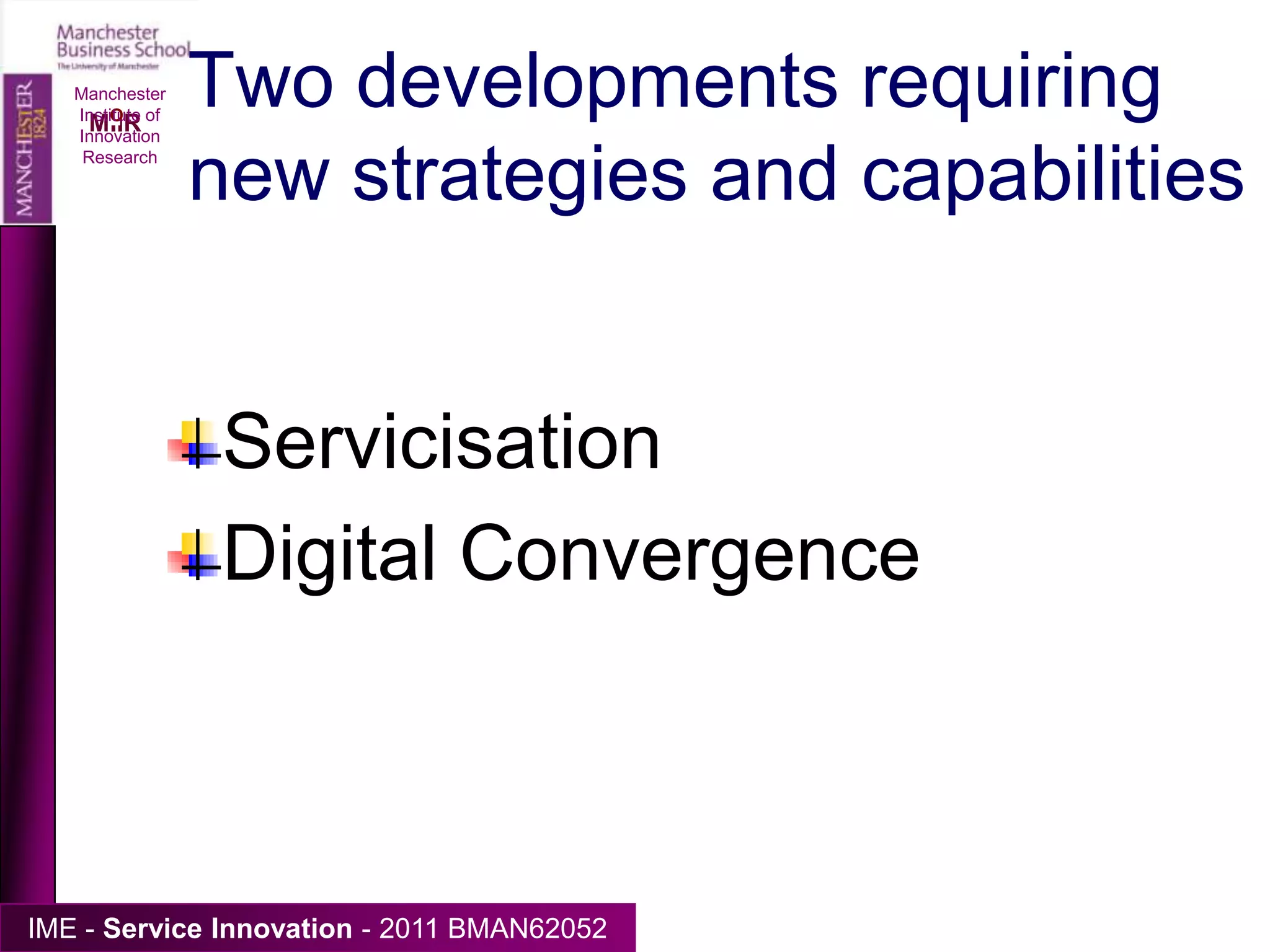

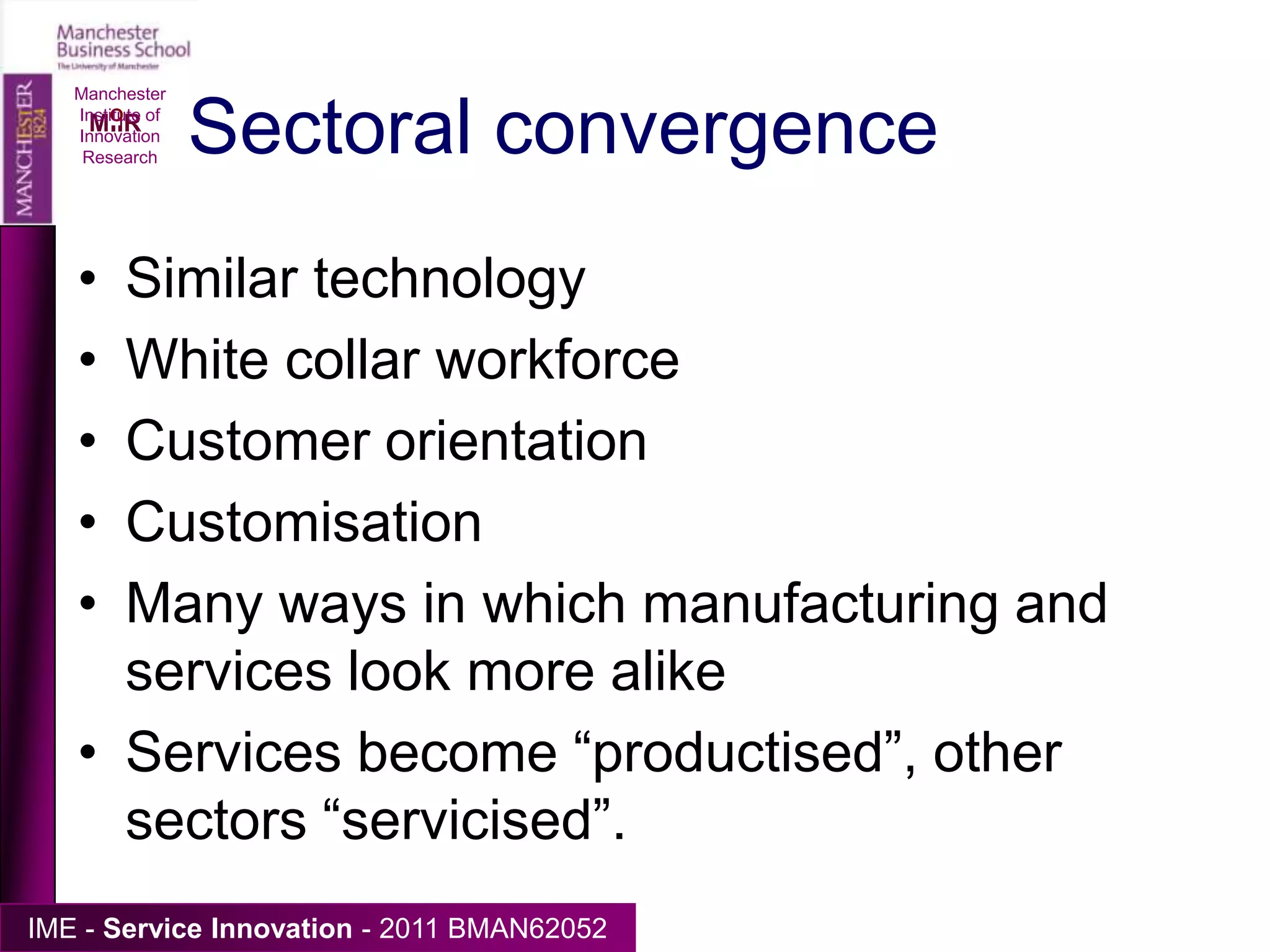

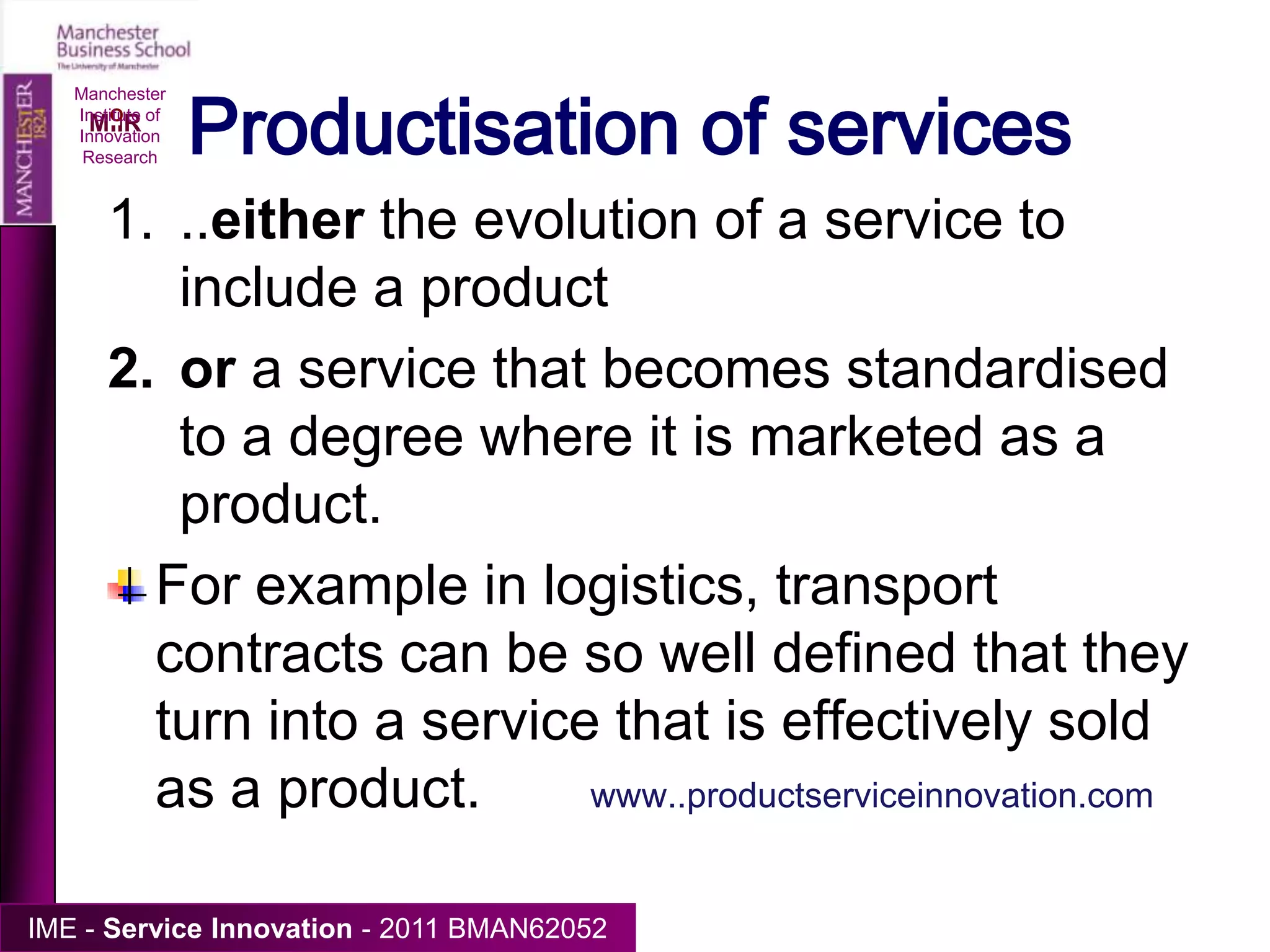

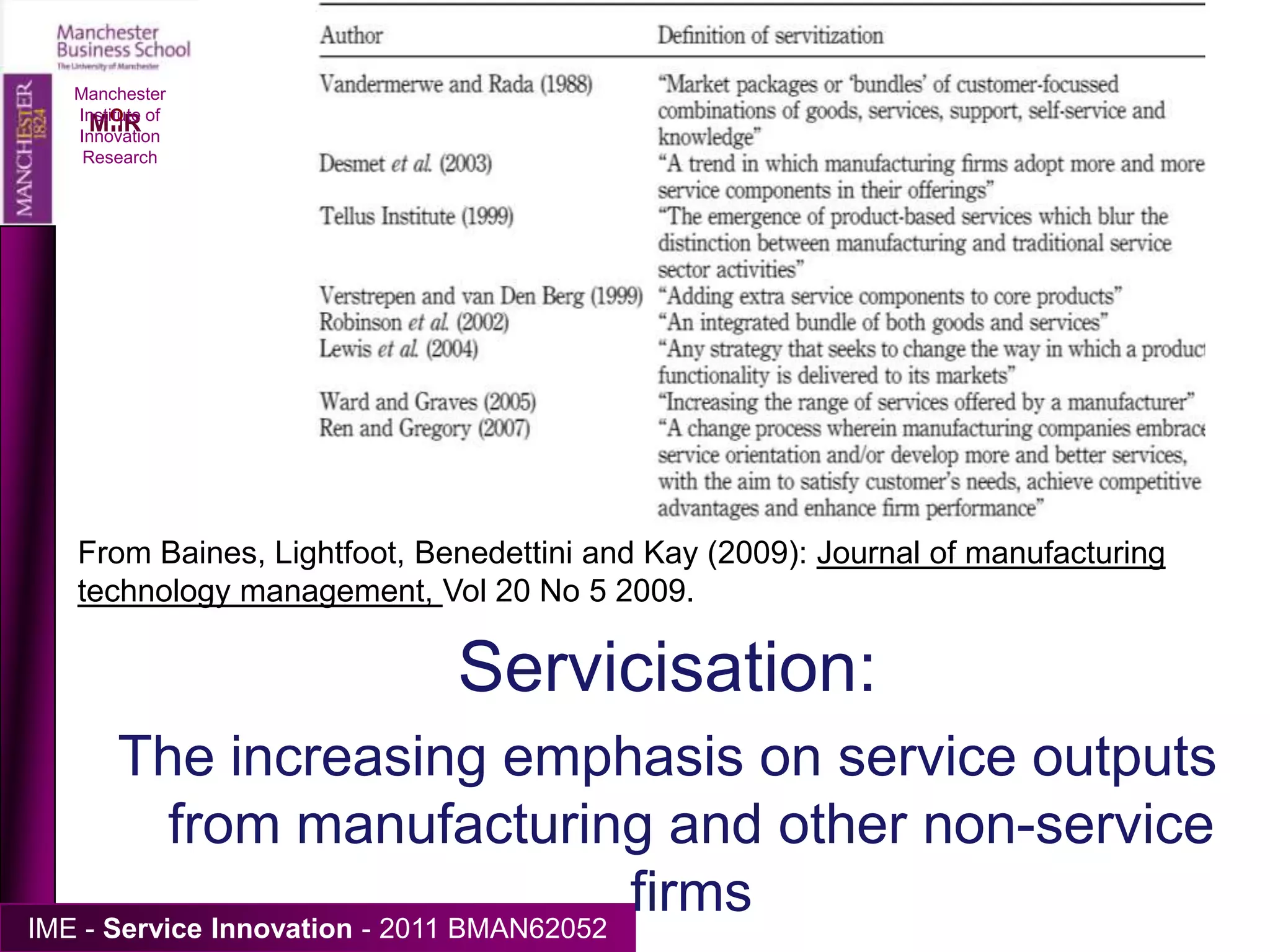

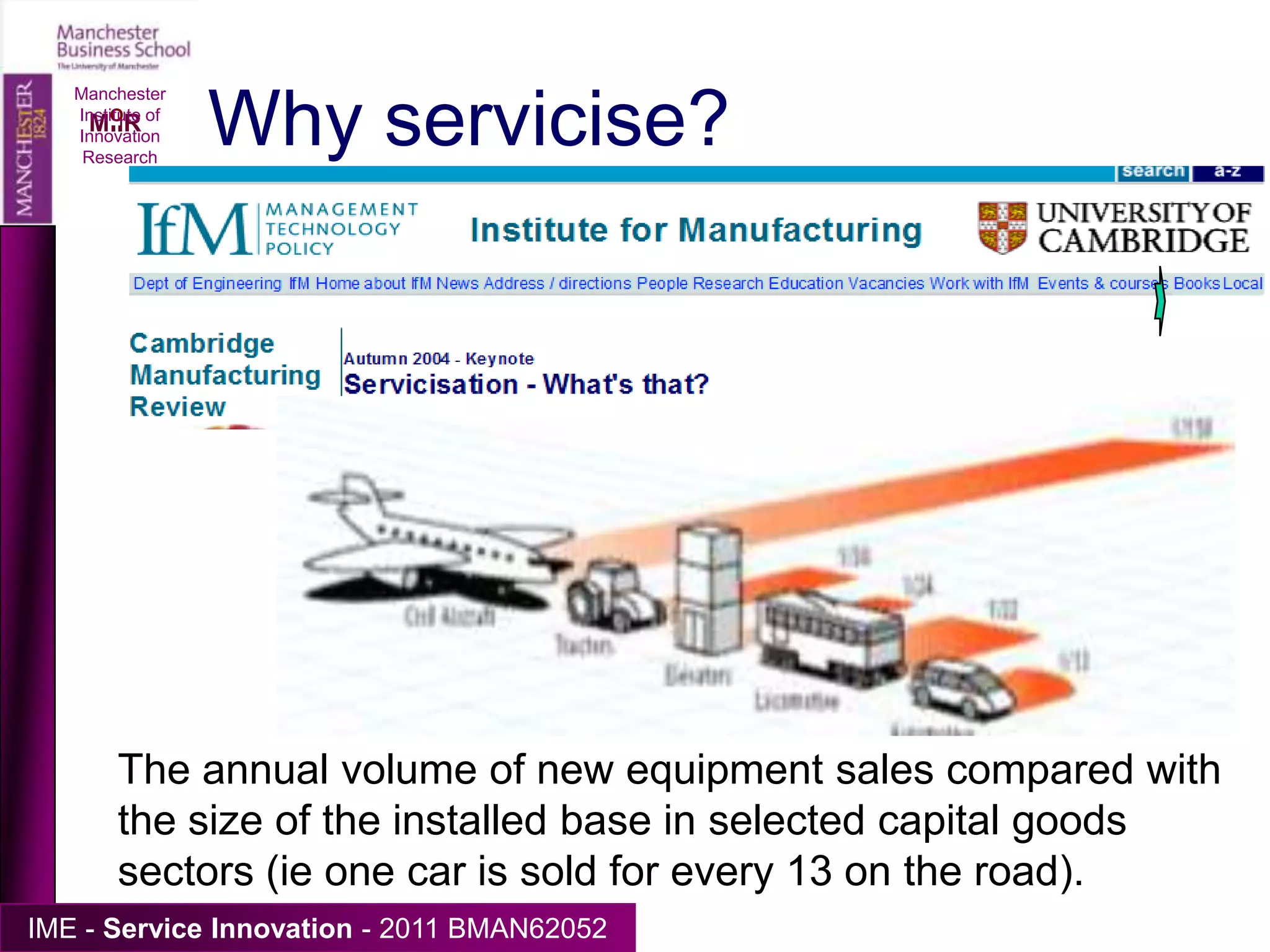

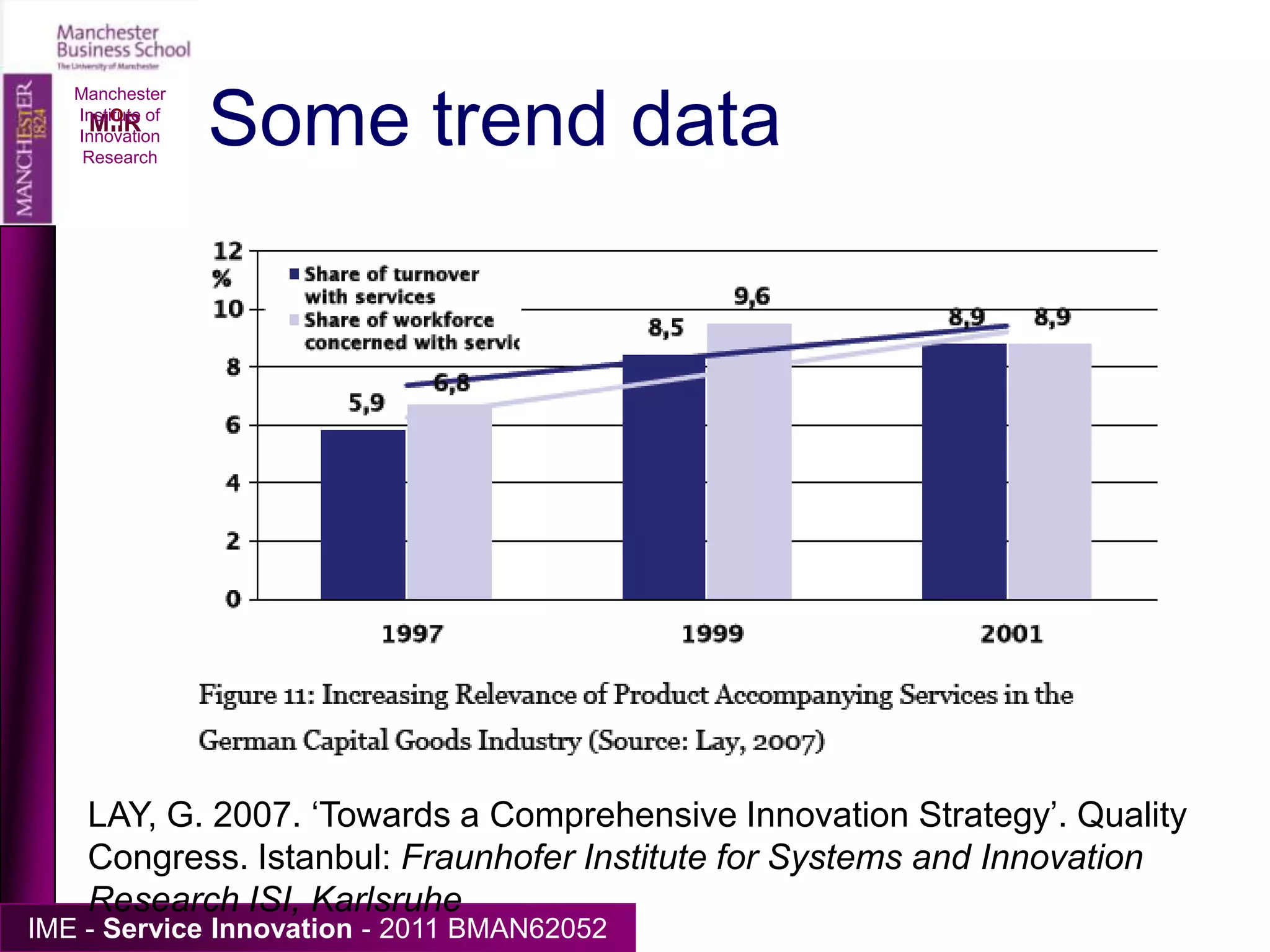

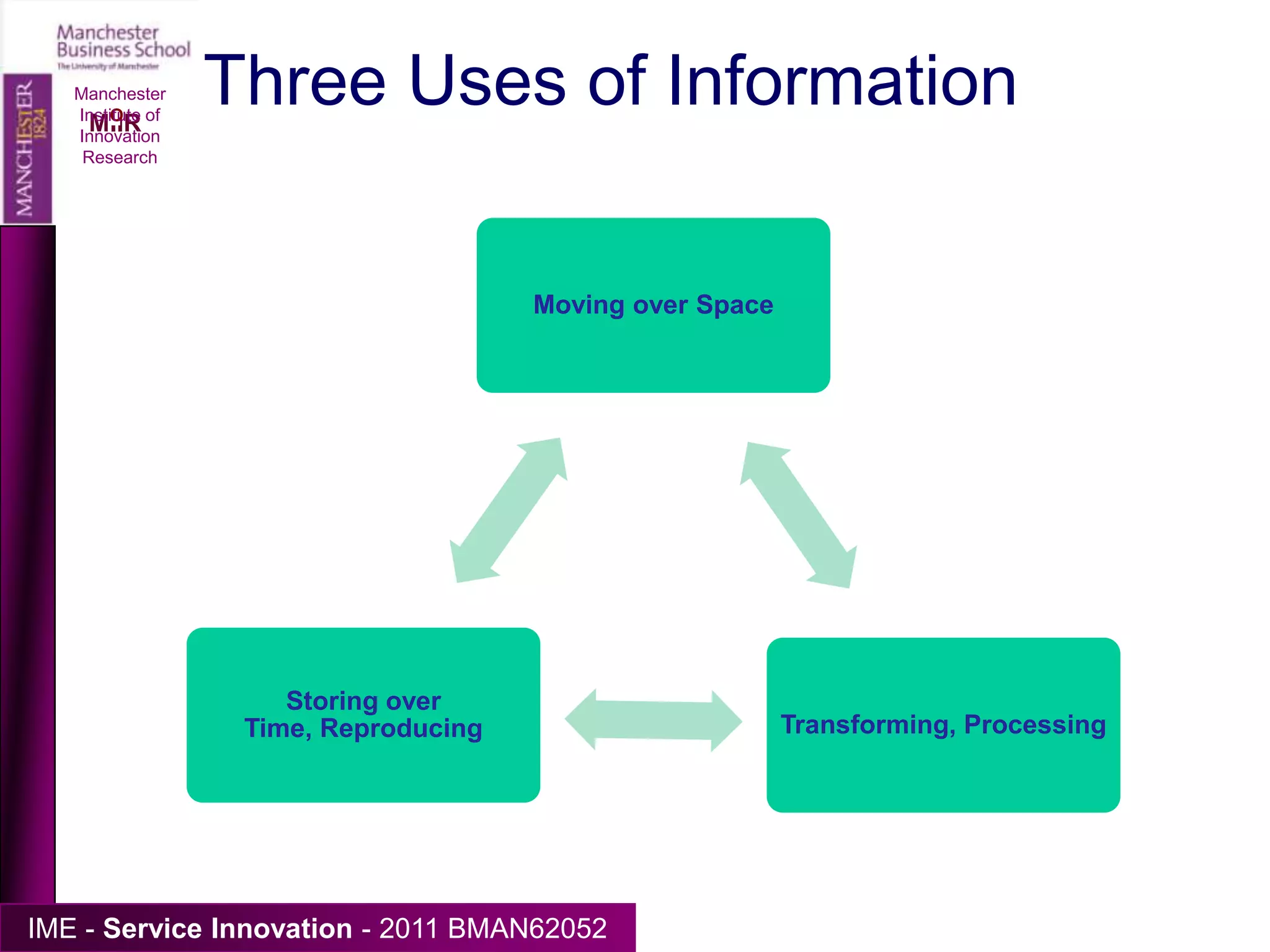

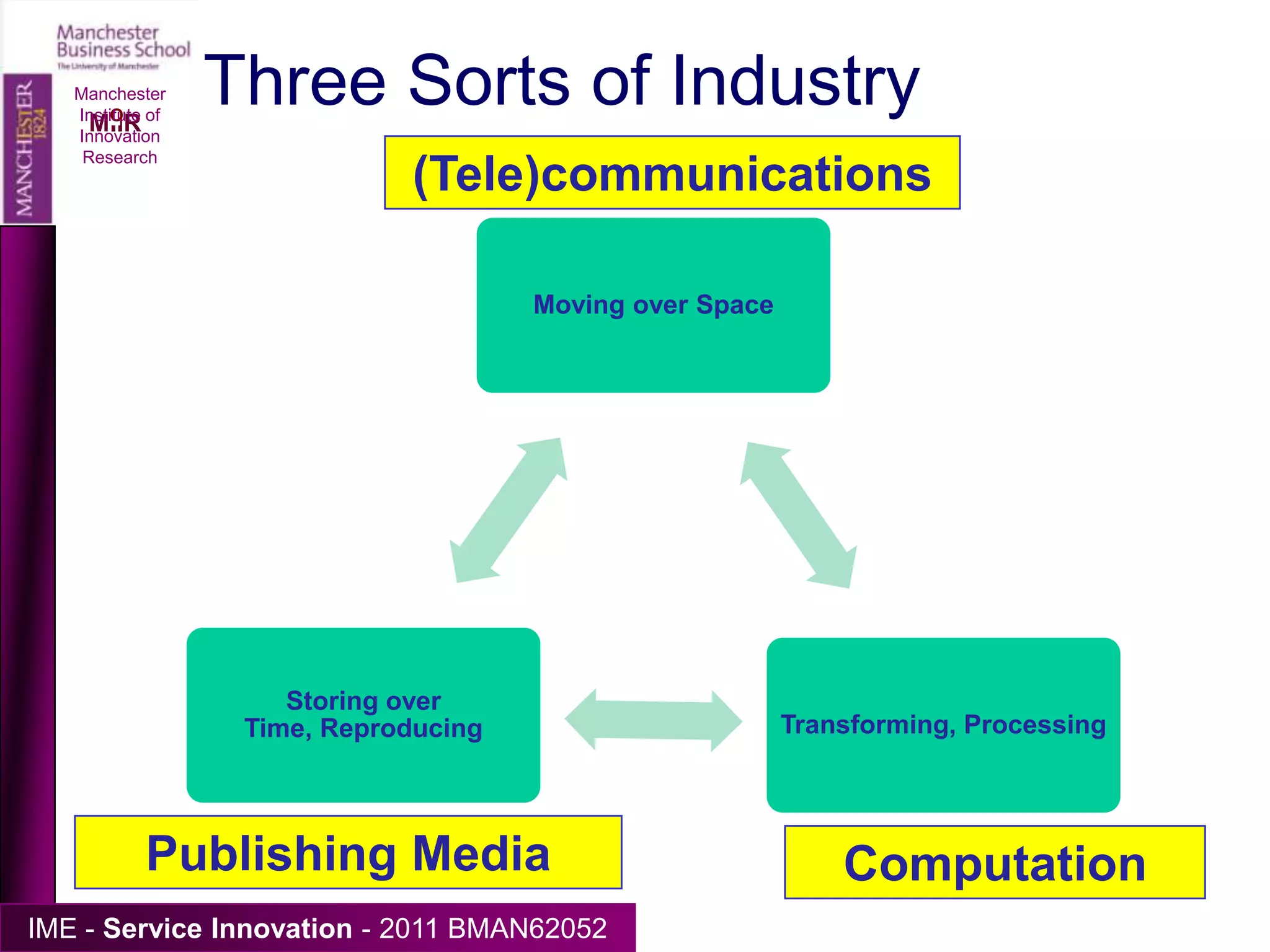

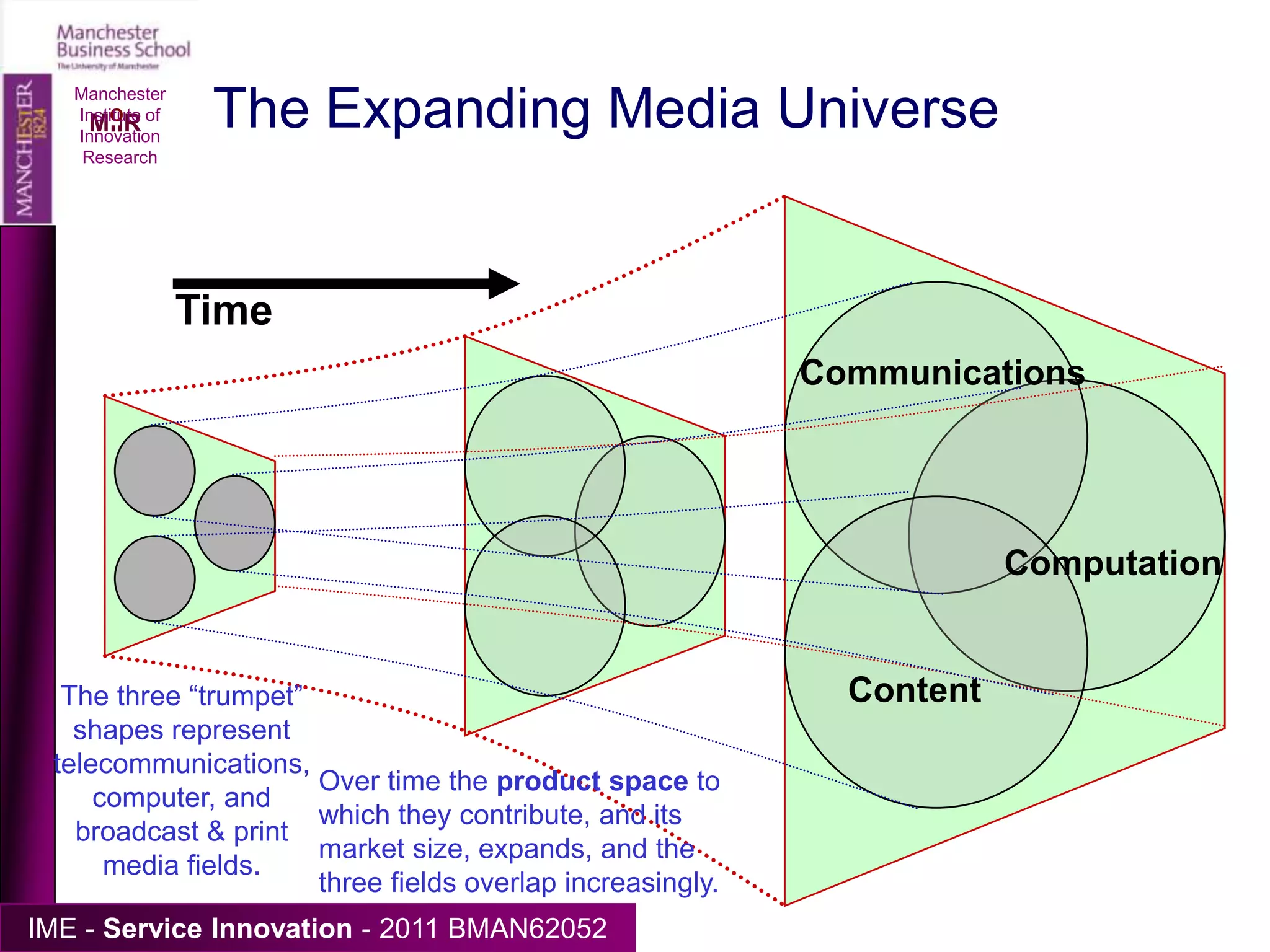

This document discusses two developments requiring new strategies and capabilities: servicisation and digital convergence. It provides background on both topics, including how servicisation involves manufacturing firms increasingly offering services and how digital convergence involves the merging of previously separate industries like publishing, media, IT, and telecommunications due to shared digital technologies. The document also discusses challenges involved in these transitions and provides examples of firms that have adapted to these changes.