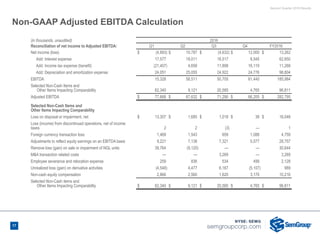

This document summarizes SemGroup's second quarter 2018 earnings conference call. It discusses non-GAAP financial measures used by SemGroup like Adjusted EBITDA, Cash Available for Dividends, and Total Segment Profit. It provides definitions of these terms and notes that they are not substitutes for GAAP measures but are used by management to evaluate performance. The document also contains forward-looking statements about SemGroup's prospects, plans, and financial performance that are based on current expectations and assumptions which involve risks and uncertainties.