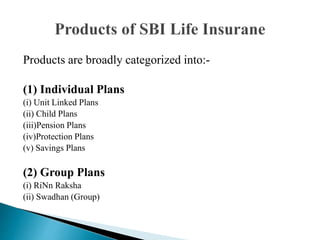

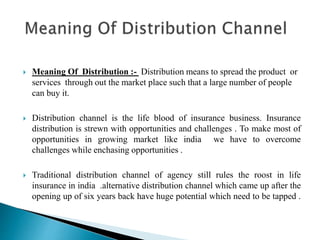

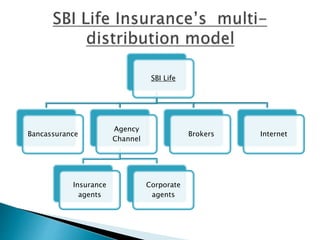

The document discusses insurance and its types. It defines insurance as a contract between an insurance company and a policyholder, where the insurer agrees to pay a specified amount if a specified event occurs. Insurance is divided into life insurance, which covers human lives, and non-life (general) insurance, which covers other assets. The document then discusses SBI Life Insurance, its joint venture with State Bank of India and Cardif SA, and its various individual and group insurance products.