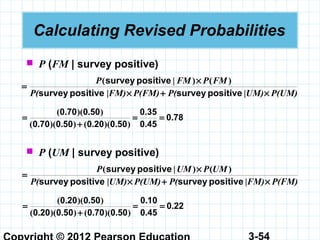

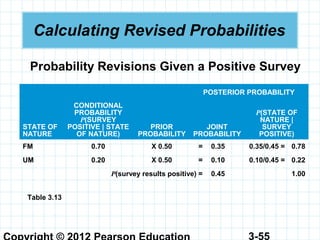

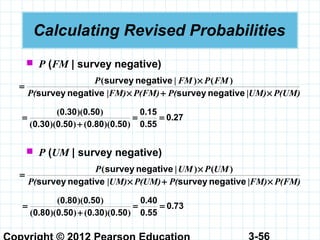

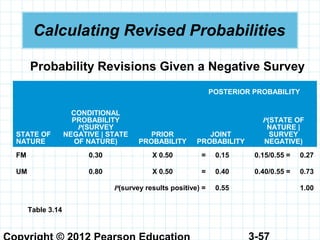

Downloaded 59 times

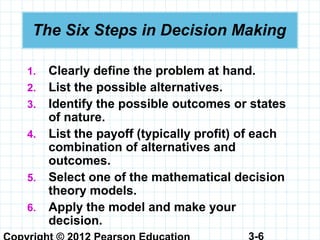

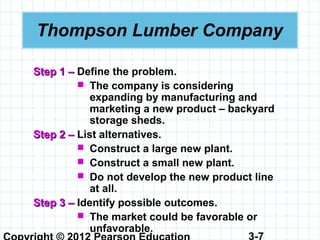

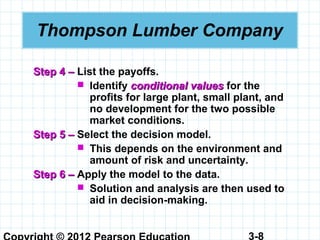

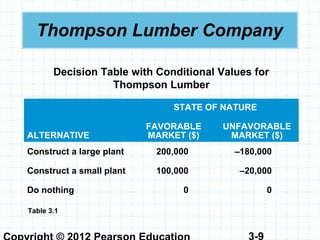

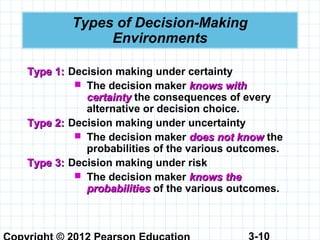

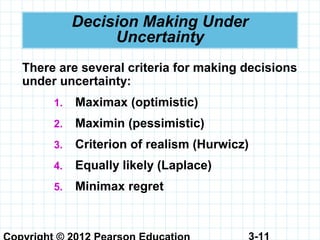

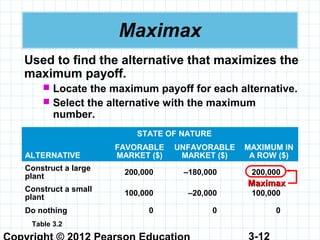

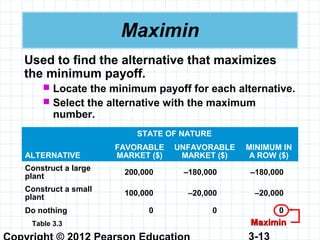

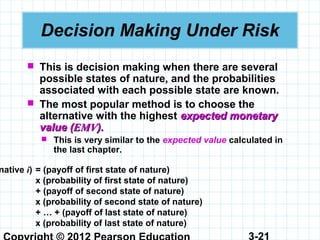

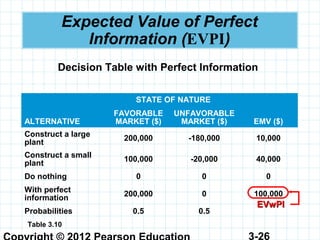

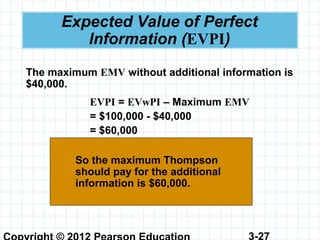

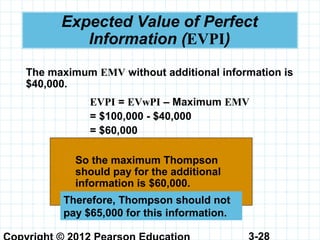

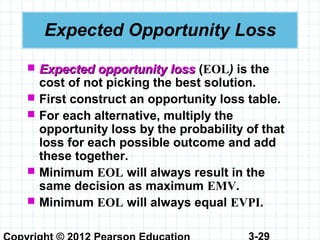

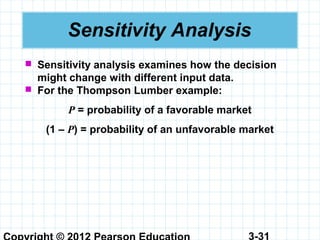

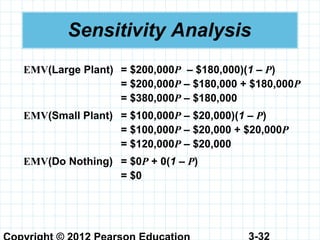

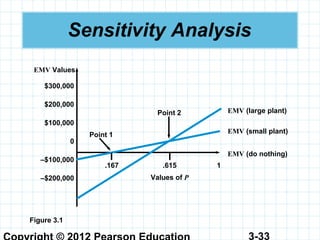

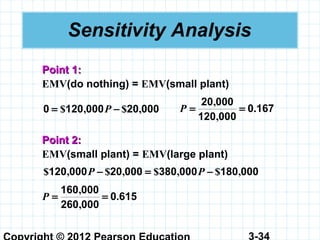

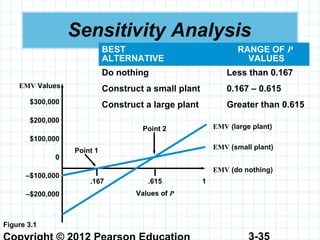

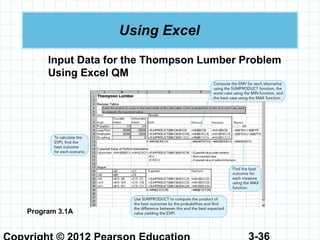

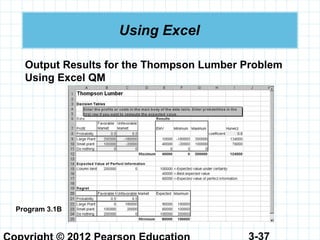

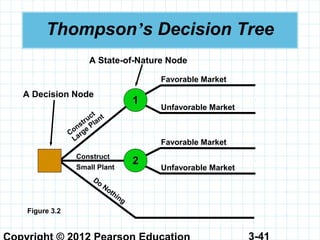

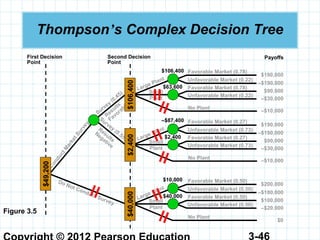

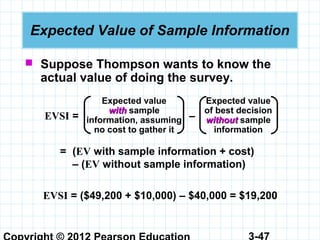

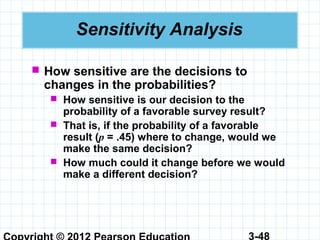

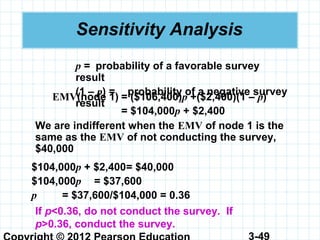

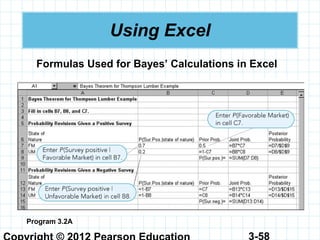

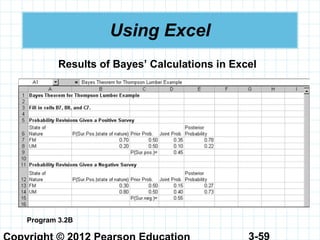

This document outlines the key concepts and steps involved in decision analysis and decision making under uncertainty. It discusses the six steps in decision making, types of decision making environments, and methods for making decisions under uncertainty, risk, and with imperfect information. These methods include maximax, maximin, Hurwicz criterion, equally likely, minimax regret, expected monetary value, expected value of perfect information, and expected opportunity loss. An example involving a company called Thompson Lumber is used to illustrate applying these decision making techniques. Sensitivity analysis is also discussed as a way to examine how the optimal decision may change with different input data.