Ron and Chelsea Jade have provided the following information for you.docx

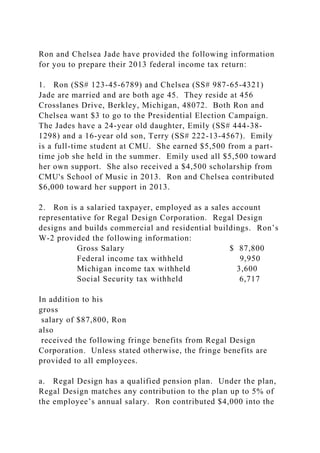

Ron and Chelsea Jade have provided the following information for you to prepare their 2013 federal income tax return: 1. Ron (SS# 123-45-6789) and Chelsea (SS# 987-65-4321) Jade are married and are both age 45. They reside at 456 Crosslanes Drive, Berkley, Michigan, 48072. Both Ron and Chelsea want $3 to go to the Presidential Election Campaign. The Jades have a 24-year old daughter, Emily (SS# 444-38-1298) and a 16-year old son, Terry (SS# 222-13-4567). Emily is a full-time student at CMU. She earned $5,500 from a part-time job she held in the summer. Emily used all $5,500 toward her own support. She also received a $4,500 scholarship from CMU's School of Music in 2013. Ron and Chelsea contributed $6,000 toward her support in 2013. 2. Ron is a salaried taxpayer, employed as a sales account representative for Regal Design Corporation. Regal Design designs and builds commercial and residential buildings. Ron’s W-2 provided the following information: Gross Salary $ 87,800 Federal income tax withheld 9,950 Michigan income tax withheld 3,600 Social Security tax withheld 6,717 In addition to his gross salary of $87,800, Ron also received the following fringe benefits from Regal Design Corporation. Unless stated otherwise, the fringe benefits are provided to all employees. a. Regal Design has a qualified pension plan. Under the plan, Regal Design matches any contribution to the plan up to 5% of the employee’s annual salary. Ron contributed $4,000 into the plan; his contribution was matched by Regal Design. Ron’s pension plan account earned $800 in ordinary dividends during the year. b. Regal Design paid 100% of the premiums for Ron and his dependents to be covered under a Blue Cross/Blue Shield corporate medical insurance policy (cost of premiums - $3,500). Ron received $3,200 in reimbursements from the plan for his family medical expenses. c. Regal Design provides employees with a flexible benefits plan. Ron had $1,500 withheld from his salary, which was paid into the plan during the year. The amount of his family’s medical, dental, and optometry costs not reimbursed by insurance totaled $1,800. The flexible benefits plan reimbursed him for $1,500 of the $1,800 in additional expenses. d. Regal Design paid 100% of the premiums on a group-term life insurance policy for Ron. He named Chelsea as beneficiary. Face value of the policy is $160,000. The group-term life insurance coverage for Ron cost Regal Design $375. e. Regal Design paid 100% of the premiums on a corporate disability insurance policy for Ron. The disability insurance coverage for Ron cost Regal Design $650. f. During the year, Regal Design provided Ron with free retirement planning services from Fidelity Investments. The value of the services Ron and Chelsea received from Fidel.

Recommended

Recommended

More Related Content

Similar to Ron and Chelsea Jade have provided the following information for you.docx

Similar to Ron and Chelsea Jade have provided the following information for you.docx (20)

More from daniely50

More from daniely50 (20)

Recently uploaded

Recently uploaded (20)

Ron and Chelsea Jade have provided the following information for you.docx

- 1. Ron and Chelsea Jade have provided the following information for you to prepare their 2013 federal income tax return: 1. Ron (SS# 123-45-6789) and Chelsea (SS# 987-65-4321) Jade are married and are both age 45. They reside at 456 Crosslanes Drive, Berkley, Michigan, 48072. Both Ron and Chelsea want $3 to go to the Presidential Election Campaign. The Jades have a 24-year old daughter, Emily (SS# 444-38- 1298) and a 16-year old son, Terry (SS# 222-13-4567). Emily is a full-time student at CMU. She earned $5,500 from a part- time job she held in the summer. Emily used all $5,500 toward her own support. She also received a $4,500 scholarship from CMU's School of Music in 2013. Ron and Chelsea contributed $6,000 toward her support in 2013. 2. Ron is a salaried taxpayer, employed as a sales account representative for Regal Design Corporation. Regal Design designs and builds commercial and residential buildings. Ron’s W-2 provided the following information: Gross Salary $ 87,800 Federal income tax withheld 9,950 Michigan income tax withheld 3,600 Social Security tax withheld 6,717 In addition to his gross salary of $87,800, Ron also received the following fringe benefits from Regal Design Corporation. Unless stated otherwise, the fringe benefits are provided to all employees. a. Regal Design has a qualified pension plan. Under the plan, Regal Design matches any contribution to the plan up to 5% of the employee’s annual salary. Ron contributed $4,000 into the

- 2. plan; his contribution was matched by Regal Design. Ron’s pension plan account earned $800 in ordinary dividends during the year. b. Regal Design paid 100% of the premiums for Ron and his dependents to be covered under a Blue Cross/Blue Shield corporate medical insurance policy (cost of premiums - $3,500). Ron received $3,200 in reimbursements from the plan for his family medical expenses. c. Regal Design provides employees with a flexible benefits plan. Ron had $1,500 withheld from his salary, which was paid into the plan during the year. The amount of his family’s medical, dental, and optometry costs not reimbursed by insurance totaled $1,800. The flexible benefits plan reimbursed him for $1,500 of the $1,800 in additional expenses. d. Regal Design paid 100% of the premiums on a group-term life insurance policy for Ron. He named Chelsea as beneficiary. Face value of the policy is $160,000. The group- term life insurance coverage for Ron cost Regal Design $375. e. Regal Design paid 100% of the premiums on a corporate disability insurance policy for Ron. The disability insurance coverage for Ron cost Regal Design $650. f. During the year, Regal Design provided Ron with free retirement planning services from Fidelity Investments. The value of the services Ron and Chelsea received from Fidelity was $200. g. Regal Design allows all employees to purchase building design services from the company at a 35% discount. Ron had Regal Design design a new home the Jades are planning to build. The design service was valued at $2,000, so with his discount, Ron paid Regal Design $1,300.

- 3. h. Ron took four MBA courses this year. Since he earned an A in each of the courses, Regal Design's educational assistance program reimbursed $6,300 of the tuition he paid for the courses. i. Ron also received certain other fringe benefits not available to all employees. He received free parking for the entire year in the company’s security garage that would normally cost $250 per month. In addition, Regal Design paid $850 of his professional association dues and professional magazine subscriptions. Regal Design also paid Ron’s $325 annual dues to a health club owned and operated by Beaumont Hospital. The health club is located in the same building as his office. 3. Ron slipped on an icy spot in front of a grocery store during the current year and broke his hip. He was unable to work for three weeks and incurred $4,100 in medical costs, all of which were paid by the owner of the store. The store also gave him $800 for pain and suffering resulting from the injury. For the time he was unable to work, Regal Design Corporation’s disability plan paid him $3,000 in disability income. A disability policy Ron owned individually paid him an additional $1,250 in disability income (Ron pays the premiums on this disability insurance). 4. Ron and Chelsea earned the following in interest and dividend income per the 1099 forms they received from the various financial institutions. 100% of all ordinary dividends are also qualified dividends. Dividends: Quantum Corporation (100% ordinary dividend) $ 750 T Rowe Price Health Sciences Mutual Fund (100% capital gain distribution) 400

- 4. Consumers Energy (30% return of capital dividend) 550 Northwestern Mutual Life (dividend on Ron’s 450 life insurance policy) Biogen Corporation - 50 shares of common stock (Stock had a FMV of $5/share on the date of distribution; all shareholders were able to take their distribution in the form of stock or cash; Ron chose to receive 50 shares of stock) Interest: PNC Bank $ 60 State of Illinois bonds 475 City of Toronto, Canada bonds 250 U.S. Series EE Savings Bonds (redeemed for $4,250, 3,750 purchased in 1994 for $2,000; interest income has never been reported on the bonds; proceeds were used to purchase furniture) 5. The Jades had no type of ownership interest or authority over any financial account in any foreign country, including any type of foreign trust. 6. Chelsea owns 700 shares of Grubstake Mining & Development common stock. Grubstake is organized as a S corporation and has 35,000 shares outstanding. Grubstake reported total current year ordinary business income of

- 5. $600,000 and total regular interest income of $42,000. In addition, Grubstake paid dividends of $1 per share during the current year, so Chelsea received a dividend of $700. All her investment in Grubstake is “at-risk.” Grubstake is a passive activity investment for Chelsea. 7. Chelsea's father died last year. In addition to receiving $300,000 in cash as an inheritance from her father’s estate when the estate was settled this year, she was also designated beneficiary of a $200,000 life insurance policy on the life of her father. Chelsea elected to receive the life insurance proceeds in annual payments of $21,600 over 10 years. She received the first annual payment of $21,600 on January 1, 2013. 8. The Jades received a 2012 federal income tax refund of $1,050 on May 12, 2013. On May 17, 2013, they received their 2012 income tax refund from the State of Michigan of $825. Their total itemized deductions in 2012 was $17,800. 9. Chelsea’s name was drawn at the 2013 Home and Garden Show and she won $100 in cash and a new refrigerator. In announcing the prize at the Show, the announcer said the refrigerator had a manufacturer’s suggested retail price of $1,500. However, Ron has a sales flyer from ABC Warehouse that advertises the same refrigerator for $1,300. 10. Ron is active in the local chapter of the Michigan Audubon Society. During the year, he received an award for outstanding service to the organization. He was given a plaque and a $50 gift certificate that was donated to the chapter by local store merchants. 11. Ron received an award for 2013 Salesperson of the Year from Regal Design at its annual 4th of July employee picnic. His award was a new fishing set, which sold for $250 at MC

- 6. Sports. 12. Ron won $550 at the slots and $300 at bingo on his annual Michigan casino tour this year, but he lost $1,100 at roulette at the Soaring Eagle casino. He did win $400 in the office March Madness Basketball pool this year, although he paid $75 to join the pool. 13. Ron and Chelsea purchased a 15-year annuity for $225,000 in 2000 when Chelsea quit work to become a stay-at-home mom. The annuity pays them $1,470 per month. They received $17,640 in total monthly annuity payments this year. 14. Ron and Chelsea received a Form 1099-B from their broker for the sale of the following securities during the year: Security Sale Date Purchase Date Sales Price Commission Paid on Sale Tax Basis State of Illinois Bonds 4/19/13 2/19/09 $14,550 $550

- 7. $10,400 300 shares of Quantum Corporation stock 10/29/13 2/10/13 $5,880 $280 $3,500 250 shares of West Corporation stock 1/1/13 9/8/11 $2,200 $200 ** **The Jades purchased 600 shares of stock in West Corporation for $7,560 on September 8, 2011. Shortly after the purchase,

- 8. they received a nontaxable 40% stock dividend of 240 additional shares. 15. The Jades sold their 2008 Buick LaCrosse for $8,000 on September 5, 2013 to an unrelated buyer. They purchased the car on July 8, 2010, for $15,000. 16. Ron and Chelsea’s personal records disclose the following expenditures during the current year: Lawn care and snow removal services for home $ 1,300 Charitable contributions to First United Church 6,100 Interest on home mortgage 7,775 Real estate taxes on home 3,300 Utilities paid on home 4,200 Purchase of home furniture 4,250 17. The Jades made $1,400 in total 2013 estimated federal income tax payments and $600 in total 2013 estimated Michigan income tax payments as follows: a. The federal estimated income tax payments were paid as follows: (1) $350 on April 15, 2013; (2) $350 on June 15, 2013; (3) $350 on September 15, 2013: and (4) $350 on January 15, 2014. b. The Michigan estimated income tax payments were paid as follows: (1) $150 on April 15, 2013; (2) $150 on June 15,

- 9. 2013; (3) $150 on September 15, 2013: and (4) $150 on December 15, 2013. REOUIRED: 1. Complete Ron and Chelsea’s federal income tax return for 2013. You will need to complete Forms 1040, Schedule A, Schedule B, Schedule D, Form 8949, and Schedule E. Despite what any line on a form states, do not complete any form other than these forms. 2. You can download the required forms from the IRS website, www.irs.gov or use any tax software package. If you need to refer to the instructions to the forms, they are available at the IRS website. Neatness of the completed forms will be considered in the grading of the project . 3. Use the attached schedule, Table A-1 to determine Ron’s taxable compensation from Regal Design Corporation. Fill in the column titled “Taxable Amount” with the amount that you think is included (or reduces) Ron’s gross income. The “taxable compensation” amount at the bottom of the table must agree with the amount you report on line 7, Form 1040. Attach your completed Table A-1 to your return to receive any partial credit for the amount shown on line 7, Form 1040. 4. Attach a separate sheet of paper listing the type and amount of any items reported in “other income” on line 21, Form 1040. 5. You may complete the project with one other student from either section. If you do, turn in one completed return with the

- 10. names of both students listed who completed the project. 6. The project is worth 53 points. 7. Due Date : Monday, April 14th, by 8:00 p.m. Additional Return Preparation Notes 1. The gross salary of $87,800 is before any subtractions or additions due to withholding or fringe benefits. 2. All charitable contributions to FirstUnitedChurch were made in cash in amounts of less than $250 each. Table A-1 Schedule of Regal Design Corporation Taxable Compensation Item Regal Design Corporation Amount Taxable Amount

- 11. Annual salary $ 87,800 Federal income tax withholding $ 9,950 Michigan income tax withholding $ 3,600 Social Security tax withholding $ 6,717

- 12. Pension plan contribution paid by Ron $ 4,000 Pension plan contribution paid by Regal Design Corporation $ 4,000 Medical insurance premiums $ 3,500 Reimbursement of medical costs $ 3,200

- 13. Ron's payment into flexible benefits plan $ 1,500 Reimbursement from flexible benefits plan $ 1,500 Group term life insurance premiums $ 375 Disability insurance premiums $ 650 Payment of Fidelity retirement planning services

- 14. $ 200 Discount received on home building design $ 700 Tuition reimbursed by educational assistance program $ 6,300 Health club dues $ 325 Free parking

- 15. $ 3,000 Professional dues and subscriptions $ 850 Disability income from Regal Design' s plan and Ron's plan $ 4,250 Taxable Compensation