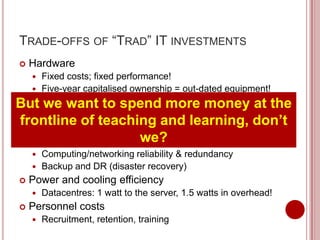

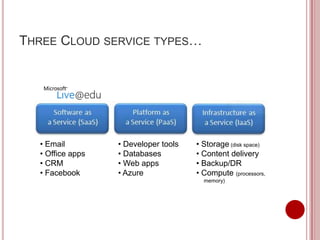

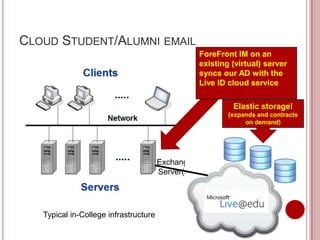

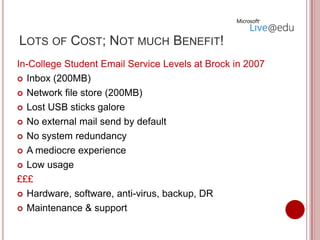

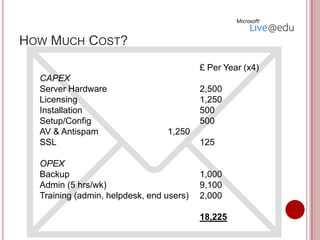

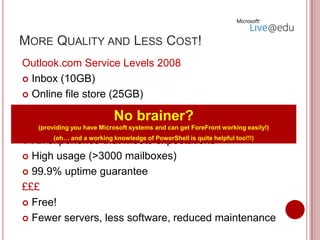

This document discusses how moving computing infrastructure and services to the cloud can save costs and improve quality for further education colleges. It begins by defining cloud computing and outlines the traditional costs of owning on-premise IT hardware and software versus renting configurable computing resources from the cloud. The document uses the example of moving from an on-premise student email server to Microsoft Outlook.com to illustrate how cloud computing reduced costs by thousands of pounds per year while improving features and reliability. It acknowledges risks around data security, legal compliance, and vendor reliability but argues that the opportunities for expenditure management, innovation, and focusing on core educational activities outweigh these concerns. The conclusion is that for most colleges, computing is now effectively a utility and spending