This document is a form for computing tax credits under the Nebraska Employment and Investment Growth Act. It requires information about a company's investment amounts, employment levels, wages, and other details related to a project over multiple years. The form is used to track qualification for credits and to calculate the credits that can be claimed or carried forward for the tax year.

ACC 422 Final Exam Guide New 2017 seek Your Dream/snaptutorialdotcomapjk535

For more classes visit

www.snaptutorial.com

Brief Exercise 7-7

Larkspur Family Importers sold goods to Tung Decorators for $40,800 on November 1, 2017, accepting Tung’s $40,800, 6-month, 6% note.

Prepare Larkspur’s November 1 entry, December 31 annual adjusting entry, and May 1 entry for the collection of the note and interest.

ACC 422 Final Exam Guide Score 29-30 seek Your Dream/snaptutorialdotcomapjk536

For more classes visit

www.snaptutorial.com

Question 14

A fire destroys all of the merchandise of Shamrock Company on February 10, 2017. Presented below is information compiled up to the date of the fire.

Inventory, January 1, 2017

$432,200

Sales revenue to February 10, 2017

ACC 422 Final Exam Guide New 2017 seek Your Dream/acc422martdotcomapjk538

For more classes visit

www.snaptutorial.com

Brief Exercise 7-7

Larkspur Family Importers sold goods to Tung Decorators for $40,800 on November 1, 2017, accepting Tung’s $40,800, 6-month, 6% note.

Prepare Larkspur’s November 1 entry, December 31 annual adjusting entry, and May 1 entry for the collection of the note and interest.

ACC 422 Final Exam Guide New 2017 seek Your Dream/uophelpdotcomapjk533

For more classes visit

www.uophelp.com

Brief Exercise 7-7

Larkspur Family Importers sold goods to Tung Decorators for $40,800 on November 1, 2017, accepting Tung’s $40,800, 6-month, 6% note.

Prepare Larkspur’s November 1 entry, December 31 annual adjusting entry, and May 1 entry for the collection of the note and interest.

ACC 422 Final Exam Guide Score 29-30 seek Your Dream/acc422martdotcomapjk538

For more classes visit

www.snaptutorial.com

Question 14

A fire destroys all of the merchandise of Shamrock Company on February 10, 2017. Presented below is information compiled up to the date of the fire.

Inventory, January 1, 2017

$432,200

Sales revenue to February 10, 2017

ACC 422 Final Exam Guide Score 29-30 seek Your Dream/uophelpdotcomapjk533

For more classes visit

www.uophelp.com

Question 14

A fire destroys all of the merchandise of Shamrock Company on February 10, 2017. Presented below is information compiled up to the date of the fire.

Inventory, January 1, 2017

$432,200

Sales revenue to February 10, 2017

1,935,200

ACC 422 Final Exam Guide New 2017 seek Your Dream/snaptutorialdotcomapjk535

For more classes visit

www.snaptutorial.com

Brief Exercise 7-7

Larkspur Family Importers sold goods to Tung Decorators for $40,800 on November 1, 2017, accepting Tung’s $40,800, 6-month, 6% note.

Prepare Larkspur’s November 1 entry, December 31 annual adjusting entry, and May 1 entry for the collection of the note and interest.

ACC 422 Final Exam Guide Score 29-30 seek Your Dream/snaptutorialdotcomapjk536

For more classes visit

www.snaptutorial.com

Question 14

A fire destroys all of the merchandise of Shamrock Company on February 10, 2017. Presented below is information compiled up to the date of the fire.

Inventory, January 1, 2017

$432,200

Sales revenue to February 10, 2017

ACC 422 Final Exam Guide New 2017 seek Your Dream/acc422martdotcomapjk538

For more classes visit

www.snaptutorial.com

Brief Exercise 7-7

Larkspur Family Importers sold goods to Tung Decorators for $40,800 on November 1, 2017, accepting Tung’s $40,800, 6-month, 6% note.

Prepare Larkspur’s November 1 entry, December 31 annual adjusting entry, and May 1 entry for the collection of the note and interest.

ACC 422 Final Exam Guide New 2017 seek Your Dream/uophelpdotcomapjk533

For more classes visit

www.uophelp.com

Brief Exercise 7-7

Larkspur Family Importers sold goods to Tung Decorators for $40,800 on November 1, 2017, accepting Tung’s $40,800, 6-month, 6% note.

Prepare Larkspur’s November 1 entry, December 31 annual adjusting entry, and May 1 entry for the collection of the note and interest.

ACC 422 Final Exam Guide Score 29-30 seek Your Dream/acc422martdotcomapjk538

For more classes visit

www.snaptutorial.com

Question 14

A fire destroys all of the merchandise of Shamrock Company on February 10, 2017. Presented below is information compiled up to the date of the fire.

Inventory, January 1, 2017

$432,200

Sales revenue to February 10, 2017

ACC 422 Final Exam Guide Score 29-30 seek Your Dream/uophelpdotcomapjk533

For more classes visit

www.uophelp.com

Question 14

A fire destroys all of the merchandise of Shamrock Company on February 10, 2017. Presented below is information compiled up to the date of the fire.

Inventory, January 1, 2017

$432,200

Sales revenue to February 10, 2017

1,935,200

Discover the innovative and creative projects that highlight my journey throu...dylandmeas

Discover the innovative and creative projects that highlight my journey through Full Sail University. Below, you’ll find a collection of my work showcasing my skills and expertise in digital marketing, event planning, and media production.

Unveiling the Secrets How Does Generative AI Work.pdfSam H

At its core, generative artificial intelligence relies on the concept of generative models, which serve as engines that churn out entirely new data resembling their training data. It is like a sculptor who has studied so many forms found in nature and then uses this knowledge to create sculptures from his imagination that have never been seen before anywhere else. If taken to cyberspace, gans work almost the same way.

What is the TDS Return Filing Due Date for FY 2024-25.pdfseoforlegalpillers

It is crucial for the taxpayers to understand about the TDS Return Filing Due Date, so that they can fulfill your TDS obligations efficiently. Taxpayers can avoid penalties by sticking to the deadlines and by accurate filing of TDS. Timely filing of TDS will make sure about the availability of tax credits. You can also seek the professional guidance of experts like Legal Pillers for timely filing of the TDS Return.

Affordable Stationery Printing Services in Jaipur | Navpack n PrintNavpack & Print

Looking for professional printing services in Jaipur? Navpack n Print offers high-quality and affordable stationery printing for all your business needs. Stand out with custom stationery designs and fast turnaround times. Contact us today for a quote!

Buy Verified PayPal Account | Buy Google 5 Star Reviewsusawebmarket

Buy Verified PayPal Account

Looking to buy verified PayPal accounts? Discover 7 expert tips for safely purchasing a verified PayPal account in 2024. Ensure security and reliability for your transactions.

PayPal Services Features-

🟢 Email Access

🟢 Bank Added

🟢 Card Verified

🟢 Full SSN Provided

🟢 Phone Number Access

🟢 Driving License Copy

🟢 Fasted Delivery

Client Satisfaction is Our First priority. Our services is very appropriate to buy. We assume that the first-rate way to purchase our offerings is to order on the website. If you have any worry in our cooperation usually You can order us on Skype or Telegram.

24/7 Hours Reply/Please Contact

usawebmarketEmail: support@usawebmarket.com

Skype: usawebmarket

Telegram: @usawebmarket

WhatsApp: +1(218) 203-5951

USA WEB MARKET is the Best Verified PayPal, Payoneer, Cash App, Skrill, Neteller, Stripe Account and SEO, SMM Service provider.100%Satisfection granted.100% replacement Granted.

Attending a job Interview for B1 and B2 Englsih learnersErika906060

It is a sample of an interview for a business english class for pre-intermediate and intermediate english students with emphasis on the speking ability.

Memorandum Of Association Constitution of Company.pptseri bangash

www.seribangash.com

A Memorandum of Association (MOA) is a legal document that outlines the fundamental principles and objectives upon which a company operates. It serves as the company's charter or constitution and defines the scope of its activities. Here's a detailed note on the MOA:

Contents of Memorandum of Association:

Name Clause: This clause states the name of the company, which should end with words like "Limited" or "Ltd." for a public limited company and "Private Limited" or "Pvt. Ltd." for a private limited company.

https://seribangash.com/article-of-association-is-legal-doc-of-company/

Registered Office Clause: It specifies the location where the company's registered office is situated. This office is where all official communications and notices are sent.

Objective Clause: This clause delineates the main objectives for which the company is formed. It's important to define these objectives clearly, as the company cannot undertake activities beyond those mentioned in this clause.

www.seribangash.com

Liability Clause: It outlines the extent of liability of the company's members. In the case of companies limited by shares, the liability of members is limited to the amount unpaid on their shares. For companies limited by guarantee, members' liability is limited to the amount they undertake to contribute if the company is wound up.

https://seribangash.com/promotors-is-person-conceived-formation-company/

Capital Clause: This clause specifies the authorized capital of the company, i.e., the maximum amount of share capital the company is authorized to issue. It also mentions the division of this capital into shares and their respective nominal value.

Association Clause: It simply states that the subscribers wish to form a company and agree to become members of it, in accordance with the terms of the MOA.

Importance of Memorandum of Association:

Legal Requirement: The MOA is a legal requirement for the formation of a company. It must be filed with the Registrar of Companies during the incorporation process.

Constitutional Document: It serves as the company's constitutional document, defining its scope, powers, and limitations.

Protection of Members: It protects the interests of the company's members by clearly defining the objectives and limiting their liability.

External Communication: It provides clarity to external parties, such as investors, creditors, and regulatory authorities, regarding the company's objectives and powers.

https://seribangash.com/difference-public-and-private-company-law/

Binding Authority: The company and its members are bound by the provisions of the MOA. Any action taken beyond its scope may be considered ultra vires (beyond the powers) of the company and therefore void.

Amendment of MOA:

While the MOA lays down the company's fundamental principles, it is not entirely immutable. It can be amended, but only under specific circumstances and in compliance with legal procedures. Amendments typically require shareholder

Personal Brand Statement:

As an Army veteran dedicated to lifelong learning, I bring a disciplined, strategic mindset to my pursuits. I am constantly expanding my knowledge to innovate and lead effectively. My journey is driven by a commitment to excellence, and to make a meaningful impact in the world.

Improving profitability for small businessBen Wann

In this comprehensive presentation, we will explore strategies and practical tips for enhancing profitability in small businesses. Tailored to meet the unique challenges faced by small enterprises, this session covers various aspects that directly impact the bottom line. Attendees will learn how to optimize operational efficiency, manage expenses, and increase revenue through innovative marketing and customer engagement techniques.

As a business owner in Delaware, staying on top of your tax obligations is paramount, especially with the annual deadline for Delaware Franchise Tax looming on March 1. One such obligation is the annual Delaware Franchise Tax, which serves as a crucial requirement for maintaining your company’s legal standing within the state. While the prospect of handling tax matters may seem daunting, rest assured that the process can be straightforward with the right guidance. In this comprehensive guide, we’ll walk you through the steps of filing your Delaware Franchise Tax and provide insights to help you navigate the process effectively.

[Note: This is a partial preview. To download this presentation, visit:

https://www.oeconsulting.com.sg/training-presentations]

Sustainability has become an increasingly critical topic as the world recognizes the need to protect our planet and its resources for future generations. Sustainability means meeting our current needs without compromising the ability of future generations to meet theirs. It involves long-term planning and consideration of the consequences of our actions. The goal is to create strategies that ensure the long-term viability of People, Planet, and Profit.

Leading companies such as Nike, Toyota, and Siemens are prioritizing sustainable innovation in their business models, setting an example for others to follow. In this Sustainability training presentation, you will learn key concepts, principles, and practices of sustainability applicable across industries. This training aims to create awareness and educate employees, senior executives, consultants, and other key stakeholders, including investors, policymakers, and supply chain partners, on the importance and implementation of sustainability.

LEARNING OBJECTIVES

1. Develop a comprehensive understanding of the fundamental principles and concepts that form the foundation of sustainability within corporate environments.

2. Explore the sustainability implementation model, focusing on effective measures and reporting strategies to track and communicate sustainability efforts.

3. Identify and define best practices and critical success factors essential for achieving sustainability goals within organizations.

CONTENTS

1. Introduction and Key Concepts of Sustainability

2. Principles and Practices of Sustainability

3. Measures and Reporting in Sustainability

4. Sustainability Implementation & Best Practices

To download the complete presentation, visit: https://www.oeconsulting.com.sg/training-presentations

Explore our most comprehensive guide on lookback analysis at SafePaaS, covering access governance and how it can transform modern ERP audits. Browse now!

Enterprise Excellence is Inclusive Excellence.pdfKaiNexus

Enterprise excellence and inclusive excellence are closely linked, and real-world challenges have shown that both are essential to the success of any organization. To achieve enterprise excellence, organizations must focus on improving their operations and processes while creating an inclusive environment that engages everyone. In this interactive session, the facilitator will highlight commonly established business practices and how they limit our ability to engage everyone every day. More importantly, though, participants will likely gain increased awareness of what we can do differently to maximize enterprise excellence through deliberate inclusion.

What is Enterprise Excellence?

Enterprise Excellence is a holistic approach that's aimed at achieving world-class performance across all aspects of the organization.

What might I learn?

A way to engage all in creating Inclusive Excellence. Lessons from the US military and their parallels to the story of Harry Potter. How belt systems and CI teams can destroy inclusive practices. How leadership language invites people to the party. There are three things leaders can do to engage everyone every day: maximizing psychological safety to create environments where folks learn, contribute, and challenge the status quo.

Who might benefit? Anyone and everyone leading folks from the shop floor to top floor.

Dr. William Harvey is a seasoned Operations Leader with extensive experience in chemical processing, manufacturing, and operations management. At Michelman, he currently oversees multiple sites, leading teams in strategic planning and coaching/practicing continuous improvement. William is set to start his eighth year of teaching at the University of Cincinnati where he teaches marketing, finance, and management. William holds various certifications in change management, quality, leadership, operational excellence, team building, and DiSC, among others.

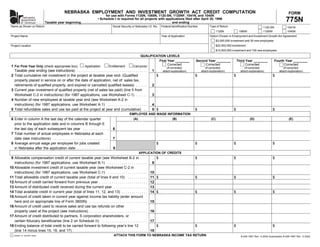

1. RESET FORM

NEBRASKA EMPLOYMENT AND INVESTMENT GROWTH ACT CREDIT COMPUTATION FORM

for use with Forms 1120N, 1065N, 1120-SN, 1120NF, 1041N, and 1040N

nebraska

775N

• Schedule I is required for all projects with applications filed after April 30, 1996

department

Taxable year beginning , and ending ,

of revenue

Name as Shown on Return Social Security or Nebraska I.D. No. Federal Identification Number Type of Return 1120-SN 1041N

1120N 1065N 1120NF 1040N

Project Name Year of Application Option Chosen in Employment and Investment Growth Act Agreement

$3,000,000 investment and 30 new employees

$20,000,000 investment

Project Location

$10,000,000 investment and 100 new employees

QUALIFICATION LEVELS

First Year ________ Second Year ________ Third Year ________ Fourth Year ________

Corrected Corrected Corrected Corrected

1 For First Year Only (check appropriate box) Application Entitlement Carryover (If corrected, (If corrected, (If corrected, (If corrected,

Taxable year ending (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 attach explanation) attach explanation) attach explanation) attach explanation)

2 Total cumulative net investment in the project at taxable year end. (Qualified $ $ $ $

property placed in service on or after the date of application, net of: sales tax,

retirements of qualified property, and expired or cancelled qualified leases) . . . . . . 2

3 Current year investment of qualified property (net of sales tax paid) (line 5 from

Worksheet C-2 in instructions) (for 1987 applications, use Worksheet C-1) . . . . . . 3

4 Number of new employees at taxable year end (see Worksheet A-2 in

instructions) (for 1987 applications, use Worksheet A-1) . . . . . . . . . . . . . . . . . . . . 4

5 Total refundable sales and use tax paid at the project at year end (cumulative) . . 5$ $ $ $

EMPLOYEE AND WAGE INFORMATION

6 Enter in column A the last day of the calendar quarter (A) (B) (C) (D) (E)

prior to the application date and in columns B through E

the last day of each subsequent tax year . . . . . . . . . . . . . 6

7 Total number of actual employees in Nebraska at each

date (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

8 Average annual wage per employee for jobs created $ $ $ $

in Nebraska after the application date . . . . . . . . . . . . . . . . 8

APPLICATION OF CREDITS

9 Allowable compensation credit of current taxable year (see Worksheet B-2 in $ $ $ $

instructions) (for 1987 applications, use Worksheet B-1) . . . . . . . . . . . . . . . . . . . . 9

10 Allowable investment credit of current taxable year (see Worksheet C-2 in

instructions) (for 1987 applications, use Worksheet C-1) . . . . . . . . . . . . . . . . . . . . 10

11 Total allowable credit of current taxable year (total of lines 9 and 10) . . . . . . . . . . 11 $ $ $ $

12 Amount of credit carried forward from previous year . . . . . . . . . . . . . . . . . . . . . . . . 12

13 Amount of distributed credit received during the current year . . . . . . . . . . . . . . . . . 13

14 Total available credit in current year (total of lines 11, 12, and 13) . . . . . . . . . . . . . 14 $ $ $ $

15 Amount of credit taken in current year against income tax liability (enter amount

here and on appropriate line of Form 3800N) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

16 Amount of credit used to receive sales and use tax refunds on other

property used at the project (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

17 Amount of credit distributed to partners, S corporation shareholders, or

certain fiduciary beneficiaries (line 2 on Schedule II) . . . . . . . . . . . . . . . . . . . . . . . 17

18 Ending balance of total credit to be carried forward to following year’s line 12 $ $ $ $

(line 14 minus lines 15, 16, and 17) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

ATTACH THIS FORM TO NEBRASKA INCOME TAX RETURN

printed on recycled paper

8-426-1987 Rev. 4-2004 Supersedes 8-426-1987 Rev. 5-2002

2. NEBRASKA EMPLOYMENT AND INVESTMENT GROWTH ACT CREDIT COMPUTATION, Page 2

Social Security or Nebraska I.D. No.

Project Name

Company Name

QUALIFICATION LEVELS

Fifth Year ________ Sixth Year ________ Seventh Year ________ Eighth Year ________ Ninth Year ________

Corrected Corrected Corrected Corrected Corrected

(If corrected, (If corrected, (If corrected, (If corrected, (If corrected,

1 Taxable year ending (see instructions) . . . . . . . . . . . . . . . 1 attach explanation) attach explanation) attach explanation) attach explanation) attach explanation)

2 Total cumulative net investment in the project at taxable $ $ $ $ $

year end. (Qualified property placed in service on or after

the date of application, net of: sales tax, retirements of

qualified property, and expired or cancelled qualified leases) 2

3 Current year investment of qualified property (net of sales

tax paid) (line 5 from Worksheet C-2 in instructions) (for

1987 applications, use Worksheet C-1) . . . . . . . . . . . . . . . 3

4 Number of new employees at taxable year end (see

Worksheet A-2 in instructions) (for 1987 applications,

use Worksheet A-1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

5 Total refundable sales and use tax paid at the project $ $ $ $ $

at year end . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

EMPLOYEE AND WAGE INFORMATION

6 Enter in columns F through J the last day of each (F) (G) (H) (I) (J)

tax year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

7 Total number of actual employees in Nebraska at each

date (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

8 Average annual wage per employee for jobs created $ $ $ $ $

in Nebraska after the application date . . . . . . . . . . . . . . . . 8

APPLICATION OF CREDITS

9 Allowable compensation credit of current taxable year $ $ $ $ $

(see Worksheet B-2 in instructions) (for 1987 applications,

use Worksheet B-1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

10 Allowable investment credit of current taxable year (see

Worksheet C-2 in instructions) (for 1987 applications, use

Worksheet C-1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

11 Total allowable credit of current taxable year (total of $ $ $ $ $

lines 9 and 10) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

12 Amount of credit carried forward from previous year . . . . . 12

13 Amount of distributed credit received during the

current year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

14 Total available credit in current year (total of lines 11, $ $ $ $ $

12, and 13) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

15 Amount of credit taken in current year against income

tax liability (enter amount here and on appropriate line

of Form 3800N) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

16 Amount of credit used to receive sales and use tax

refunds on other property used at the project

(see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

17 Amount of credit distributed to partners, S corporation

shareholders, or certain fiduciary beneficiaries

(line 2 on Schedule II) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

18 Ending balance of total credit to be carried forward to $ $ $ $ $

following year’s line 12 (line 14 minus lines 15, 16, and 17) 18

ATTACH THIS FORM TO NEBRASKA INCOME TAX RETURN

3. NEBRASKA SCHEDULE I — Estimated Sales or Use Tax Refunds FORM

• Required for any project with application filed after April 30, 1996

nebraska

775N

department

• Attach to Form 775N

of revenue

Name as Shown on Form 775N Project Name Nebraska Identification Number

B – Adjusted C

A D

3 If Different Than Direct Refund

Tax Year in Which Refund is Made Credit Refunds

Last Filed Amount

1 Application Year

$

$

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22 Total Estimated Refunds $

$

(lines 1 through 21)

INSTRUCTIONS

Year. The taxable year of the taxpayer.

WHO MUST FILE. Any applicant who applied after

April 30, 1996, under the Employment and Investment Growth

COLUMN C - DIRECT REFUNDS. Direct refunds are

Act must file the Nebraska Schedule I - Estimated Sales and

refunds of Nebraska sales and use taxes on purchases of qualified

Use Tax Refunds each year.

property for use at the project, or on aircraft for use in connection

DEFINITIONS.

with the project. All purchases of qualified property or aircraft

Entitlement period. The year during which the required after the date of application through the end of the entitlement

increases in employment and investment were met or exceeded, period are eligible for refund. The direct refunds cannot be

and the next six years. claimed or paid until the year after the required levels of

Carryover period. The next eight years after the end of the employment and investment are met. In subsequent years,

entitlement period. quarterly refund claims may be filed.

Qualified property. Any type of property of a type subject to

COLUMN D - CREDIT REFUNDS. Credit refunds are

depreciation, amortization, or other recovery under the Internal

refunds of Nebraska sales and use taxes using credits earned at

Revenue Code of 1986, or components of such property, that

the project. Credit refunds are for purchases for use at the project

will be located and used at the project. Qualified property does

that are not eligible for direct refunds. Credit refunds are for

not include (a) aircraft, barges, motor vehicles, railroad rolling

purchases made after the year the required levels were met,

stock, watercraft, or computer software (Revenue Ruling 29-

through the end of the carryover period. Credit refunds for

87-11), or (b) property that is rented by the taxpayer qualifying

purchases during a year cannot exceed the credit balance at the

under the Employment and Investment Growth Act to another

beginning of the year.

person.

ATTACH THIS PAGE TO YOUR NEBRASKA INCOME TAX RETURN

3

4. NEBRASKA SCHEDULE II — Distribution of Employment and Investment FORM

Growth Act Credit

nebraska

775N

department

of revenue For Partnerships, S Corporations, and Certain Fiduciaries Only

Name as Shown on Form 775N Project Name Nebraska Identification Number

1 Enter in the space provided each partner’s, shareholder’s, or beneficiary’s name, social security number or Nebraska identification

number, share of income or ownership, and distributed share of the credit reported on line 17, Form 775N (or attach a schedule

providing the above information). In the last column indicate whether each partner, shareholder, or beneficiary is subject to income

or franchise tax and sales tax.

Subject to Income

Social Security or

Name of Partner, Share of

Amount of Credit and Sales Tax

Nebraska I.D. No.

Shareholder, or Beneficiary* Income or Ownership

Yes No

2 TOTAL (enter here, and include on line 17, Form 775N) ....................................

* NOTE: Each partner, S corporation shareholder, and beneficiary should be notified of the distributed share of the credit reported on line

17, Form 775N. Such notice will allow partners, S corporation shareholders, or beneficiaries to complete their Form 3800N, Part C.

ATTACH THIS PAGE TO YOUR NEBRASKA INCOME TAX RETURN

4

5. NEBRASKA SCHEDULE III —Changes Within Current Employment and FORM

nebraska

Investment Growth Act Project

department

775N

of revenue

Name as Shown on Form 775N Project Name Nebraska Identification Number Date of Application

SECTION 1:

Addition of New Location to Project

1 A Is there a new location included in the project? .................................................................................... YES NO

B What is the new address?

2 Does the application include all locations in the state? .............................................................................. YES NO

3 Is the location interdependent with the prior project locations? ................................................................. YES NO

How?

SECTION 2:

Change in Ownership of Project

4 Has the controlling ownership of applicant changed? ................................................................................ YES NO

If Yes, please explain.

5 Is the applicant named in the Employment and Investment Growth Act agreement a corporation? .......... YES NO

If No, it is not necessary to complete the rest of this section.

6 Does Paragraph 1 of the Employment and Investment Growth Agreement include unitary group

members? ........................................................................................................................................... YES NO

SECTION 3:

Addition of New Entity or Acquisition of Assets

7 Was there a purchase of the assets of another business? ........................................................................ YES NO

If Yes, please identify.

Please complete questions 9B, 10 and 11 of this section.

8 Is there a new corporation, joint venture, limited liability company, or partnership that is doing business

at the project? ........................................................................................................................................... YES NO

If Yes, please identify.

Please complete questions 9 through 11 of this section and questions 5 and 6 of Section 2.

9 A Is the entity owned at least fifty percent by corporate members of the unitary group? ......................... YES NO

If Yes, please identify owners and percent of ownership.

B Is the new business engaged in a qualifying activity? .......................................................................... YES NO

Describe the activity:

C Is the entity unitary with the corporate members of the unitary group? ................................................ YES NO

10 Was the base year adjusted for the full-time equivalent employees which worked for the new entity for

the 12-month period of time prior to the date of acquisition? ..................................................................... YES NO

11 Was the investment placed in service prior to the date of acquisition excluded from the investment

calculations? ........................................................................................................................................... YES NO

NOTE: If the response to line 7 or 8 includes more than one entity, please attach a schedule which provides a response to the

required questions for each of the entities.

ATTACH THIS PAGE TO YOUR NEBRASKA INCOME TAX RETURN

5

6. INSTRUCTIONS

WHO MUST FILE. Any taxpayer who has filed a project application For 1987 applications, the average number of employees is

for an agreement with the State Tax Commissioner must file a determined by converting into equivalent employees of 40

Nebraska Employment and Investment Growth Act Credit hours per week the number of hours paid for the time periods

Computation, Form 775N, for each year from the filing of the including the first day of the year and the last day of each

application through the expiration of all incentives under the Act. quarter of the year.

WHEN AND WHERE TO FILE. This computation must be filed For applications filed after January 1, 1988, the annual average

as an attachment to the taxpayer’s Nebraska income tax return. number of new employees is determined by converting into

However, the taxpayer may elect to file the form reporting the initial equivalent employees the total number of hours paid per year,

attainment of the required levels immediately after the last day of divided by (40 multiplied by the number of weeks in the year).

the year the required levels were met. 9. Qualifying business. Any business engaged in the

ROUND TO WHOLE DOLLARS. Any amount from fifty cents following activities:

through 99 cents is to be rounded to the next higher dollar; and any a. The conducting of research, development, or testing for

amount less than 50 cents is to be rounded to the next lower dollar. scientific, agricultural, animal husbandry, food product,

The amounts on the computation form must be shown in whole or industrial purposes;

dollars.

b. The performance of data processing, telecom-

munication, insurance, or financial services;

DEFINITIONS.

1. Base year. The year immediately preceding the year during c. The assembly, fabrication, manufacture, or

which the application was submitted by the taxpayer. processing of tangible personal property;

2. Base-year employee. Any individual who was employed d. The storage, warehousing, distribution, or trans-portation

in Nebraska and subject to the Nebraska income tax on of tangible personal property;

compensation received from the taxpayer or its predecessors e. The sale of tangible personal property if more than 20

during the base year and who was employed at the project at percent of the total sales are in any combination of the

some time since the end of the year preceding the base year. following:

For companies acquired by the taxpayer after the year of (1) Sales for resale (wholesale sales),

application, the base year for the acquired company shall be (2) Sales of tangible personal property assembled,

the twelve months preceding the year of acquisition. Make fabricated, manufactured, or processed by the seller,

adjustment on line 4 of Worksheet A-1 or A-2, depending on or

the year of application.

(3) Sales of tangible personal property used by the

3. Compensation. The wages and other payments subject to purchaser in any of the listed qualifying activities;

withholding for federal income tax purposes. Normally, f. The administrative management of any activities,

moving expenses paid by the employer to the employee and including headquarter facilities, relating to such

401K contributions made by an employee are not activities; or

compensation.

g. Any combination of the activities listed above.

4. Entitlement period. The year during which the required

10. Qualified employee leasing company. A qualified

increases in employment and investment were first met or

employee leasing company is a company that places all

exceeded, and the next six years.

employees of a client-lessee on its payroll and leases such

5. Investment. The value of qualified property incorporated employees to the client-lessee on an ongoing basis for a fee

into or used at the project. For qualified property owned by and, that also grants to the client-lessee input into hiring

the taxpayer, the value is the original cost of the property. and firing decisions. A qualified employee leasing company

For qualified property rented by the taxpayer, the average net does not include a temporary employment agency.

annual rent is multiplied by the number of years of the lease 11. Qualified property. Any tangible property of a type subject

for which the taxpayer is initially bound, not to exceed ten to depreciation, amortization, or other recovery under the

years for 1987 applications. For applications after January 1, Internal Revenue Code of 1986, or components of such

1988, the average net annual rent is multiplied by the number property, that will be located and used at the project. Qualified

of years for which the taxpayer is initially bound, not to exceed property does not include: (a) aircraft, barges, motor vehicles,

ten years or the end of the third year after the entitlement railroad rolling stock, watercraft, or computer software

period, whichever is earlier. The rental of land included in (Revenue Ruling 29-87-11), or (b) property that is rented by

and incidental to the leasing of a building is included in the the taxpayer qualifying under the Employment and Investment

computation. Growth Act to another person.

6. Motor vehicle. Any motor vehicle, trailer, or semitrailer as 12. Taxpayer. Any person subject to sales and use tax, and either

defined in section 60-301 and subject to licensing for operation an income tax imposed by the Nebraska Revenue Act of 1967

on the highways. or a franchise tax under Chapter 77, article 38, any corporation

7. Nebraska employee. An individual who is either a resident that is a member of the same unitary group which is subject

or partial-year resident of Nebraska. to such taxes, and any partnership, S corporation, or joint

venture when the partners, shareholders, or members are

8. Number of new employees. The excess of the average

subject to such taxes.

number of employees employed at the project during a year

over the average number of base-year employees. 13. Year. The taxable year of the taxpayer.

6

7. SPECIFIC INSTRUCTIONS FOR APPLICATIONS FILED AFTER JANUARY 1, 1988

to correct previously reported years, check the corrected box for each

LINE 1. If you have more than nine years to report, you may start your

current report with the first year of your entitlement period or your year changed.

carryover period by checking the appropriate box. If you find it necessary LINE 4. Use the following worksheet to calculate your line 4 entry:

WORKSHEET A-2 — Full-time Equivalent Employees

Current Year at Project

1 Total number of employee hours paid per year (full-time, part-time, overtime, holiday, etc. hours paid during current year) . . 1

2 Number of full-time equivalent employees per year [divide line 1 amount by (40 times the number of weeks paid in year)] 2

Base Year at Project

3 Total number of employee hours paid per year (full-time, part-time, overtime, holiday, etc. hours paid during base year) . 3

4 Increase of base-year employees in hours (as a result of employees who worked in Nebraska in the base year being

transferred to and employed at the project or the acquisition by the taxpayer of a company eligible for inclusion

in the project — see definition of base-year employee on page 6) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

5 Total number of employee hours paid per year after adjustment, if any, during base year (line 3 plus line 4) . . . . . . . . 5

6 Number of full-time equivalent employees per year [divide line 5 amount by (40 times the number of weeks paid in year)] 6

7 Number of new employees at taxable year end (line 2 minus line 6). Enter amount here and on line 4, Form 775N . . . 7

LINE 5. Enter the total of sales and use taxes paid on the project at year LINE 10. Use the following worksheet to calculate your line 10 entry:

end. This is the cumulative balance of the sales and use taxes paid at the

WORKSHEET C-2 — Investment Credit

project.

1 Total cost of qualified property incorporated into

LINE 7. Enter the total number of employees employed in Nebraska at or used at the project (see definition of “qualified

each date. Use the number of actual people employed, not full-time property”) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

equivalent employees. Include all employees in Nebraska, not just those 2 Total average net annual lease/rent expense for

employed at the project. qualified property leased/rented by the taxpayer for

use at the project (multiply average net annual rent

LINE 8. Enter the estimated annual wage per new employee for jobs

by the number of years of the lease for which

created in Nebraska after the application date. taxpayer was originally bound, not to exceed ten

years, or 3 years past end of entitlement period,

NOTE: A taxpayer must have signed an agreement and met the

whichever is earlier) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

required levels of employment and investment for the project in order

3 Total value of qualified property incorporated

to claim a compensation credit on line 9 and an investment credit on

into or used at the project (total of lines 1 and 2) . . . . . . . $

line 10. The taxpayer must meet both threshold levels of investing

4 A Less the amount of refundable Nebraska state

in qualified property of at least $3 million and the hiring of at least

and local option sales or use taxes included

30 new employees by the close of the current taxable year in order in the line 3 amount . . . . . . . . . . . . . . . . . . . . . . . . . . . $

to claim either compensation credit or investment credit for the

B Less the unpaid portion of canceled leases previously

current taxable year’s Form 775N. claimed as investment . . . . . . . . . . . . . . . . . . . . . . . . . $

LINE 9. Use the following worksheet to calculate your line 9 entry: 5 Investment amount of qualified property (line 3 minus

the total of lines 4A and 4B) (Enter amount here and on

WORKSHEET B-2 — Compensation Credits line 3 of Form 775N) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

6 Investment credit of current year (multiply line 5 by .10,

1 Total taxable compensation paid to all employees employed and enter this amount on line 10 of Form 775N) . . . . . . . . $

at the project for the current year . . . . . . . . . . . . . . . . . . . $

LINE 13. Enter the amount of distributed credit received during the

2 Total full-time equivalent employees for the current

year (line 2 of Worksheet A-2) . . . . . . . . . . . . . . . . . . . . . $

year. For example, a C corporation subsidiary could receive credits from

3 Average compensation for current year

its unitary S corporation parent.

(line 1 divided by line 2) . . . . . . . . . . . . . . . . . . . . . . . . . . $

LINE 16. Enter the amount of credit used to obtain refunds of sales and

4 Total full-time equivalent employees for base year

(line 6 of Worksheet A-2) . . . . . . . . . . . . . . . . . . . . . . . . . $

use taxes paid by the taxpayer on non-qualified property purchased and

used at the project after the end of the taxable year in which the taxpayer

5 Taxable compensation paid to non-resident employees,

who are not base year employees, for the current year . . $

met both thresholds of investing $3 million and hiring 30 new employees.

6 Total eligible current year compensation paid

(line 1 minus line 5) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

LINE 17. From line 2, Schedule II, enter the amount of credit distributed

7 Average compensation paid to base-year employees

to partners, S corporation shareholders, or certain fiduciary beneficiaries.

(line 3 multiplied by line 4) . . . . . . . . . . . . . . . . . . . . . . . . $

Any credit distributed by a partnership, S corporation, or estate or trust

8 Excess compensation paid during the year (line 6

minus line 7) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

must be distributed to the partners, shareholders, or beneficiaries in the

9 Compensation credit for the current year (multiply

same manner as income is distributed for use against their income tax

line 8 amount by .05, and enter on line 9, Form 775N) . . . $

liabilities.

ATTACH THIS PAGE TO YOUR NEBRASKA INCOME TAX RETURN

7

8. SPECIFIC INSTRUCTIONS FOR 1987 APPLICATIONS

to correct previously reported years, check the corrected box for each

LINE 1. If you have more than nine years to report, you may start your

current report with the first year of your entitlement period or your year changed.

carryover period by checking the appropriate box. If you find it necessary LINE 4. Use the following worksheet to calculate your line 4 entry:

WORKSHEET A-1 — Full-Time Equivalent Employees

TAXABLE YEAR (F)

Average of

LAST DAY OF QUARTER

(A)

Employment Calculation Columns A, B,

First (B) (C) (D) (E) C, D, and E

Day First Second Third Fourth

Current Year at Project

1 Total number of employee hours paid per week (full-time, part-time, overtime,

holiday, etc. hours paid during the week which included the day listed above)

2 Number of full-time equivalent employees per week (divide line 1

amount by 40) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Base Year at Project

3 Total number of employee hours paid per week (full-time, part-time, overtime,

holiday, etc. hours paid during the week which included the day listed above) .

4 Increase of base-year employees in hours (as a result of Nebraska

employees being transferred to and employed at the project or the

acquisition by the taxpayer of a company eligible for inclusion in the

project — see definition of base-year employee on page 6) . . . . . . . . . . . . . . . .

5 Total number of employee hours paid per week after adjustment,

if any (including the day listed above — line 3 plus line 4) . . . . . . . . . . . . . . . . .

6 Number of full-time equivalent employees per week (divide line 5

amount by 40) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7 Number of new employees at taxable year end (line 2, col. F, minus line 6, col. F). Enter amount here and on line 4, Form 775N .

LINE 5. Enter the total of sales and use taxes paid on the project at year LINE 10. Use the following worksheet to calculate your line 10 entry:

end. This is the cumulative balance of the sales and use taxes paid at the

project. WORKSHEET C-1 — Investment Credit

LINE 7. Enter the total number of employees employed in Nebraska at 1 Total cost of qualified property incorporated into or used

at the project (see definition of “qualified property”) . . . . . $

each date. Use the number of actual people employed, not full-time

2 Total average net annual lease/rent expense for

equivalent employees. Include all employees in Nebraska, not just those

qualified property leased/rented by the taxpayer for

employed at the project. use at the project (multiply average net annual rent by

LINE 8. Enter the estimated annual wage per new employee for jobs the number of years of the lease for which taxpayer

created in Nebraska after the application date. was originally bound, not to exceed ten years) . . . . . . . . . $

3 Total value of qualified property incorporated

NOTE: A taxpayer must have signed an agreement and met the into or used at the project (total of lines 1 and 2) . . . . . . . $

required levels of employment and investment for the project in order 4 A Less the amount of refundable Nebraska state

to claim a compensation credit on line 9 and an investment credit on and local option sales or use taxes included

line 10. The taxpayer must meet both threshold levels of investing in the line 3 amount . . . . . . . . . . . . . . . . . . . . . . . . . . . $

in qualified property of at least $3 million and the hiring of at least B Less the unpaid portion of canceled leases previously

30 new employees by the close of the current taxable year in order claimed as investment . . . . . . . . . . . . . . . . . . . . . . . . . $

to claim either compensation credit or investment credit for the 5 Investment amount of qualified property (line 3 minus

current taxable year’s Form 775N. the total of lines 4A and 4B) (Enter amount here and on

line 3 of Form 775N) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

LINE 9. Use the following worksheet to calculate your line 9 entry:

6 Investment credit of current year (multiply line 5 by .10,

and enter this amount on line 10 of Form 775N) . . . . . . . . $

WORKSHEET B-1 — Compensation Credits

LINE 13. Enter the amount of distributed credit received during the

1 Total taxable compensation paid to Nebraska resident employees,

year. For example, a C corporation subsidiary could receive credits from

other than base-year employees, while employed

its unitary S corporation parent.

at the project for the current year . . . . . . . . . . . . . . . . . . . $

2 Taxable compensation paid to base-year employees at the

LINE 16. Enter the amount of credit used to obtain refunds of sales and

project for the current year . . . . . . . . . . . . . . . . . . . . . . . . $

use taxes paid by the taxpayer on non-qualified property purchased and

3 Total taxable compensation paid (total of lines 1 and 2) . . $

used at the project after the end of the taxable year in which the taxpayer

4 Taxable compensation paid to base-year employees during

the base year (enter the amount of compensation

met both thresholds of investing $3 million and hiring 30 new employees.

paid to base-year employees during the base year

or the average of the total compensation paid during

LINE 17. From line 2, Schedule II, enter the amount of credit distributed

the base year and the two preceding years,

to partners, S corporation shareholders, or certain fiduciary beneficiaries.

whichever is greater) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

5 Excess compensation paid during the year

Any credit distributed by a partnership, S corporation, or estate or trust

(line 3 minus line 4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

must be distributed to the partners, shareholders, or beneficiaries in the

6 Compensation credit for the current year (multiply

same manner as income is distributed for use against their income tax

line 5 amount by .05, and enter on line 9 of

Form 775N) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

liabilities.

ATTACH THIS PAGE TO YOUR NEBRASKA INCOME TAX RETURN

8