Viridian Energy is a socially and environmentally responsible company bringing a Green Energy Choice to the Illinois market. Save Money & Go Green.

Similar to revenue.ne.gov tax current f_3800nwkst_r&d (20)

Falcon stands out as a top-tier P2P Invoice Discounting platform in India, bridging esteemed blue-chip companies and eager investors. Our goal is to transform the investment landscape in India by establishing a comprehensive destination for borrowers and investors with diverse profiles and needs, all while minimizing risk. What sets Falcon apart is the elimination of intermediaries such as commercial banks and depository institutions, allowing investors to enjoy higher yields.

Affordable Stationery Printing Services in Jaipur | Navpack n PrintNavpack & Print

Looking for professional printing services in Jaipur? Navpack n Print offers high-quality and affordable stationery printing for all your business needs. Stand out with custom stationery designs and fast turnaround times. Contact us today for a quote!

[Note: This is a partial preview. To download this presentation, visit:

https://www.oeconsulting.com.sg/training-presentations]

Sustainability has become an increasingly critical topic as the world recognizes the need to protect our planet and its resources for future generations. Sustainability means meeting our current needs without compromising the ability of future generations to meet theirs. It involves long-term planning and consideration of the consequences of our actions. The goal is to create strategies that ensure the long-term viability of People, Planet, and Profit.

Leading companies such as Nike, Toyota, and Siemens are prioritizing sustainable innovation in their business models, setting an example for others to follow. In this Sustainability training presentation, you will learn key concepts, principles, and practices of sustainability applicable across industries. This training aims to create awareness and educate employees, senior executives, consultants, and other key stakeholders, including investors, policymakers, and supply chain partners, on the importance and implementation of sustainability.

LEARNING OBJECTIVES

1. Develop a comprehensive understanding of the fundamental principles and concepts that form the foundation of sustainability within corporate environments.

2. Explore the sustainability implementation model, focusing on effective measures and reporting strategies to track and communicate sustainability efforts.

3. Identify and define best practices and critical success factors essential for achieving sustainability goals within organizations.

CONTENTS

1. Introduction and Key Concepts of Sustainability

2. Principles and Practices of Sustainability

3. Measures and Reporting in Sustainability

4. Sustainability Implementation & Best Practices

To download the complete presentation, visit: https://www.oeconsulting.com.sg/training-presentations

Digital Transformation and IT Strategy Toolkit and TemplatesAurelien Domont, MBA

This Digital Transformation and IT Strategy Toolkit was created by ex-McKinsey, Deloitte and BCG Management Consultants, after more than 5,000 hours of work. It is considered the world's best & most comprehensive Digital Transformation and IT Strategy Toolkit. It includes all the Frameworks, Best Practices & Templates required to successfully undertake the Digital Transformation of your organization and define a robust IT Strategy.

Editable Toolkit to help you reuse our content: 700 Powerpoint slides | 35 Excel sheets | 84 minutes of Video training

This PowerPoint presentation is only a small preview of our Toolkits. For more details, visit www.domontconsulting.com

Discover the innovative and creative projects that highlight my journey throu...dylandmeas

Discover the innovative and creative projects that highlight my journey through Full Sail University. Below, you’ll find a collection of my work showcasing my skills and expertise in digital marketing, event planning, and media production.

The key differences between the MDR and IVDR in the EUAllensmith572606

In the European Union (EU), two significant regulations have been introduced to enhance the safety and effectiveness of medical devices – the In Vitro Diagnostic Regulation (IVDR) and the Medical Device Regulation (MDR).

https://mavenprofserv.com/comparison-and-highlighting-of-the-key-differences-between-the-mdr-and-ivdr-in-the-eu/

LA HUG - Video Testimonials with Chynna Morgan - June 2024Lital Barkan

Have you ever heard that user-generated content or video testimonials can take your brand to the next level? We will explore how you can effectively use video testimonials to leverage and boost your sales, content strategy, and increase your CRM data.🤯

We will dig deeper into:

1. How to capture video testimonials that convert from your audience 🎥

2. How to leverage your testimonials to boost your sales 💲

3. How you can capture more CRM data to understand your audience better through video testimonials. 📊

Cracking the Workplace Discipline Code Main.pptxWorkforce Group

Cultivating and maintaining discipline within teams is a critical differentiator for successful organisations.

Forward-thinking leaders and business managers understand the impact that discipline has on organisational success. A disciplined workforce operates with clarity, focus, and a shared understanding of expectations, ultimately driving better results, optimising productivity, and facilitating seamless collaboration.

Although discipline is not a one-size-fits-all approach, it can help create a work environment that encourages personal growth and accountability rather than solely relying on punitive measures.

In this deck, you will learn the significance of workplace discipline for organisational success. You’ll also learn

• Four (4) workplace discipline methods you should consider

• The best and most practical approach to implementing workplace discipline.

• Three (3) key tips to maintain a disciplined workplace.

The world of search engine optimization (SEO) is buzzing with discussions after Google confirmed that around 2,500 leaked internal documents related to its Search feature are indeed authentic. The revelation has sparked significant concerns within the SEO community. The leaked documents were initially reported by SEO experts Rand Fishkin and Mike King, igniting widespread analysis and discourse. For More Info:- https://news.arihantwebtech.com/search-disrupted-googles-leaked-documents-rock-the-seo-world/

Enterprise Excellence is Inclusive Excellence.pdfKaiNexus

Enterprise excellence and inclusive excellence are closely linked, and real-world challenges have shown that both are essential to the success of any organization. To achieve enterprise excellence, organizations must focus on improving their operations and processes while creating an inclusive environment that engages everyone. In this interactive session, the facilitator will highlight commonly established business practices and how they limit our ability to engage everyone every day. More importantly, though, participants will likely gain increased awareness of what we can do differently to maximize enterprise excellence through deliberate inclusion.

What is Enterprise Excellence?

Enterprise Excellence is a holistic approach that's aimed at achieving world-class performance across all aspects of the organization.

What might I learn?

A way to engage all in creating Inclusive Excellence. Lessons from the US military and their parallels to the story of Harry Potter. How belt systems and CI teams can destroy inclusive practices. How leadership language invites people to the party. There are three things leaders can do to engage everyone every day: maximizing psychological safety to create environments where folks learn, contribute, and challenge the status quo.

Who might benefit? Anyone and everyone leading folks from the shop floor to top floor.

Dr. William Harvey is a seasoned Operations Leader with extensive experience in chemical processing, manufacturing, and operations management. At Michelman, he currently oversees multiple sites, leading teams in strategic planning and coaching/practicing continuous improvement. William is set to start his eighth year of teaching at the University of Cincinnati where he teaches marketing, finance, and management. William holds various certifications in change management, quality, leadership, operational excellence, team building, and DiSC, among others.

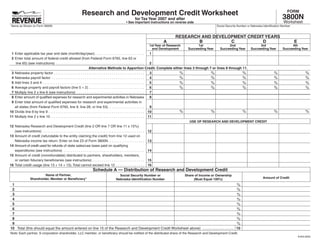

1. Research and Development Credit Worksheet FORM

3800N

for Tax Year 2007 and after

Worksheet

• See important instructions on reverse side

Name as Shown on Form 3800N Social Security Number or Nebraska Identification Number

RESEARCH AND DEVELOPMENT CREDIT YEARS

A B C D E

1st Year of Research 1st 2nd 3rd 4th

and Development Succeeding Year Succeeding Year Succeeding Year Succeeding Year

1 Enter applicable tax year end date (month/day/year) . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2 Enter total amount of federal credit allowed (from Federal Form 6765, line 63 or

2

line 65) (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Alternative Methods to Apportion Credit. Complete either lines 3 through 7 or lines 8 through 11.

% % % % %

3 Nebraska property factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

% % % % %

4 Nebraska payroll factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

% % % % %

5 Add lines 3 and 4 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

% % % % %

6 Average property and payroll factors (line 5 ÷ 2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

7 Multiply line 2 x line 6 (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

8 Enter amount of qualified expenses for research and experimental activities in Nebraska 8

9 Enter total amount of qualified expenses for research and experimental activities in

9

all states (from Federal Form 6765, line 9, line 28, or line 53) . . . . . . . . . . . . . . . . . . .

% % % % %

10 Divide line 8 by line 9 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

11 Multiply line 2 x line 10 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

USE OF RESEARCH AND DEVELOPMENT CREDIT

12 Nebraska Research and Development Credit (line 2 OR line 7 OR line 11 x 15%)

12

(see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

13 Amount of credit (refundable to the entity claiming the credit) from line 12 used on

13

Nebraska income tax return . Enter on line 23 of Form 3800N . . . . . . . . . . . . . . . . . . .

14 Amount of credit used for refunds of state sales/use taxes paid on qualifying

14

expenditures (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

15 Amount of credit (nonrefundable) distributed to partners, shareholders, members,

15

or certain fiduciary beneficiaries (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . .

16 Total credit usage (line 13 + 14 + 15) . Total cannot exceed line 12 . . . . . . . . . . . . . . . 16

Schedule A — Distribution of Research and Development Credit

Name of Partner, Social Security Number or Share of Income or Ownership

Amount of Credit

Shareholder, Member or Beneficiary* Nebraska Identification Number (Must Equal 100%)

%

1

%

2

%

3

%

4

%

5

%

6

%

7

%

8

%

9

10 Total (this should equal the amount entered on line 15 of the Research and Development Credit Worksheet above) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Note: Each partner, S corporation shareholder, LLC member, or beneficiary should be notified of the distributed share of the Research and Development Credit .

8-653-2009

2. INSTRUCTIONS

WHO MAY FILE. Any business firm making expenditures LINE 7. Multiply line 2 by the average factor calculated on

in research and experimental (R&D) activities as defined in line 6.

Internal Revenue Code (IRC) § 174 may claim a credit equal LINES 8 AND 9. Enter the total amount of qualified expenses

to 15 percent of the federal credit allowed under IRC § 41. for research and experimental activities in Nebraska and the

total amount of qualified expenses in all states on these lines.

Business firm means any business entity including a

The total amount of qualified expenses is line 9, line 28, or

corporation, fiduciary, sole proprietorship, partnership, joint

line 53 of Federal Form 6765.

venture, limited liability company, or other private entity that

LINE 10. Round the factors to 4 decimal places and enter

is subject to sales tax under Neb. Rev. Stat. § 77‑2703.

as a percent.

WHEN AND WHERE TO FILE. This credit computation

LINE 12. Nebraska Research and Development

worksheet must be completed and attached to the Nebraska

Credit. Multiply the amount on line 2 OR line 7 OR line 11

Incentives Credit Computation, Form 3800N. The credit is

by 15 percent. The business firm may use whichever result

allowed for the first tax year it is claimed and for the four

yields the highest amount. This is the amount of credit to

succeeding tax years.

be claimed on Nebraska Incentives Credit Computation,

Form 3800N, for the year indicated on line 1.

SPECIFIC INSTRUCTIONS

LINE 1. Enter in column A the first tax year end date for LINE 13. The amount of the credit is refundable to the

which the credit is claimed, then enter in the other columns person or entity who created the credit, whether or not there

the applicable tax year end dates that correspond to the is a liability shown on the return.

column A tax year end. LINE 14. Claims may be filed quarterly for refunds of state

sales/use taxes paid, either directly or indirectly, after the

LINE 2. Enter the amount of the federal credit allowed for

filing of the income tax return for the tax year in which the

increasing research activities from line 63 or line 65, as

credit was first allowed. A taxpayer indirectly pays state

appropriate, of Credit for Increasing Research Activities,

sales/use taxes when the taxes are paid by their contractor on

Federal Form 6765, for each applicable tax year.

annexed building materials in a project built for the taxpayer.

If doing business only in Nebraska, skip lines 3 through Local sales/use taxes are not subject to refund. The contractor

11, and multiply the amount on line 2 by 15%. Enter this must either certify the actual amount of taxes paid or certify

amount on line 12, and complete the remainder of the form. that state sales/use taxes were paid on all annexed building

materials. The certification option presumes that 40 percent

If doing business both within and without Nebraska,

of the project’s cost was for building materials on which the

complete either lines 3 through 7, or lines 8 through 11,

tax was paid. The contractor must maintain documentation

depending upon the method of apportionment selected.

to adequately support any certification made.

LINES 3 AND 4. The Nebraska property and payroll factors

LINE 15. Credits must be distributed in the same percentage

are determined pursuant to Neb. Rev. Stat. §§ 77‑2734.12

as income is distributed to the recipients. The credit is a

and 77‑2734.13, respectively. Round the factors to 4 decimal

nonrefundable credit in the hands of the recipient and may

places and enter as a percent.

only be used against the recipient’s Nebraska income tax

LINES 5 AND 6. Round the factors to 4 decimal places and liability. Do not include any amount in the credits distributed

enter as a percent. which were distributed on the Federal Form 6765, line 64.