Download to read offline

![RESEARCH32 33

Rules for creating retail experiences

How do you go about defining the best combination of physical and

digital for your brand? Our research uncovered five overarching rules

to keep in mind when designing the future of your retail experience.

1Retailers must become

more flexible, immersive,

and fit for purpose

Digital extensions — a great interactive

kiosk, mobile app, or sales associate

tool — are no longer enough. Retail

brands must reimagine their business

in the age of the customer.

Digital transformation is on the agenda

of retailers and their boardrooms.

According to a 2015 International

Data Corporation (IDC) study, nearly

two-thirds (64 percent) of Western

European retailers are currently under-

taking a formal digital transformation

5

IDC. “64% of Western European Retailers Currently Undergoing Formal Digital Transformation Effort, While Further 21% About to Start by End of the Year, Says IDC.”

https://www.idc.com/getdoc.jsp?containerId=prUK25829515.

program, while a further 21 percent

were expected to have started one by

the end of 2015. They note that a “race

to digitize [is] taking place among the

largest retailers in Europe.”5

Our research shows that more trans-

formation is sorely needed. If there is

one overarching finding from our study

it is this: The examples that we saw in

market do not go far enough toward

rethinking the retail business for the

digital age.

Based on our research, we see the top

reimagining priorities to be centered

around three main questions:

You’ve been matched:

the output of the ColorIQ process

Sephora’s ColorIQ measures skin color, sets up follow-up purchases of

various foundations, and also offers a hands-on experience in the store.

FIGURE03

1HOW CAN YOU IMPROVE

FLEXIBILITY?

Retailing in the digital age should be

more flexible than in the past. This

means omnichannel and visibility; click

and collect; mobile ordering; ship-to-

home; and all the permutations. Our

leaders — Apple, Argos, and Sephora

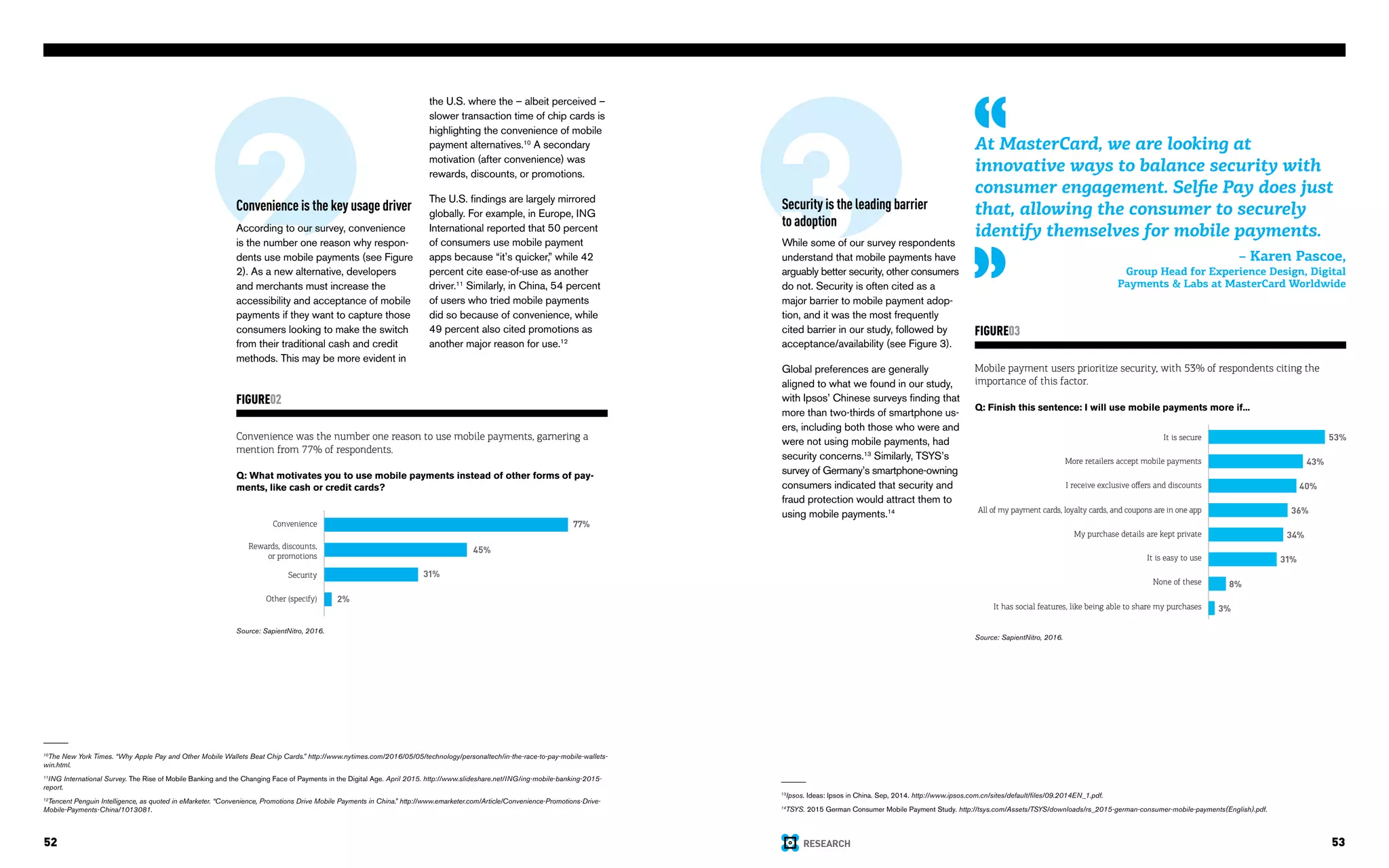

— have all made significant progress in

this area (see Figure 3). In the UK, spe-

cifically in the cities, click and collect/

reserve has been credited with stalling

the decline in footfall. In fact, at one

leading UK retailer, it accounts for the

majority of orders via online platforms.

2HOW CAN YOU MAKE

THE EXPERIENCE MORE

IMMERSIVE?

On the less frequent occasions that

customers do go to the store, they

need to be greeted by great experiences.

Museum quality if you’re selling tech

hardware. Dynamic changing rooms

and great customer service if you’re in

apparel. Smaller spaces. Better tools.

Faster service.

3HOW CAN YOU MAKE

YOUR RETAILING PROPER-

TIES FIT FOR PURPOSE?

Retailing properties (mobile, e-com-

merce, and physical) should be fit for

purpose. Retailers in the digital age

need inventory, but they don’t need as

much inventory. Endless aisle tools,

smartphones, visibility of inventory, and

sales associates (You do have visibility,

right?) all mean more flexibility. Reduce

square footage, invest in community

events, and make the store and brand

be more connected to humans. Look

to recent trends in bookstores and

banks — fewer, smaller, and more

beautiful examples with higher sales

per square foot.](https://image.slidesharecdn.com/reimaginingbusinessintheagefinal-191209221024/75/Reimagining-Business-in-the-Age-of-the-Customer-18-2048.jpg)

![65OUR PERSPECTIVES

Customer experience (CX) has finally reached prime time. It is being recognized

broadly as a key differentiator of the products and services that businesses offer,

no matter what the industry. Business leaders get it: The environments they create

and interactions they foster for their customers define their brands. As such, they

need to pay closer attention to experience design and related disciplines [in-

cluding user experience (UX), customer experience (CX), and human computer

interactions (HCI)].

Along with the aforementioned C-level epiphany, experience designers and product

managers are being inundated with (often contradictory) advice from bloggers,

analysts, and self-proclaimed experts on how to achieve breakthrough experiences.

And, among this rabble, those same product managers have also formed their own

opinions about experience design – opinions which are often heavily influenced by

idiosyncratic brand loyalties.

In a world where digital interactions pervade almost every experience that custom-

ers have with a brand, business leaders can’t afford to get UX wrong. But how can

they get it right when design opinions are endless, design patterns are seemingly

infinite, and consumer interactions and expectations are ever-evolving?

We recommend starting by taking a step back, understanding the foundations of

experience design, and debunking some of the contemporary, mainstream myths.

DISPELLING

5 MYTHS ABOUT

EXPERIENCEDESIGN

PAUL EISEN, PhD](https://image.slidesharecdn.com/reimaginingbusinessintheagefinal-191209221024/75/Reimagining-Business-in-the-Age-of-the-Customer-34-2048.jpg)

![96 97OUR PERSPECTIVES

In a separate question, the culture

and mindset change was the biggest

challenge. One expert noted, “[the

biggest challenge] is the people and

not the technology. Changing people’s

mindset, be it for agile, microservices or

experimentation-orientation, would take

considerable effort.”

In today’s always-on age, customers

are less patient and expect to interact

almost instantly. This requires software

delivery to be transformed into an

outside-in function that plans, builds,

and runs technology according to how

customers move within market spaces.

In this article, we explain how we’ve

helped clients embrace continuous

delivery, and respond to the challenge

of the always-on age. We’ll also share

our latest research into enterprise

IT practices and the current state of

enterprise IT.

A culture of experimentation

The single, greatest key to embracing

continuous delivery is culture, and

systematically building a culture of

rapid change. Both Amazon and

Google emphasize their “fail fast”

culture, with Jeff Bezos, for example,

noting that “[Amazon is] the best place

in the world to fail.” To put it simply,

these firms build and pilot hundreds of

ideas to find the successful ones.5

For

example, Google's 25,000 engineers

reportedly modify 15 million lines of

code across 250,000 files each week.6

The only constant is change.

This experimentation culture is particu-

larly important in retail (or any customer-

facing channel) where it is key to

truly realizing returns from the major

e-commerce, content, or digital market-

ing platform implementation projects

that are now largely complete.

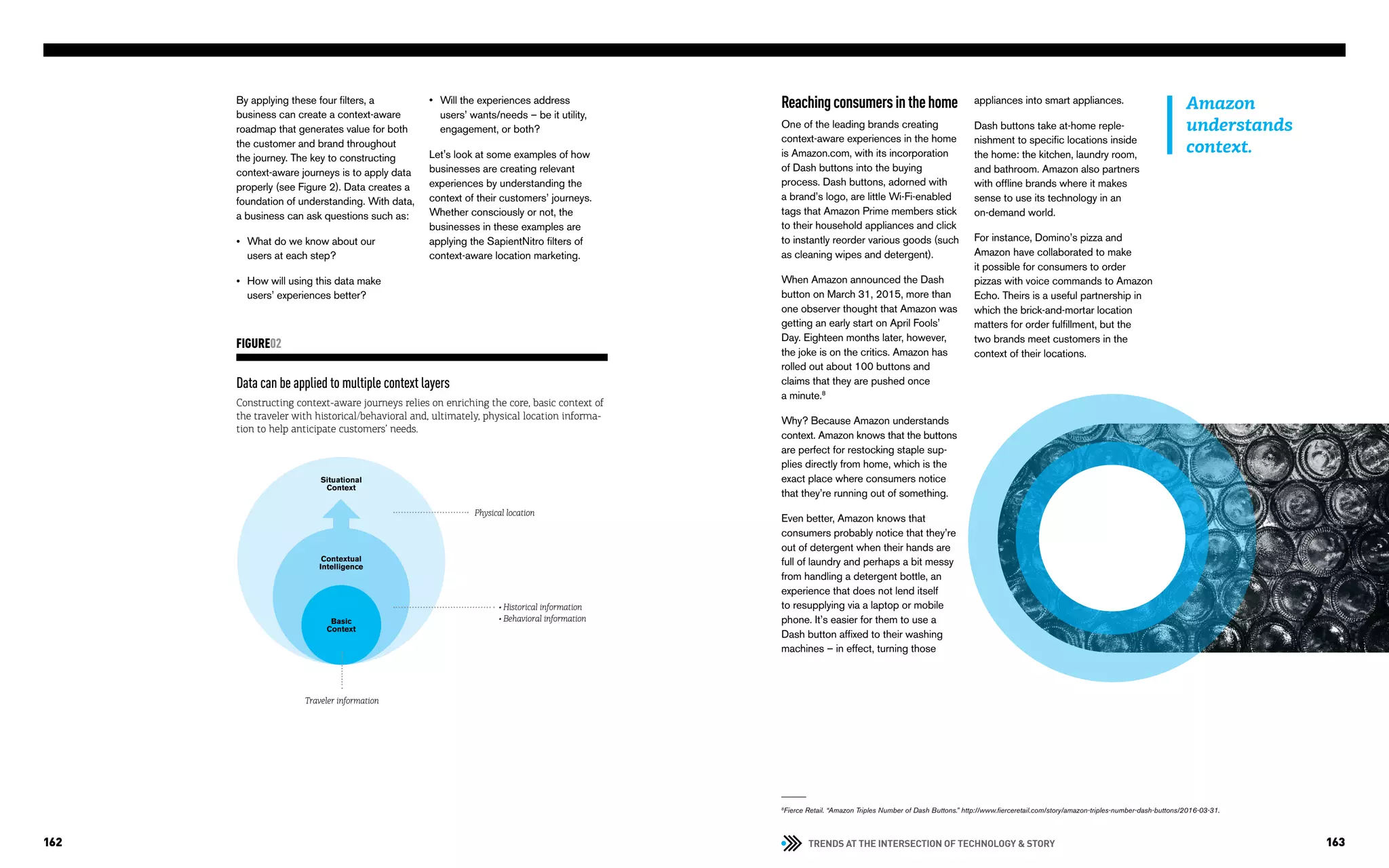

Yet our research shows that just 23

percent of companies support an

experimentation culture (see Figure 1).

Companies which adopt a culture of

experimentation emphasize test and

learn methods, rapid prototyping, and

immediate feedback from real cus-

tomers. The most important process

is sustaining a never-ending cycle of

measuring outcomes, changing quickly

based on feedback, and then putting

the next thing in front of your customers.

Just 23% of companies support an experimentation culture.

FIGURE01

Q: To what extent do you agree/disagree with the following statement: Most com-

panies support an “experimentation culture,” that is, one characterized by “test

and learn” and “small and frequent” methods.

Introducing a shift in mindset

Our approach to continuous delivery

is a bit like a long car trip. In the past,

we have always focused on reaching

the destination, on how to “go live” on

a specific date. It was not about how

the car was working, how bumpy the

ride was, or how we lost our direction

hundreds of times along the way; rather,

it was all about “have we reached

the destination?”

Our new mindset focuses on both the

car and the journey. By focusing on

the car, new traits become important:

the flexibility to adapt to changing

road conditions, the speed to quickly

achieve your goals, and the endurance

to reach the end destination.

Having a solid engineering methodo-

logy is like having a good car which

is maintained well with excellent road

conditions. It doesn’t guarantee that

you'll make it to your destination safely

and comfortably, but it makes the pros-

pect a lot more likely.

Autonomous product teams

To help large corporations embrace

an experimentation culture, we’ve

developed and refined an “Enterprise

Startup” approach. We start with an

autonomous product team that runs its

own profit and loss (P&L) and reports

to internal investors, even as it also

makes decisions on a daily basis.

The team tests and fails fast by deploy-

ing minimum viable products (MVPs)

and then iterating.

Organize around customer journeys

We organize product teams around

customer journeys, not around traditional

functional areas. For example, rather

than having a team focused on product

development, we focus it around the

customer need. Instead of mortgage

origination, we organize the team on

the “buying a home” customer journey.

Use best-in-class agile methods

We also use best-in-class agile me-

thods. This means shifting the IT

culture from long product development

cycles and extended quality assurance

(QA) periods to daily releases and

continuous QA.

For example, Marks and Spencer, like

most retailers, had traditionally done a

code freeze for several months during

the holidays. This year that changed:

They conducted nineteen code releases

during the peak holiday season. The

result was an improved product and

millions of new data points on customer

behaviors in the new experience.

40%

30%

20%

10%

0%

Strongly

disagree

Disagree Neither agree

nor disagree

Agree Strongly

agree

38%

33%

5%

23 percent of

companies support

experimentation

culture

13%

10%

90%

IDC prediction

of IT projects will be

rooted in the principles

of experimentation,

speed, and quality by

the end of 2018.4

23%

Just

of companies support an

“experimentation culture.”

Source: SapientNitro, 2016.

4

IDC. IDC FutureScape CIO Agenda Predication 5: Driving Experimentation, Speed, and Quality. http://www.idc.com/getdoc.jsp?containerId=US40548115.

5

Forbes. “Jeff Bezos Calls Amazon ‘Best Place in the World to Fail’ in Shareholder Letter.” http://www.forbes.com/sites/ryanmac/2016/04/05/jeff-bezos-calls-amazon-best-place-in-

the-world-to-fail-in-shareholder-letter/.

6

Wired. “Google is 2 Billion Lines of Code – And It’s All in One Place.” http://www.wired.com/2015/09/google-2-billion-lines-codeand-one-place/.

7

For more information, see “About the research” on page 106.

Source: SapientNitro, 2016.7](https://image.slidesharecdn.com/reimaginingbusinessintheagefinal-191209221024/75/Reimagining-Business-in-the-Age-of-the-Customer-50-2048.jpg)

![INDUSTRY VOICES & GAME CHANGERS112 113

Over the last six years, RBS has re-

leased a series of innovations and inter-

nal changes in order to adapt to a more

competitive marketplace. RBS has

transformed its organization to focus

on customer experience, building on

its history of deep product and channel

centricity. Guided by the promise of

“Helpful Banking,” the organization has

been building a digitally-led culture,

reimagining internal structures, and sub-

sequently bettering its customers’ lives.

Organizational change: Creating

journey managers

The reimagining of RBS’s digital busi-

ness started with its people – more

specifically, its product managers. Pre-

viously, product managers across RBS

worked in organizational silos, such as

checking accounts, savings accounts,

mortgages, etc. They rarely communi-

cated across the lines and customer

feedback suggested that customer

requests were, at times, getting lost in

the handoff between specialists. Fur-

thermore, customers reported that they

were not getting holistic “life advice.”

RBS reached the conclusion that an

entirely new role needed to be created

to drive business transformation and

improve the customer experience. This

role was needed in order to disrupt

traditional mindsets, look across pro-

ducts and services, and collaborate

with those who would continue to ma-

nage and own existing products.

To serve this purpose, RBS created the

position of “journey manager.” Journey

managers are individuals who are con-

cerned with customers’ aspirations and

goals. They are oriented not around

products, but rather around customers

and their major financial moments –

including opening their first accounts,

saving money for university, and buying

a home.

In 2012, RBS had five journey managers.

Three years later, there were sixty.

A digitally-led culture and

simplified user experience

Over the years, RBS – like many banks

– has developed multiple website and

web platforms to support its business

needs at specific moments in time.

Often, these proprietary platforms lived

on at a growing cost both financially

and in terms of maintaining a distinct

user experience.

When reimagining its business, however,

RBS saw an opportunity to focus on

the simplification of its digital estates.

Over the last 18 months, RBS has

been on a journey to consolidate over

200 distinct web platforms into a single

one, thereby increasing collaboration

among business teams and simplifying

the user experience.

In addition, RBS introduced an initiative

aimed at increasing the overall digital

IQ of the organization and helping it

transform into a digitally-led company. To

achieve this, two major steps were taken.

The first saw RBS develop agency-like

digital studios in both London and

Edinburgh. These studios began trans-

forming the organization's culture and

technology systems from the inside out

Our busiest

branch...is the

7:01 [train]

from Reading

to Paddington –

over 167,000

of our customers

use our Mobile

Banking app

between 7am

and 8am...

every day.

– Ross McEwan,

CEO of RBS3

via Scrum collaborative development

areas, cross-functional teams, and the

mindset of a more nimble enterprise

startup.

The second step was “Bank of APIs,”

a series of hackathons run by RBS and

open to both staff and external par-

ticipants. Spanning the brand’s three

major geographies (London, Edinburgh,

and India), this initiative further commu-

nicates RBS’s new way of working and

dedication to innovation.

And that was just the start.

The innovation imperative

With the new journey managers and

refined product mix, RBS was working

hard to address consumers’ core

needs. However, to effectively reima-

gine their business, RBS’s leaders

needed to reinvent the customer

journey across all channels and truly

put customers in the center.

But how was the organization going to

address the customer experience holisti-

cally? RBS realized that game-changing

innovation requires an end-to-end view

of the customer experience. RBS was

able to introduce a series of innovative

services to the market over twenty-four

months by combining customer insights

from the journey managers, a team

making rapid prototypes, and a nascent

crowdsourcing/co-creation platform.

The following pages highlight the

innovations made in three major areas:

optimizing existing web properties,

building new tools based on customer

needs, and aggressively embracing the

latest mobile technology.

112

3

BBC. “RBS: Ross McEwan Speech in Full.” http://www.bbc.co.uk/news/business-your-money-26365616.](https://image.slidesharecdn.com/reimaginingbusinessintheagefinal-191209221024/75/Reimagining-Business-in-the-Age-of-the-Customer-58-2048.jpg)

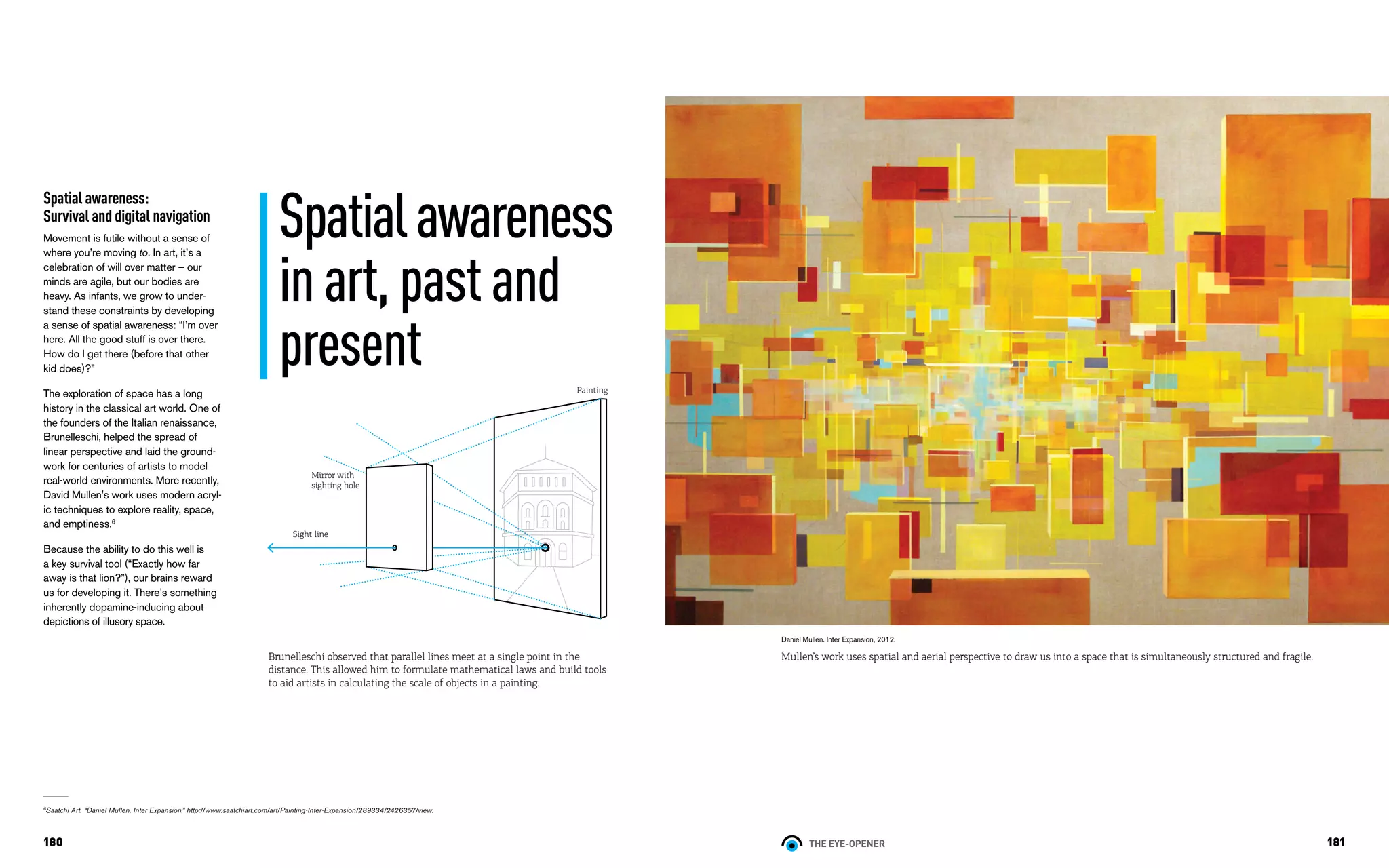

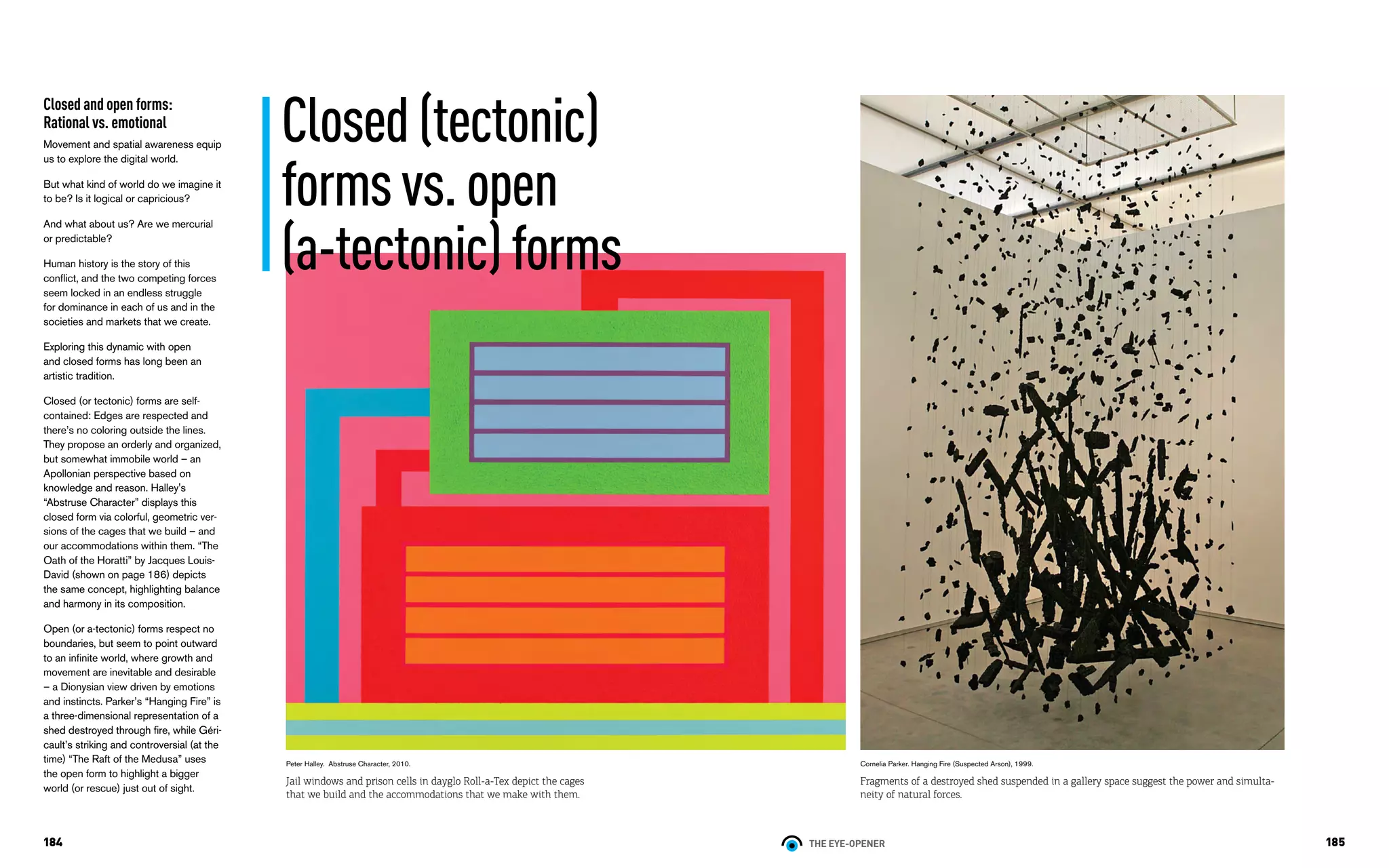

![190

Conclusion

Throughout this piece, we’ve used the

word art to loosely reference what

Daniel Kahneman calls “System 1

thinking” which is “fast…intuitive,

associative, metaphorical, automatic,

impressionistic…[and the] secret

author of many of the choices and judg-

ments [that we] make.”12

Art depicts

and provokes instinctual reactions that

are the sum of 40,000 years of human

life, observation, and learning – allowing

it to uncover valuable wisdom.

By contrast, digital technology has

grown out of Kahneman’s “System 2

thinking”: slow, deliberate, and conside-

red. But “digital” in the broader sense

is young. It’s a teenager full of energy,

with an appetite for the new, but a very

short attention span.

So what can the digital world learn

from art practice?

We’ve touched on four main themes:

existential evidence, kinesis and move-

ment, spatial awareness, and open vs.

closed forms.

In each, classical and modern art

has much to offer. Early French cave

paintings show self-awareness and

evidence of being. Boccioni’s flowing

bronze “Unique Forms of Continuity

in Space” highlights movement and

energy. Mullen’s “Inter Expansion” uses

acrylic paint and shape to suggest

depth and spatial awareness. And

closed and open forms are highlighted

in Parker’s “Hanging Fire” and Géri-

cault’s “The Raft of the Medusa.”

These core themes resonate in today’s

world with just as much urgency and

life. Touch ID and the role of persona-

lization emphasize the importance of

identity. The rise of video and use of

motion and animation reinforce the

import of kinesis. The desktop meta-

phor in most operating systems and

evolution of VR depict how spatial

awareness has continued relevance.

And the debate at the heart of the

nature of the Internet – around its open

or closed system, and the architecture

of its websites – reinforces that key

point as well.

We believe that the notion of tension

is what ties art to digital technology.

Artists love tension because it excites:

complementary colors sizzle and con-

flicts drive drama. It’s an appetite for

“the opposite” by which you recognize

a truly creative thinker – one with the

ability to take seemingly unrelated, even

opposing, things and make them into

something new.

To grow well, digital will need to ma-

ture, deepen, and acquire art’s wisdom

of human experience. Therefore, a

union of technology and emotion is

needed: a mutually beneficial symbiosis

to give art relevance and digital a soul.

Matthew Maxwell

Associate Creative Director,

SapientNitro London

mmaxwell@sapient.com

12

Daniel Kahneman. Thinking, Fast and Slow. Penguin Books. 2010.](https://image.slidesharecdn.com/reimaginingbusinessintheagefinal-191209221024/75/Reimagining-Business-in-the-Age-of-the-Customer-97-2048.jpg)

The document discusses the need for businesses to undergo transformative changes in response to evolving customer expectations and technological advancements. It emphasizes that leaders must not only improve efficiency but also focus on the right strategic changes necessary for long-term relevance. The insights gathered highlight that many organizations understand the importance of digital business transformation but struggle to prioritize and implement it effectively.