Download to read offline

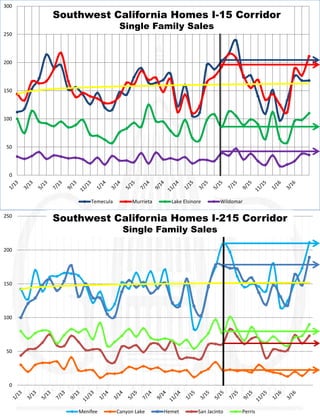

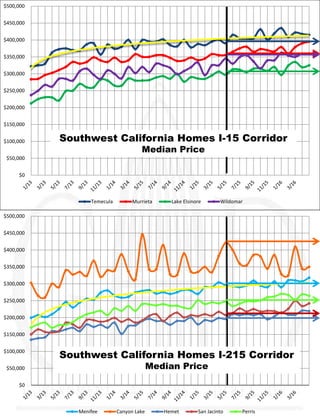

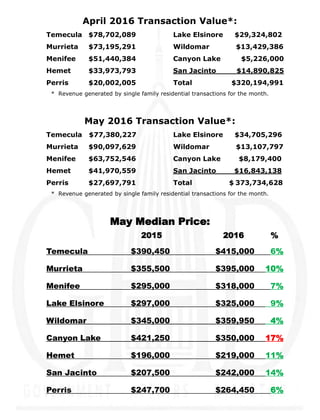

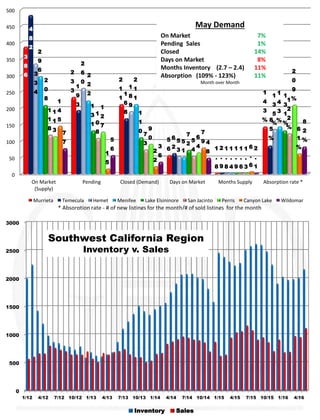

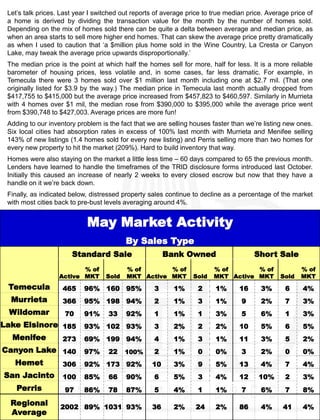

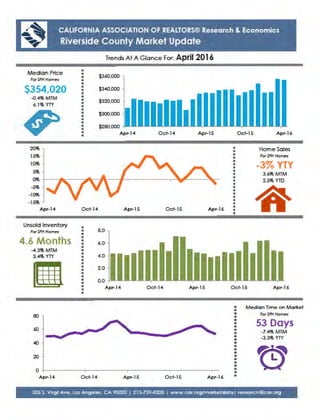

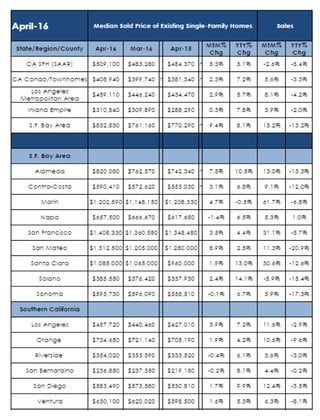

This document discusses recent housing market trends in Southwest California. It notes that in May, home sales increased 14% from the previous month while median home prices rose 4%. Inventory remains low across most cities in the region, at 2 months or less of supply. The fast pace of home sales compared to new listings coming on the market has led to absorption rates over 100% in many cities, making it difficult to build up inventory. Distressed property sales continue to decline as a percentage of the total market.