Raportu analityczny S&P Global Ratings dotyczący sytuacji budżetowej polskich samorządów

•

0 likes•6 views

Podsumowanie: Raport przedstawia przegląd sytuacji budżetowej polskich samorządów, skupiając się na wzorcach dochodów i wydatków, poziomach zadłużenia oraz zrównoważeniu finansowym. Raport zauważa, że polskie samorządy w ostatnich latach stanęły przed znaczącymi wyzwaniami fiskalnymi, wynikającymi z szeregu czynników, w tym zmian w krajowej polityce fiskalnej, wzrostu wydatków związanych z usługami społecznymi i infrastrukturą oraz trudności w pozyskiwaniu dochodów z lokalnych podatków i opłat. Raport kończy, że chociaż ogólna sytuacja fiskalna polskich samorządów pozostaje trudna, istnieją pewne pozytywne oznaki poprawy, w tym silniejsze praktyki planowania i zarządzania budżetem oraz zwiększone wsparcie ze strony rządu

Recommended

Recommended

More Related Content

Similar to Raportu analityczny S&P Global Ratings dotyczący sytuacji budżetowej polskich samorządów

Similar to Raportu analityczny S&P Global Ratings dotyczący sytuacji budżetowej polskich samorządów (20)

More from CEO Magazyn Polska

More from CEO Magazyn Polska (20)

Recently uploaded

Recently uploaded (20)

Raportu analityczny S&P Global Ratings dotyczący sytuacji budżetowej polskich samorządów

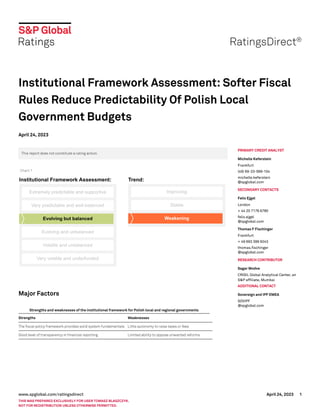

- 1. Institutional Framework Assessment: Softer Fiscal Rules Reduce Predictability Of Polish Local Government Budgets April 24, 2023 This report does not constitute a rating action. Chart 1 Major Factors Strengths and weaknesses of the institutional framework for Polish local and regional governments Strengths Weaknesses The fiscal policy framework provides solid system fundamentals Little autonomy to raise taxes or fees Good level of transparency in financial reporting Limited ability to oppose unwanted reforms Institutional Framework Assessment: Softer Fiscal Rules Reduce Predictability Of Polish Local Government Budgets April 24, 2023 PRIMARY CREDIT ANALYST Michelle Keferstein Frankfurt (49) 69-33-999-104 michelle.keferstein @spglobal.com SECONDARY CONTACTS Felix Ejgel London + 44 20 7176 6780 felix.ejgel @spglobal.com Thomas F Fischinger Frankfurt + 49 693 399 9243 thomas.fischinger @spglobal.com RESEARCH CONTRIBUTOR Sagar Modve CRISIL Global Analytical Center, an S&P affiliate, Mumbai ADDITIONAL CONTACT Sovereign and IPF EMEA SOVIPF @spglobal.com www.spglobal.com/ratingsdirect April 24, 2023 1 THIS WAS PREPARED EXCLUSIVELY FOR USER TOMASZ BLASZCZYK. NOT FOR REDISTRIBUTION UNLESS OTHERWISE PERMITTED.

- 2. Recent Developments Recently introduced tax reforms, known as the "Polish Deal", lowered revenue for local and regional governments (LRGs) (see chart 3). This is only partly compensated by higher capital transfers from the central government, according to S&P Global Ratings' understanding. We consider that the overall structure of the tax system leaves Polish LRGs with limited room to directly benefit from higher tax collection (operating revenue). Monthly transfers from the central government for personal income tax (PIT) and corporate income tax (CIT) are not directly adjusted for currently elevated inflation. That is an issue for LRGs given our forecast of higher-for-longer expenditure, due to energy and commodity prices, and an expansion of the services they provide. The central government will partly compensate for those losses, but we expect LRGs will have to accept some weakening of budgetary performance. In anticipation of weaker performance, the central government has loosened regulations--specifically rules for balanced budgets and debt servicing --that were key to the institutional framework's strength. While we expect that the loosening of the rules will be reversed, that could take a few years. We believe the temporary relaxation of the legal limits governing the debt service ratio and the balanced-budget calculation (specifically relating to COVID-19 and refugee expenditures) could affect the public finance system's predictability and the flexibility of revenue. The temporary suspension of those rules, which is effective until 2025, could also set a precedent that will make rule bending a structural feature of the Polish LRGs' financing system, particularly considering that most related costs and debt issuance are excluded. This could reduce predictability, including with regards to investment planning. In particular, we see risks that the temporary measures might be prolonged or extended, leading to unsustainable spending and higher debt burdens. www.spglobal.com/ratingsdirect April 24, 2023 2 THIS WAS PREPARED EXCLUSIVELY FOR USER TOMASZ BLASZCZYK. NOT FOR REDISTRIBUTION UNLESS OTHERWISE PERMITTED. Institutional Framework Assessment: Softer Fiscal Rules Reduce Predictability Of Polish Local Government Budgets

- 3. Chart 2 Predictability Finance system reforms are usually planned well in advance and subject to only minor changes, but the recent relaxation of fiscal rules could affect predictability The Polish public finance system is evolving, generally through minor adjustments. It features some operational freedoms and is closely tied to central government funding and policy. We consider that changes to the system are usually planned well in advance with a reasonable degree of transparency. Several updates have recently been introduced to the Public Finance Act www.spglobal.com/ratingsdirect April 24, 2023 3 THIS WAS PREPARED EXCLUSIVELY FOR USER TOMASZ BLASZCZYK. NOT FOR REDISTRIBUTION UNLESS OTHERWISE PERMITTED. Institutional Framework Assessment: Softer Fiscal Rules Reduce Predictability Of Polish Local Government Budgets

- 4. and will be gradually implemented over the period to 2026. The draft of that act doesn't contain significant changes and is in effect a tweaking of existing procedures. We believe the recent relaxation of the debt-service rule could reduce system predictability. That would particularly be the case if rules allowing higher spending and debt aren't reinstated, possibly resulting in future financial difficulties for some LRGs. LRGs' influence on reforms is limited LRGs' ability to oppose unwanted changes in the legislation is limited as they do not have veto rights. Nevertheless, they can influence or oppose reforms through parliament and via their representation in standing committees and different associations. Local and regional government associations have a track record of lobbying for legislative change, with varying degrees of success depending on their influence. Revenue And Expenditure Balance Revenue is adequate to cover expenditure, however changes in the tax law further limits revenue flexibility Generally, Polish LRGs demonstrate a good match between revenue and expenditure. Operating surpluses are strong, with moderate deficits after capital accounts, on average (see chart 3). The central government finances schoolteachers' basic salaries, social support measures, and provides equalization subsidies to LRGs that have a weaker revenue base. A combination of fees, local taxes, and shared state taxes (predominantly PIT) is generally sufficient to cover other operating spending. LRGs also receive substantial EU grants to help finance capital expenditure (capex). www.spglobal.com/ratingsdirect April 24, 2023 4 THIS WAS PREPARED EXCLUSIVELY FOR USER TOMASZ BLASZCZYK. NOT FOR REDISTRIBUTION UNLESS OTHERWISE PERMITTED. Institutional Framework Assessment: Softer Fiscal Rules Reduce Predictability Of Polish Local Government Budgets

- 5. Chart 3 We consider that LRGs' have limited ability to increase revenue because shared taxes and central government subsidies contribute around 76% of operating revenue (see chart 4). Most of the central government subsidies are earmarked for education and social care. In some cases that funding is topped up by LRGs from their own revenue (for example, for teacher salaries), especially in bigger cities. Modifiable taxes, which are predominately property-related or LRGs' fees, contribute only a small part of the revenue, leaving the sector exposed to decisions made at the central government level. www.spglobal.com/ratingsdirect April 24, 2023 5 THIS WAS PREPARED EXCLUSIVELY FOR USER TOMASZ BLASZCZYK. NOT FOR REDISTRIBUTION UNLESS OTHERWISE PERMITTED. Institutional Framework Assessment: Softer Fiscal Rules Reduce Predictability Of Polish Local Government Budgets

- 6. Chart 4 The formula-based equalization system is fairly robust and reduces the wealth gap by requiring wealthier LRGs to contribute a share of their revenue to weaker LRGs. We consider it, however, to be less advanced and efficient compared with similar systems elsewhere in Europe, especially those of developed-market peers. An LRG becomes a recipient or provider of funds depending on its tax revenue per capita. The equalization system also considers some demographic characteristics, for example population density, unemployment, and infrastructure. Polish LRGs have marginally greater flexibility to adjust expenditure than revenue. Still, the legal requirement to maintain at least balanced operating budgets limits Polish LRGs ability to undertake significant operational spending. Their main expenditure responsibilities are wages for education and social workers, with these payments conducted on behalf of the central government (see chart 5). Bigger LRGs typically have to contribute additional funding from their revenue to state-delegated tasks to comply with high service standards. Investment spending usually aligns with the distribution cycle of funds from the EU budget--increasing toward the end of that cycle. This implies that most capex is financed by grants rather than LRGs' own resources. We note the risk of debt increasing, or of cutbacks to necessary investment spending, should Polish LRGs not receive sufficient grants in the new EU funding cycle. www.spglobal.com/ratingsdirect April 24, 2023 6 THIS WAS PREPARED EXCLUSIVELY FOR USER TOMASZ BLASZCZYK. NOT FOR REDISTRIBUTION UNLESS OTHERWISE PERMITTED. Institutional Framework Assessment: Softer Fiscal Rules Reduce Predictability Of Polish Local Government Budgets

- 7. Chart 5 We expect debt accumulation will remain contained. Moderate deficits over recent years, due to restrictive fiscal rules and investment grants from the EU, have had a positive impact on the stock of debt at the local level. We project LRGs' direct debt to decrease to 30% of operating revenue in 2025, down from 35% in 2016 (see chart 6). We anticipate LRGs will rely on a combination of debt issuance, cash reserves, and EU financing to support capital spending, especially over 2022-2023. www.spglobal.com/ratingsdirect April 24, 2023 7 THIS WAS PREPARED EXCLUSIVELY FOR USER TOMASZ BLASZCZYK. NOT FOR REDISTRIBUTION UNLESS OTHERWISE PERMITTED. Institutional Framework Assessment: Softer Fiscal Rules Reduce Predictability Of Polish Local Government Budgets

- 8. Chart 6 Fiscal Policy Framework Is A Key Strength The fiscal policy framework prevents fast debt accumulation due to its tough balancing restrictions, in our view. Polish public finance law limits an LRG's debt servicing to the average net surplus over the past three- or seven-years (depending on the period initially chosen by the LRG) of operating revenue and privatization proceeds, less operating expenditures. Borrowing and guarantees for projects co-financed with the EU and short-term borrowings for liquidity purposes repaid within the financial year are excluded from the debt servicing limit. This regulation also indirectly stops debt accumulation at LRGs where the operating balance has been negative for more than one year. There is, currently, a temporary relaxation of the limit on the debt service ratio calculation for increases caused by refugee assistance and investment spending related to the strategic investment program (as outlined in the recent tax reform). LRGs are legally required to have balanced budgets, excluding reserves and unassigned resources. The balancing rule was adjusted in 2022 so that the deficit of one year will have to be covered by current revenue and specified revenue in another financial year, instead of only by current revenue. To provide additional flexibility during the current difficult period, LRGs have been given the leeway to show an average balanced budget for 2023-2025. Despite the temporary relaxation of rules governing debt accumulation and budget balance, we www.spglobal.com/ratingsdirect April 24, 2023 8 THIS WAS PREPARED EXCLUSIVELY FOR USER TOMASZ BLASZCZYK. NOT FOR REDISTRIBUTION UNLESS OTHERWISE PERMITTED. Institutional Framework Assessment: Softer Fiscal Rules Reduce Predictability Of Polish Local Government Budgets

- 9. expect LRGs' debt burdens to remain controlled. This is due in part to the higher interest rate environment, which discourages borrowing, and an expected reduction in investment spending in 2024. Extraordinary Support Is Generally Provided As Emergency Loans The Polish constitution guarantees the legal structure of the public finance system, but it does not specify the type of financial support that can be provided in case of need. The only type of support that is defined by law are emergency loans, for which an insignificant amount of funding is set aside each year. The system was, for example, tested in 2013-2014, after Mazovia Voivodeship, a province located in east-central Poland, was unable to conduct some payments on time due to administrative issues, ultimately resulting in the central government providing loans. Because political considerations play a role when drawing on support, we assume that timely debt servicing is not necessarily assured in case of need, and that the mechanism can't be considered a reliable bail-out procedure. Emergency loans are used widely, and their outstanding amount is published quarterly. The central government has also provided additional funds for investment spending for LRGs to support economic growth in the wake of the COVID-19 pandemic and the energy crisis. Transparency And Accountability Transparency and institutionalization of budgetary process are sound We consider that Polish LRGs demonstrate a fair level of transparency and accountability. The distribution of power between the administrations and councils is transparent, with a clear definition of roles and responsibilities. Roles and responsibilities between elected officials and managers are defined in the Public Finance Act and made public via authority websites. Minutes and records of meetings are generally published on websites but are not required by law, according to our knowledge. We regard the monitoring and control over municipal enterprises as prudent. Reasonable disclosure and mixed cash-accrual accounting supports fiscal rules Accounting standards are clear and uniform, although largely cash-based and unconsolidated. Publication of balance sheets provides some additional information. Budgetary process and information are clearly defined by law, quarterly execution data is required and publicly disclosed on the Ministry of Finance website with some time lag. LRGs are required to prepare annual financial statements and multi-annual frameworks for at least the current financial year and the next three years. These include detailed long-term infrastructure investment plans and their financing for entirety of contract. Budgets and financial plans are usually built around debt service calculation, ensuring fiscal sustainability. Disclosure and information on government-related entities is also required by law, but not necessarily publicly available. www.spglobal.com/ratingsdirect April 24, 2023 9 THIS WAS PREPARED EXCLUSIVELY FOR USER TOMASZ BLASZCZYK. NOT FOR REDISTRIBUTION UNLESS OTHERWISE PERMITTED. Institutional Framework Assessment: Softer Fiscal Rules Reduce Predictability Of Polish Local Government Budgets

- 10. Control levels and reliability of information are in line with local peers The Polish Ministry of Finance monitors the performance and financial strength of LRGs closely and publishes its reports on local budget execution and indebtedness quarterly. We note that some LRGs publish reports monthly. There is no requirement for an independent financial audit, but the state-controlled departments check the compliance of LRG budgets and performance reports as required by public finance law. Trend: Weakening We have revised our trend for the institutional framework for Polish LRGs to weakening from stable. We could lower our institutional framework assessment if the temporary suspension of the fiscal and debt rule becomes a structural feature of the framework. This could come for example from excluding additional expenditures from fiscal rules or by extending the suspension for an unspecified period. We believe that could lower the predictability of the overall system, lead to a significant weakening of budgetary performance, and to higher debt burdens. We could consider revising our assessment to stable if we saw a smooth return to previous rules. Related Criteria and Research - Institutional Framework Assessments For Local And Regional Governments Outside Of The U.S., Oct. 18, 2022 - Methodology For Rating Local And Regional Governments Outside Of The U.S., July 15, 2019 www.spglobal.com/ratingsdirect April 24, 2023 10 THIS WAS PREPARED EXCLUSIVELY FOR USER TOMASZ BLASZCZYK. NOT FOR REDISTRIBUTION UNLESS OTHERWISE PERMITTED. Institutional Framework Assessment: Softer Fiscal Rules Reduce Predictability Of Polish Local Government Budgets

- 11. www.spglobal.com/ratingsdirect April 24, 2023 11 THIS WAS PREPARED EXCLUSIVELY FOR USER TOMASZ BLASZCZYK. NOT FOR REDISTRIBUTION UNLESS OTHERWISE PERMITTED. Institutional Framework Assessment: Softer Fiscal Rules Reduce Predictability Of Polish Local Government Budgets STANDARD & POOR’S, S&P and RATINGSDIRECT are registered trademarks of Standard & Poor’s Financial Services LLC. S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com (subscription), and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available at www.standardandpoors.com/usratingsfees. S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain non-public information received in connection with each analytical process. To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves the right to assign, withdraw or suspend such acknowledgment at any time and in its sole discretion. S&P Parties disclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of an acknowledgment as well as any liability for any damage alleged to have been suffered on account thereof. Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P’s opinions, analyses and rating acknowledgment decisions (described below) are not recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives. Rating-related publications may be published for a variety of reasons that are not necessarily dependent on action by rating committees, including, but not limited to, the publication of a periodic update on a credit rating and related analyses. No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor’s Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages. Copyright © 2023 by Standard & Poor’s Financial Services LLC. All rights reserved.