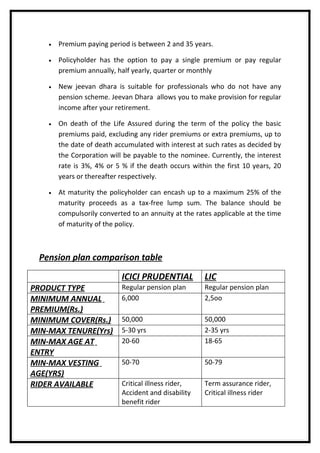

The document compares retirement plans from ICICI Prudential and LIC. Both plans allow individuals to invest regularly over a period of time and then receive pension payments starting at a chosen retirement age. ICICI Prudential's "Forever Life" plan provides life insurance coverage and allows individuals to choose their retirement date and pension payment options. LIC's "Jeevan Suraksha" and "Jeevan Dhara" plans similarly allow individuals to invest regularly for a pension and include bonus payments and life coverage. The plans differ in their minimum premium amounts, coverage amounts, investment periods, eligible ages, and riders offered.