Downloaded 14 times

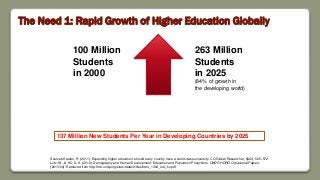

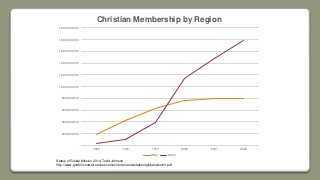

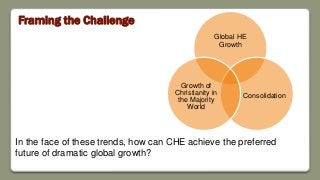

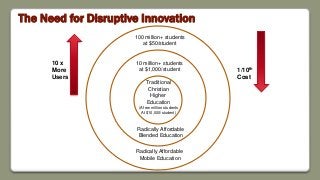

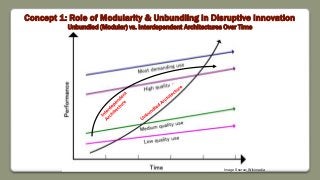

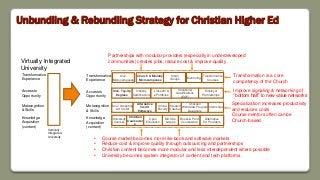

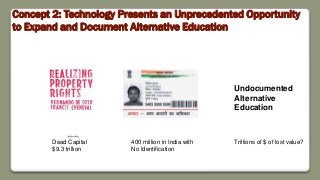

Dr. Andrew Sears discusses the need for a modular global Christian educational ecosystem to address rapid growth in higher education, particularly in the developing world, where non-Western Christianity is on the rise. He proposes a transformative model of Christian higher education that employs innovative, affordable, and modular approaches to learning, leveraging technology for broader accessibility. The document outlines various strategies and frameworks for achieving a more diverse and inclusive educational landscape while ensuring quality and relevance in the face of global changes.