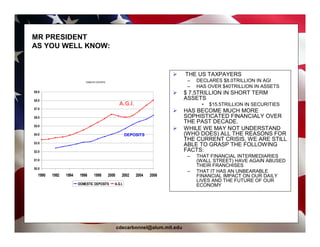

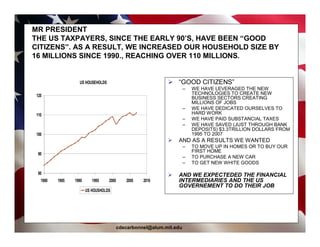

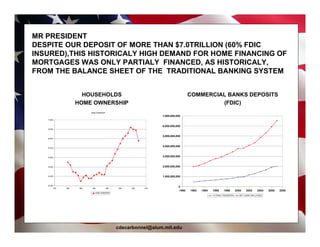

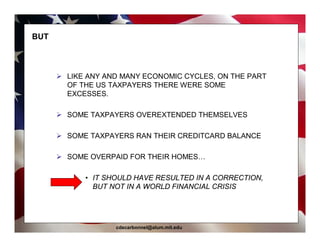

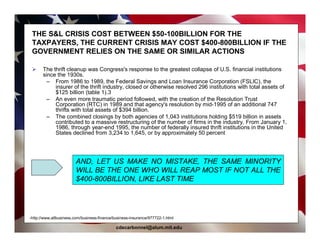

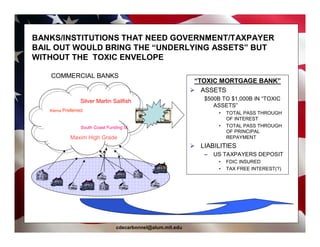

The document appears to be an open letter or proposal from a US taxpayer to President Obama regarding the financial crisis and its impact on taxpayers. It summarizes that taxpayers have lost confidence in the financial system due to the crisis and lack of a clear solution. It also notes that taxpayers have taken responsible actions like working hard, paying taxes, and saving over $3.3 trillion in bank deposits since 1995 but still want their basic needs met. The letter urges the President to restore taxpayer confidence by providing an understandable solution to the current problems.

![United Health Group [PDF Document] Form 10-Q](https://cdn.slidesharecdn.com/ss_thumbnails/1016488-thumbnail.jpg?width=640&height=640&fit=bounds)