Downloaded 14 times

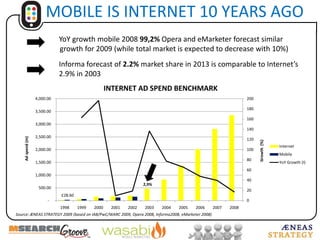

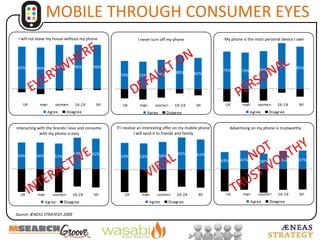

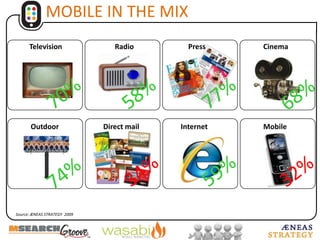

This document summarizes research on the mobile advertising market from 2009. Key findings include: 1) Mobile advertising was a tiny fraction (0.04%) of the overall advertising market but growing rapidly. 2) Consumer attitudes were mixed, with many seeing mobile as personal but not fully trusting mobile ads. 3) Success would depend on addressing privacy concerns, relevance of ads, and incentivizing consumers. 4) While challenges remained around measurement and inventory, the future potential of location-based mobile ads was seen as large. Cooperation across the mobile ecosystem would be critical to realize this potential.