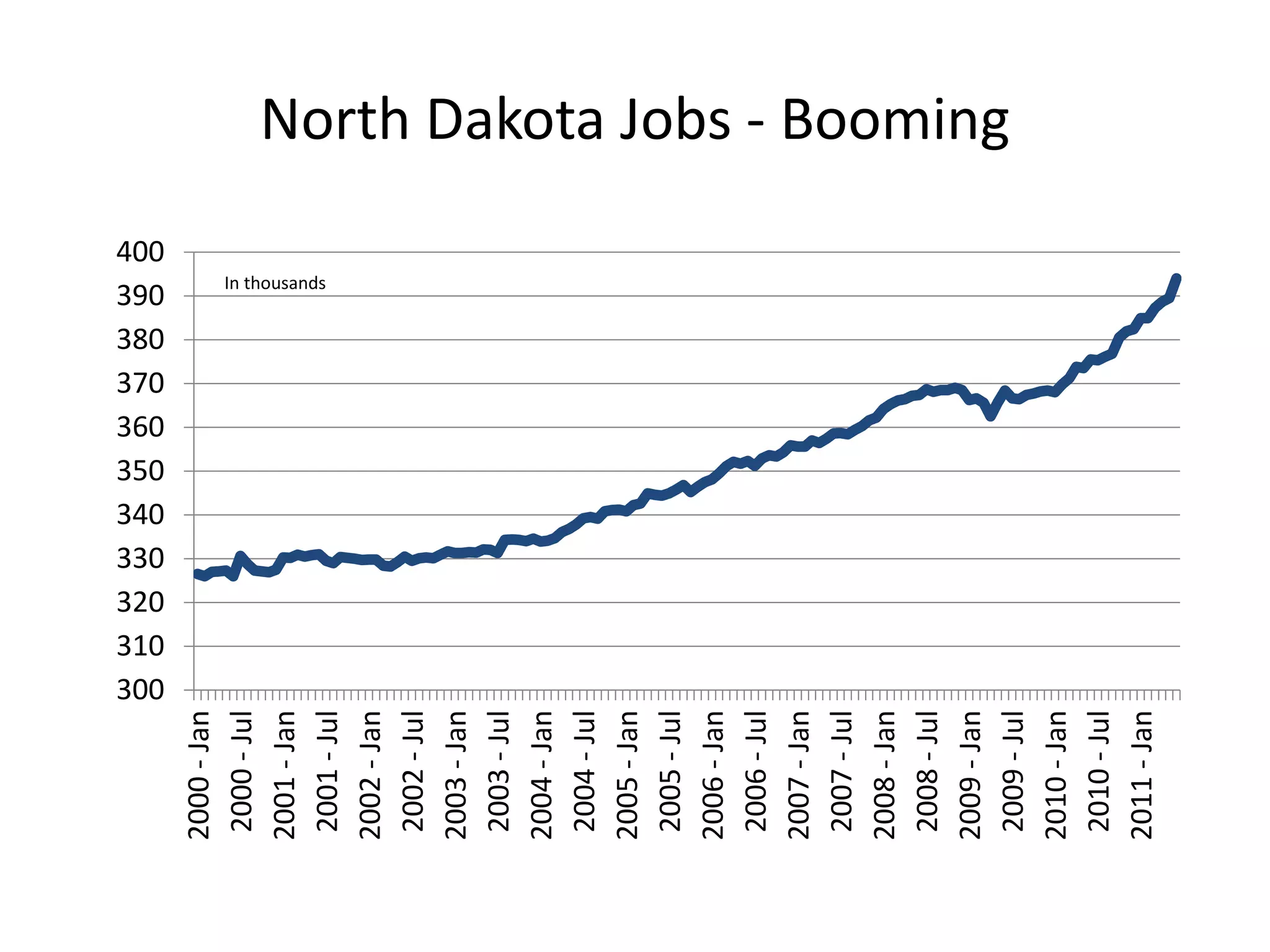

This document summarizes a presentation by Lawrence Yun, Chief Economist of the National Association of Realtors, on the housing market and economic outlook. It includes charts and data on existing home sales, mortgage rates, housing starts, home prices, jobs, unemployment and other economic indicators. The presentation analyzes improving and worsening factors for the housing market and concludes that while the economic recovery is continuing, growth is slower than desired.