Download to read offline

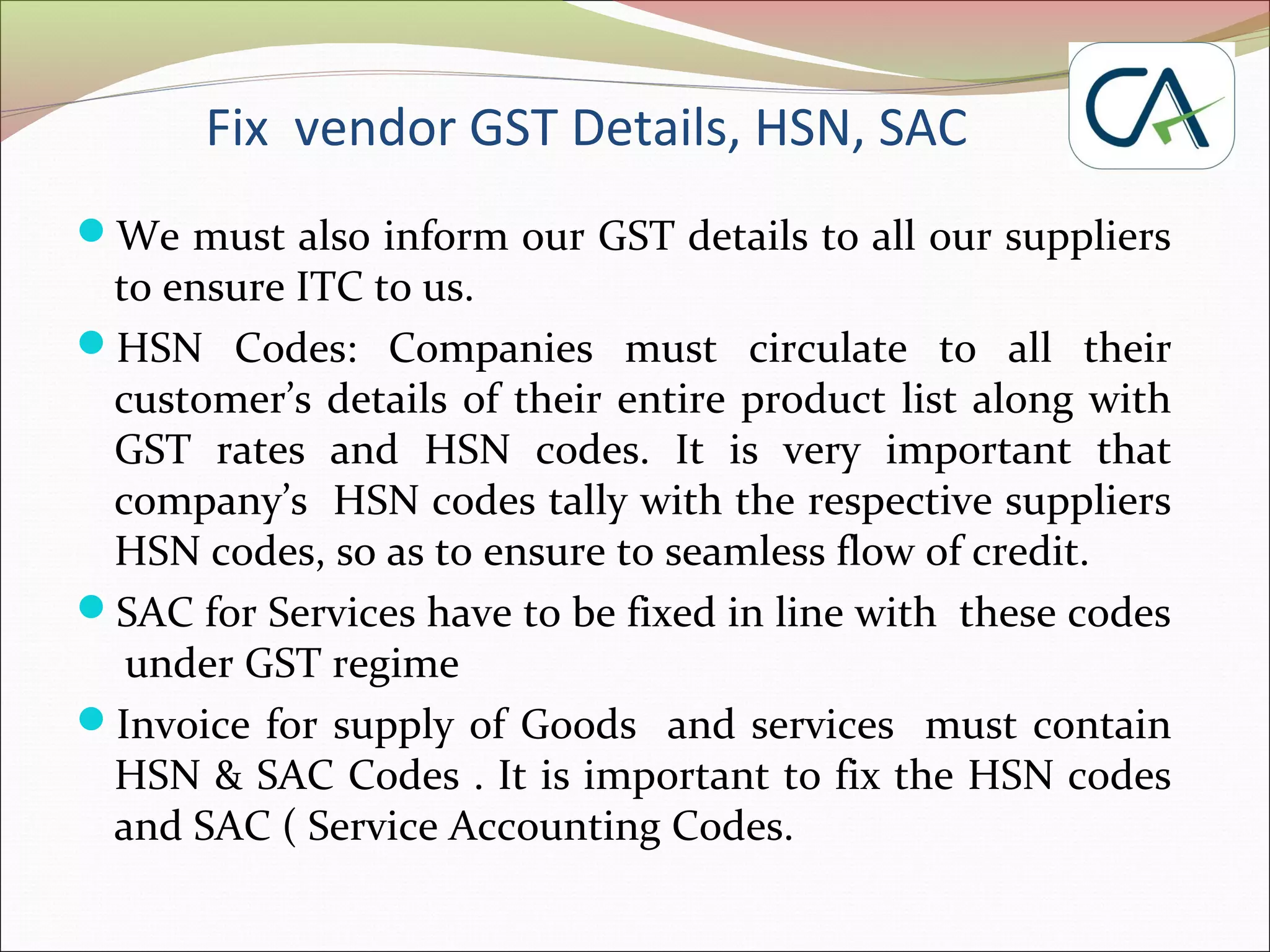

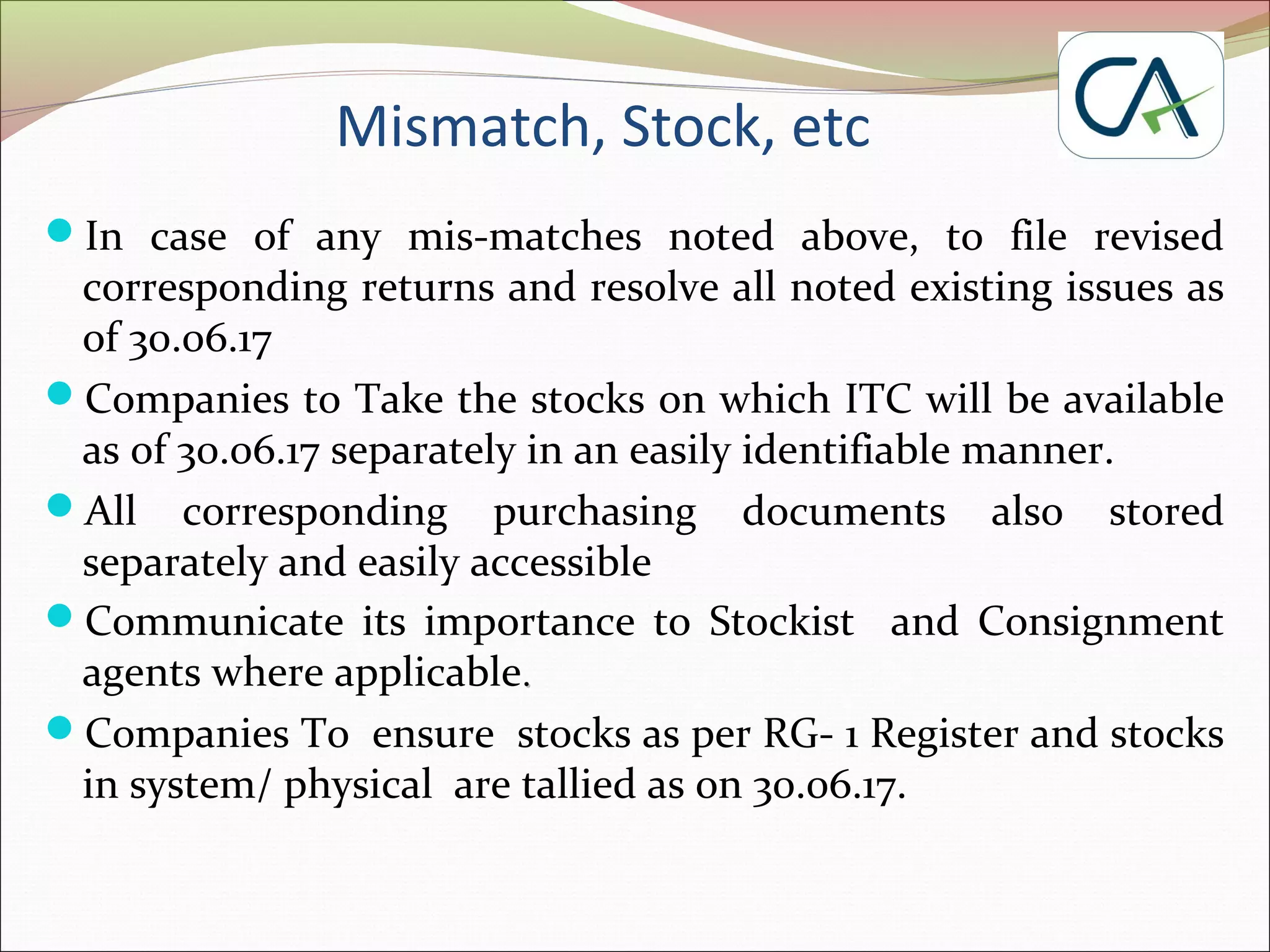

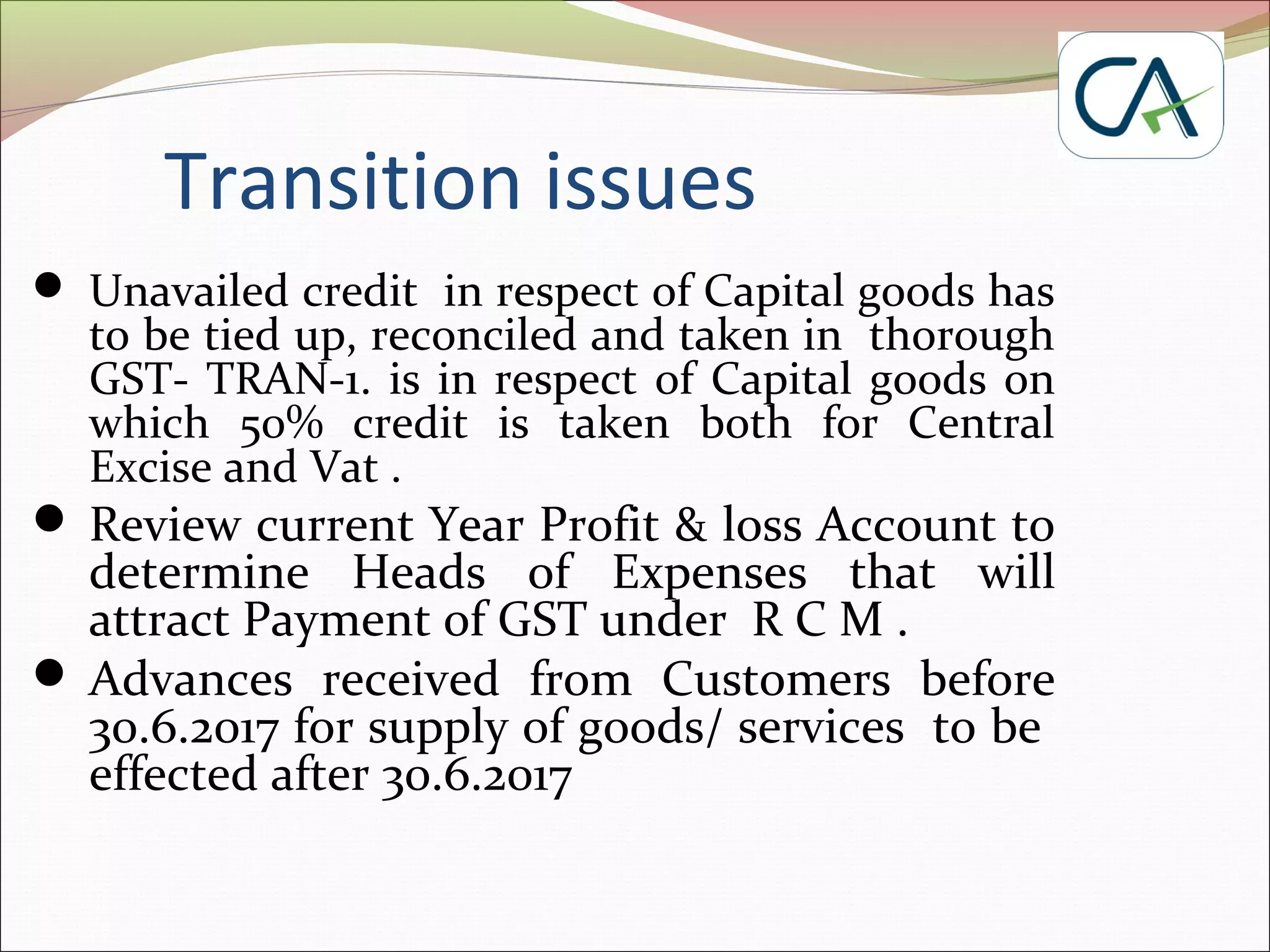

The document provides guidance on key actions companies need to take to prepare for GST implementation on July 1st, 2017. It outlines steps to obtain GST registration details from customers and suppliers to ensure seamless input tax credit flow. Companies must circulate product lists with HSN codes to customers and fix their own HSN and SAC codes. They are advised to close June 2017 sales by the 25th and ensure all stock is delivered by the 28th-29th to allow stockists to claim input tax credit. Companies should also reconcile any inventory or purchase mismatches by the 28th.