Pr 040310 Jan Stats Final

•

0 likes•312 views

ACI WORLD - January traffic shows strong start for the year - Global passenger traffic up by 6%; global freight up by 25% -

More Related Content

Similar to Pr 040310 Jan Stats Final

Similar to Pr 040310 Jan Stats Final (20)

More from Gianfranco Conti

More from Gianfranco Conti (20)

Recently uploaded

Recently uploaded (20)

Pr 040310 Jan Stats Final

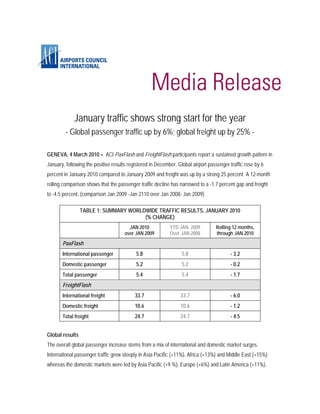

- 1. January traffic shows strong start for the year - Global passenger traffic up by 6%; global freight up by 25% - GENEVA, 4 March 2010 – ACI PaxFlash and FreightFlash participants report a sustained growth pattern in January, following the positive results registered in December. Global airport passenger traffic rose by 6 percent in January 2010 compared to January 2009 and freight was up by a strong 25 percent A 12-month rolling comparison shows that the passenger traffic decline has narrowed to a -1.7 percent gap and freight to -4.5 percent, (comparison Jan 2009 -Jan 2110 over Jan 2008- Jan 2009). TABLE 1: SUMMARY WORLDWIDE TRAFFIC RESULTS, JANUARY 2010 (% CHANGE) JAN 2010 YTD JAN 2009 Rolling 12 months, over JAN 2009 Over JAN 2008 through JAN 2010 PaxFlash International passenger 5.8 5.8 - 3.2 Domestic passenger 5.2 5.2 - 0.2 Total passenger 5.4 5.4 - 1.7 FreightFlash International freight 33.7 33.7 - 6.0 Domestic freight 10.6 10.6 - 1.2 Total freight 24.7 24.7 - 4.5 Global results The overall global passenger increase stems from a mix of international and domestic market surges. International passenger traffic grew steeply in Asia Pacific (+11%), Africa (+13%) and Middle East (+15%) whereas the domestic markets were led by Asia Pacific (+9 %), Europe (+6%) and Latin America (+11%).

- 2. Freight growth figures are even more impressive, with Asia Pacific and Middle East topping results respectively at +43 and +29 percent. Even keeping in mind that January 2009 showed the sharpest declines in freight traffic last year, January 2010 appears to be profiting from increasing stabilization of world production markets. Tonnage rose sharply at several key hubs: Abu Dhabi +26%, Bangkok +46%, Dubai +32%, Hong Kong +43%, Incheon +38%, Shanghai +82%, Sharjah +50%, Singapore +21%, Taipei +90%, Tel Aviv +18%, Tokyo Narita +45%. Regional comments Double-digit growth in Africa was reported by Abidjan, Cairo, Casablanca, Fez, Hurghada, Marrakech, Monastir, Oujda, Saint Denis and Sharm El Sheikh. Strong gains were made at several major Asia Pacific hubs (Bangkok, Beijing, Guangzhou, Incheon, Jakarta, Kuala Lumpur, Manila, Mumbai, Narita, New Delhi, Shanghai, Singapore, Sydney) but also at middle tier airports, notably in India and China. In Latin America, airports reported strong results – some international and some domestic – in Argentina (Buenos Aires +12%), Brazil (Brasilia +15%, Sao Paulo +22%), Ecuador (Guayaquil +10%, Quito +7%), and Peru (Lima +10%), whereas Mexico City and Cancun remained below 2009 levels. In Europe, international traffic rose by 3 percent and domestic by 6 percent, with mixed results for international traffic at the five largest competing hubs: Amsterdam +1%, Frankfurt +4%, London LHR +1%, Paris CDG +1 %, Madrid +9%. International traffic also rose in the second tier category: Brussels +2%, Copenhagen +4%, Istanbul +22%, Milan +9%, Munich +1%, Rome +15%, Vienna +4% and Zurich +6%. In the Middle East, international traffic was the driver for excellent results at almost all airports, including reports from Dubai where traffic rose by +17%, Abu Dhabi by +11% and Tel Aviv by +21%. North America’s international traffic was flat at +0.2%. Domestic traffic rose by 1.6 percent, with strongest growth seen by Boston +13%, Baltimore +9.1%, Chicago Midway +15%, Los Angeles +9%, New York LGA +5% and San Francisco +8%. Please note that for technical reasons Atlanta Hartsfield (ATL) airport has submitted preliminary figures only, but they indicate a 5 percent drop at the world’s busiest hub. See Tables 2 and 3 of this release for complete regional traffic results. 2

- 3. Notes for editors 1. ACI, the only worldwide association of airports, is a non-profit organisation whose prime purpose is to represent the interests of airports and to promote professional excellence in airport management and operations. ACI has 575 members who operate over 1630 airports in 179 countries and territories. 2. PaxFlash and FreightFlash statistics are based on a significant sample of airports that provide regular monthly reports to ACI. They represent approximately 60% of total passenger traffic and 70% of total freight traffic worldwide. Commentary, tables and charts are based on data submitted by participating airports. 3. Regional results and trend graphics are provided on the following pages. 4. For queries concerning the statistics, please contact Nancy Gautier, Director Communications, ACI World, Geneva Switzerland, email ngautier@aci.aero 3

- 4. TABLE 2: PaxFlash Summary – JANUARY 2010 YTD JAN YE JAN Regions JAN 2010 % YOY % YOY % YOY 2010 2010 International Passengers AFR 5 074 13.4 5 074 13.4 64 598 0.5 ASP 31 330 10.7 31 330 10.7 342 195 (0.4) EUR 52 521 2.9 52 521 2.9 807 235 (5.0) LAC 6 133 4.9 6 133 4.9 59 234 (6.9) MEA 7 286 15.3 7 286 15.3 84 188 8.3 NAM 13 142 (0.2) 13 142 (0.2) 161 218 (5.3) ACI TOTAL 115 485 5.8 115 485 5.8 1 518 668 (3.2) Domestic Passengers AFR 2 446 2.9 2 446 2.9 30 935 (5.5) ASP 45 129 8.6 45 129 8.6 544 649 7.3 EUR 19 204 5.8 19 204 5.8 273 497 (3.7) LAC 13 517 11.4 13 517 11.4 146 217 6.2 MEA NAM 60 823 1.6 60 823 1.6 827 216 (4.3) ACI TOTAL 141 118 5.2 141 118 5.2 1 822 514 (0.2) Total Passengers AFR 7 573 9.6 7 573 9.6 96 279 (1.6) ASP 77 594 9.3 77 594 9.3 899 692 4.2 EUR 72 093 3.6 72 093 3.6 1 084 843 (4.7) LAC 20 341 9.1 20 341 9.1 212 126 2.0 MEA 7 651 14.8 7 651 14.8 88 171 7.6 NAM 74 044 1.1 74 044 1.1 989 622 (4.7) TOTAL 259 296 5.4 259 296 5.4 3 370 733 (1.7) Traffic table definitions: PASSENGER TRAFFIC: departing + arriving passengers (000s) INTERNATIONAL: traffic performed between the designated airport and an airport in another country/territory DOMESTIC: traffic performed between two airports located in the same country/territory TOTAL: international + domestic passengers + direct transit passengers counted once (when breakdown is available) YOY Year over year same month comparison YTD Year to date, starting January 2009, compared to same period previous year YE Year end, based on rolling 12 month period, compared to same prior 12 month period AFR – Africa EUR – Europe MEA – Middle East ASP – Asia Pacific (including India) LAC – Latin America and Caribbean NAM – North America 4

- 5. Month by month comparison with same month previous year World passenger trends 8 International Domestic Total 6 4 2 0 % CHG -2 -4 -6 -8 -10 -12 -14 JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC JAN 2009 2010 Month by month comparison with same month previous year Total Passenger Trends By Region 25 AFR ASP EUR LAC MEA NAM 20 15 10 5 % CHG 0 -5 -10 -15 -20 JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC JAN 2009 2010 5

- 6. Month by month comparison with same month previous year International Passenger Trends by Region 25 20 AFR ASP EUR LAC MEA NAM 15 10 5 0 % CHG -5 -10 -15 -20 -25 -30 -35 JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC JAN 2009 2010 6

- 7. TABLE 3: FreightFlash Summary – JANUARY 2010 YTD JAN YE JAN Regions JAN 2010 % YOY % YOY % YOY 2010 2010 International Freight AFR 25.3 0.4 25.3 0.4 349.9 (16.0) ASP 1 537.2 46.6 1 537.2 46.6 17 495.9 (4.3) EUR 851.9 22.9 851.9 22.9 10 245.1 (8.4) LAC 134.3 26.1 134.3 26.1 1 577.7 (9.3) MEA 299.7 28.8 299.7 28.8 3 500.7 5.9 NAM 481.8 24.9 481.8 24.9 5 550.4 (11.4) ACI TOTAL 3 330.1 33.7 3 330.1 33.7 38 719.7 (6.0) Domestic Freight AFR 2.2 18.2 2.2 18.2 28.2 (5.6) ASP 547.1 34.7 547.1 34.7 6 201.7 10.8 EUR 32.0 (3.5) 32.0 (3.5) 449.5 (10.6) LAC 56.6 (7.0) 56.6 (7.0) 814.7 (10.1) MEA NAM 983.7 2.0 983.7 2.0 12 138.3 (5.5) ACI TOTAL 1 621.6 10.6 1 621.6 10.6 19 632.4 (1.2) Total Freight AFR 31.6 0.0 31.6 0.0 432.6 (14.3) ASP 2 084.3 43.3 2 084.3 43.3 23 700.6 (0.8) EUR 889.2 21.6 889.2 21.6 10 760.9 (8.5) LAC 190.9 14.1 190.9 14.1 2 392.8 (9.5) MEA 299.7 28.8 299.7 28.8 3 502.0 5.9 NAM 1 507.1 8.2 1 507.1 8.2 18 243.1 (7.5) ACI TOTAL 5 002.8 24.7 5 002.8 24.7 59 031.9 (4.5) Traffic table definitions: FREIGHT TRAFFIC: loaded and unloaded freight; data in metric tonnes INTERNATIONAL: traffic performed between the designated airport and an airport in another country/territory DOMESTIC: traffic performed between two airports located in the same country/territory TOTAL: international + domestic freight (when breakdown is available) Note: No domestic freight traffic is reported by airports in the Middle East region. The July responses for domestic freight in Africa were insufficient to determine growth percentages. YOY Year over year same month comparison YTD Year to date, starting January 2009, compared to same period previous year YE Year end, based on rolling 12 month period, compared to same prior 12 month period AFR – Africa EUR – Europe MEA – Middle East ASP – Asia Pacific (including India) LAC – Latin America and Caribbean NAM – North America 7

- 8. Month by month comparison with same month previous year World freight trends 40 International Domestic Total 30 20 10 % CHG 0 -10 -20 -30 JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC JAN 2009 2010 Month by month comparison with same month previous year Total Freight Regional Trends 50 40 AFR ASP EUR LAC MEA NAM 30 20 10 % CHG 0 -10 -20 -30 -40 JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC JAN 2009 2010 8

- 9. Month by month comparison with same month previous year International Freight Regional Trends 60 50 AFR ASP EUR LAC MEA NAM 40 30 20 % CHG 10 0 -10 -20 -30 -40 JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC JAN 2009 2010 - ENDS - 9