PPT GRAND PRESENTATION cbdc (central based digital currency)

1.

CURRENT SCENARIO ANDFUTURE

OF CENTRAL BANK DIGITAL

CURRENCIES

(GRAND PRESENTATION)

BY : AKSHITA JAIN

YASHIKA ARORA

ANURAG NAGI

SUMIT MATHUR

ISHIKA DHAMA

SHREYA SHAMBHAVI

2.

WHAT IS CENTRALBANK DIGITAL CURRENCY (CBDC)?

1. A Central Bank Digital Currency (CBDC) is the legal tender issued by a central

bank in a digital form. It is the same as a fiat currency and is exchangeable one-to-

one with the fiat currency. Only its form is different.

2.It is basically the virtual form of a fiat currency created and regulated by the

nation’s monetary authority or central bank (Reserve Bank of India).

3.It is a digital token or electronic record of a country’s official money.

4.It is sovereign currency in an electronic form and it would appear as liability

(currency in circulation) on a central bank’s balance sheet.

5. RBI started the process of designing CBDC framework in 2022. Finance Bill 2022

enacted with amendments in Reserve Bank of India Act, 1934 for CBDC.

3.

CURRENT SCENARIO OFOTHER CURRENCY

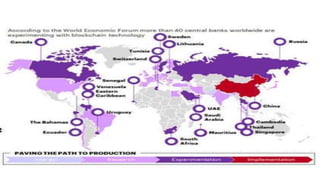

• 81 countries , representing over 90 percent of Global GDP, are

exploring CBDCs.

• Fourteen countries have tested pilots.

• China(e-Yuan) and south Korea, England , Sweden(e-Krona).

• 16 countries such currencies are in the development phase.

• 32 countries in the research phase-USA , UK , Mexico etc.

• The Bahamas , Nigeria and 7 countries in Eastern Caribbean

Union- have already launched a centrally governed digital.

4.

AIM OF CBDC’S

1.Theaim of study of CBDC’s is to study how

mitigate the risks and trim costs in handling

physical currency, costs of phasing out

soiled notes, transportation, insurance and

logistics.

2.t will also wean people away from

cryptocurrencies as a means for money

transfer.

5.

OBJECTIVES OF CBDCs

1.Exchangingenhancing financial inclusion control.

2. Ensuring the stability of the financial system.

3. Improving the efficiency of payment system.

4. Providing a safe , and efficient means of payment ,accessible to all citizens ,

reducing reliance on physical cash and potentially lowering transaction costs.

5. Seen as a way to fortify the economy against the challenges posed by private

digital currencies and to maintain control over monetary policy.

6. The main objective is to mitigate the risks and trim costs in handling physical

currency, costs of phasing out soiled notes, transportation, insurance and

logistics.

7.It will also wean people away from cryptocurrencies as a means for money

transfer.

6.

FIAT MONEY

• Itis a government-issued currency that is not backed by a

commodity such as gold.

• It gives central banks greater control over the economy

because they can control how much money is printed.

• Most modern paper currencies such as the US dollar are fiat

currencies.

• One danger of fiat money is that governments will print too

much of it, resulting in hyperinflation.

INTERNATIONAL MONETARY FUND(IMF)STATEMENT

1.The IMF’s Digital Money Strategy , endorsed by its Executive Board in July 2021, gives

the institution a mandate to help that digital money fosters domestic and international

economic and financial stability.

2.CBDC’s , in particular , will likely have important implications for monetary policy, financial

stability, and the international monetary system (IMS).

3.The IMF must monitor ,and advise on , digital money developments for members.

4.Given its mandate and global membership , the IMF is uniquely well-placed to offer advice

to countries across different regions and income groups.

5.Over 40 countries have approached the IMF to request assistance through CBDC capacity

development(CD).

CROSS BORDER TRANSACTION

•CBDCs possess unique attributes that can revolutionize

cross-border transactions.

• Instant settlement feature of CBDCs as a significant

advantage, making cross-border payments cheaper,

faster, and more secure.

• Faster, cheaper, transparent, and inclusive cross-border

payment services can yield substantial benefits for

individuals and economies worldwide.

• These improvements can support economic growth,

international trade, and financial inclusion on a global

scale.

11.

FINANCIAL INCLUSION

• Theincreased use of CBDC could be explored for many other

financial activities to push the informal economy into the formal

zone to ensure better tax and regulatory compliance.

• It can also pave the way for furthering financial inclusion.

TRADITIONAL AND INNOVATION

• CBDC can gradually bring a cultural shift towards virtual

currency by reducing currency handling costs.

• CBDC is envisaged to bring in the best of both worlds:

• The convenience and security of digital forms like

cryptocurrencies.

• The regulated, reserved-backed money circulation of the

traditional banking system.

12.

What are theChallenges in Adopting CBDC Across India?

● The first issue to tackle is the heightened risk to the privacy of

users—given that the central bank could potentially end up

handling an enormous amount of data regarding user

transactions.

● This has serious implications given that digital currencies will

not offer users the level of privacy and anonymity offered by

transacting in cash.

● Compromise of credentials is another major issue.

1. PRIVACY CONCERN :

13.

2. DISINTERMEDIATION OFBANKS :

• If sufficiently large and broad-based, the shift to CBDC can impinge

upon the bank’s ability to plough back funds into credit intermediation.

• If e-cash becomes popular and the Reserve Bank of India (RBI) places

no limit on the amount that can be stored in mobile wallets, weaker

banks may struggle to retain low-cost deposits.

3. OTHER RISKS ARE :

• Faster obsolescence of technology could pose a threat to the CBDC

ecosystem calling for higher costs of upgradation.

• Operational risks of intermediaries as the staff will have to be retrained

and groomed to work in the CBDC environment.

• Elevated cyber security risks, vulnerability testing and the costs of

protecting the firewalls.

• Operational burden and costs for the central bank in managing CBDC.

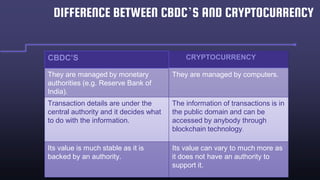

CBDC’S CRYPTOCURRENCY

They aremanaged by monetary

authorities (e.g. Reserve Bank of

India).

They are managed by computers.

Transaction details are under the

central authority and it decides what

to do with the information.

The information of transactions is in

the public domain and can be

accessed by anybody through

blockchain technology.

Its value is much stable as it is

backed by an authority.

Its value can vary to much more as

it does not have an authority to

support it.

DIFFERENCE BETWEEN CBDC’S AND CRYPTOCURRENCY

16.

ADVANTAGES OF CBDC’S

•It aims at reduction in operational costs involved in physical cash

management, fostering financial inclusion, bringing resilience,

efficiency and innovation in the payments system.

• It will add efficiency to the settlement system and boost innovation in

cross-border payments space.

• It will provide the public with the uses that any private virtual

currencies can provide without any associated risks.

• It will curb issues such as money laundering, terror financing,

• tax evasion , etc.

17.

BRICS Will CreatePayment System Based on Digital

Currencies and Blockchain

• The BRICS grouping will create a payment system based on blockchain.

• The effort is part of a specific task for this year to increase the role of BRICS in the international

monetary system.

• The five-nation BRICS group comprising Brazil, Russia, India, China and South Africa will work

on creating a payment system based on blockchain and digital technologies, a report by Russian

news agency TASS said.

• “We believe that creating an independent BRICS payment system is an important goal for the

future, which would be based on state-of-the-art tools such as digital technologies and

blockchain.

• The main thing is to make sure it is convenient for governments, common people and

businesses, as well as cost-effective and free of politics,” Kremlin aide Yury Ushakov said in an

interview with TASS.

• The effort is part of a specific task for this year to increase the role of BRICS in the international

monetary system.

• For some time now, the BRICS grouping has been making efforts to reduce its reliance on U.S.

dollars in settlement, also known as de-dollarization..

18.

BRICS Will CreatePayment System Based on Digital

Currencies and Blockchain

• Work will continue to develop the Contingent Reserve Arrangement,

primarily regarding the use of currencies different from the US dollar,"

Ushakov said.

• Last week, another TASS report said Russia’s Finance Ministry, the Bank

of Russia and BRICS partners will create the BRICS Bridge multisided

payment platform in an effort to improve the global monetary system.

• Also in February, Klaas Knot, the Chair of the Financial Stability Board,

which keeps an eye on the global financial system, wrote to finance

ministers from the Group of 20 (G20) countries that crypto assets,

tokenization and artificial intelligence (AI) remain priorities.

19.

DISADVANTAGES OF CBDC’S

•It does not decentralize the economy as

the central bank controls data of

transactions between the banks and their

consumers.

• The privacy of users was compromised to

some extent.

• Legal and regulatory issues act like

limitations.

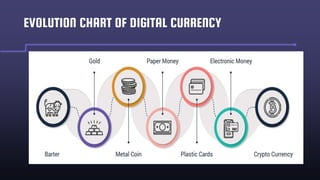

CBDCs represent adigital form of a country's national currency, in the case of India, it is Digital Rupee

(e₹), issued and regulated by the central bank. It is fundamentally different from cryptocurrencies like

Bitcoin, which are decentralized and operate outside the traditional financial system. CBDCs, on the other

hand, are fully integrated into the central bank's monetary policy and payment infrastructure . Digital

currency refers to any currency that is available in electronic form. The Digital Rupee is virtual money,

serving the same purpose as physical money. It is a form of digital currency issued by the Reserve Bank

of India (RBI), the country's central bank. The Digital Rupee is a centralized digital currency directly

regulated by the RBI, maintaining the stability and trust associated with traditional currencies . The Digital

Rupee is introduced in India to enhance financial inclusion, providing greater access to formal financial

services. It aims to promote efficiency in transactions through faster and more secure digital payment

methods, align with the country's technological advancements, foster a digital-first economy, reduce

dependence on physical currency, and enable better regulatory control over monetary transactions while

countering potential illicit activities . Digital Rupee, also known as e Rupee , is electronic money. It

operates as a form of digital currency issued and controlled by the Reserve Bank of India (RBI), using

blockchain or distributed ledger technology for secure and transparent transactions .Types of CBDC’s.

CBDCs can be broadly categorized into two main types : Retail CBDCs: Designed for use by the general

public for everyday transactions, similar to how cash is used today . Wholesale CBDCs: Intended for use

by financial institutions for interbank settlements and other wholesale transactions . Issuing Digital Rupee.

CASE STUDY

22.

The Reserve Bankof India (RBI) issues electronic tokens that can be exchanged on a one-to-one basis, with

denominations similar to physical currency. The RBI controls the distribution of the Digital Rupee, distributing

it to commercial banks or authorized financial institutions for circulation. Transactions made with Digital

Rupee are recorded and verified on a secure ledger system for transparency and security . Acquiring Digital

Rupee Users can acquire Digital Rupee through digital wallets provided by authorized financial institutions or

other approved platforms. These wallets function as secure digital storage for the currency. Digital tokens

can also be withdrawn, similar to withdrawing cash, and cash can be converted to e Rupee using a UPI

gateway . Users can load the required token amount or select different denominations of Digital Rupee

through their linked Banked Account (Bank of Baroda Account) or Other UPI Account. If users have chosen

"Other UPI Account," a list of all UPI apps available on their phone will appear. Users can select their

preferred UPI app, enter their UPI PIN, and complete the transaction. The amount is debited from the Bank

Account directly, and Digital Rupee is loaded in the wallet successfully . Users can redeem/unload wallet

tokens to their linked bank account. Digital Rupee Tokens will be unloaded from their wallet, and the

equivalent amount will be credited to their linked bank account . Using Digital Rupee . Person-to-Person:

Transfer money to another person’s wallet with a QR code or their mobile number. Person-to-Merchant:

Scan the QR code displayed at a merchant’s establishments (shops) to make a payment . Features of Digital

Rupee .The Digital Rupee is issued by the Reserve Bank of India and is legally recognized as a secure form

of payment accepted by individuals, businesses, and governmental bodies . Issuance follows the central

bank's financial policies . Holders have the freedom to convert Digital Rupee into physical cash through

commercial banks . Legal Tender: CBDCs are considered legal tender, usable for all types of transactions .

Central Bank Control: CBDCs are controlled and regulated by the central bank, ensuring stability and

trustworthiness . Programmable Money: CBDCs can have programmable features, such as smart contracts,

enabling automated, self-executing financial agreements .

23.

Advantages of DigitalRupee . Financia l Inclusion: Provides opportunities for those without access to traditional banking

services, allowing participation in the formal economy . Reduced Transaction Costs: Eliminates intermediaries, leading

to lower transaction costs compared to traditional banking systems . Efficiency and Speed: Transactions are processed

faster, often within seconds, regardless of geographical locations . Transparency and Security: Blockchain ledger

ensures transaction transparency while maintaining security through cryptographic protocols . Government Control and

Regulation: Being centrally regulated, the RBI can control the supply, circulation, and monetary policies associated with

Digital Rupee . Challenges and Concerns of CBDC Privacy Concerns: The use of CBDCs raises questions about privacy, as

transactions can be easily monitored and traced, potentially compromising individual financial privacy . Cybersecurity

Risks: CBDCs are susceptible to cyber-attacks, requiring robust security measures to protect the digital currency's

integrity . Disruption of Traditional Banking: Widespread adoption of CBDCs could disrupt traditional banking systems,

potentially leading to bank runs and other systemic challenges . International Implications: Global adoption of CBDCs

may influence the international monetary system, raising concerns about the role of the U.S. dollar as the world's

primary reserve currency . CBDC in Bank of Baroda Milestones . Bank of Baroda Launched CBDC application called

“Bank of Baroda Digital Rupee” on 17th January 2023.Bank of Baroda enabled CBDC UPI QR Interoperability

functionality for pilot users on the Bank of Baroda Digital Rupee app on September 2, 2023. Conclusion . The Digital

Rupee holds the potential to revolutionize India's financial landscape, promoting financial inclusion, reducing

transaction costs, and streamlining financial operations. As the digital currency ecosystem evolves, the Digital Rupee is

positioned to play a pivotal role in shaping the future of transactions and financial services in India . The Digital Rupee is

a landmark development in India's financial history, leveraging technology to create a more inclusive and efficient

financial system.

24.

QUESTIONS OF ELEARNING MODULE

1. With reference to Central Bank digital currencies, consider the

following statements :

1.It is possible to make payments in a digital currency without using

US dollar or SWIFT system.

2.A digital currency can be distributed with condition programmed

into it such as a time-frame for spending it.

Which of the statements given above is/are correct?

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Ans: (c)

25.

QUESTIONS OF ELEARNING MODULE

2.With reference to “Blockchain Technology”, consider the following

statements:

1.It is a public ledger that everyone can inspect, but which no single user

controls.

2.The structure and design of blockchain is such that all the data in it are

about cryptocurrency only.

3.Applications that depend on basic features of blockchain can be developed

without anybody’s permission.

Which of the statements given above is/are correct?

(a) 1 only

(b) 1 and 2 only

(c) 2 only

(d) 1 and 3 only

Ans: (d)

26.

QUESTIONS OF ELEARNING MODULE

3. Which one of the following statements is incorrect with respect to

Central Bank Digital Currency?

1.Digital Rupee is considered as a legal tender in India.

2.Wholesale CBDC is restricted for access to select financial

institutions only.

3.In a token-based CBDC, the person receiving a token will verify that

his ownership of the token is genuine.

4.None of the above

Answer: 4

27.

QUESTIONS OF ELEARNING MODULE

4. Which technology was used in CBDC’S?

1. Block Chain

2. Distribution Ledger Technology

3. Server

Ans: 1

28.

• The CBDChas many advantages to

offer like reduced cost, and better

central control over the paper

currency.

• The present banking system needs

to be part of the CBDC Pilot

projects in the Indian context.

• The acceptance and anonymity of

paper currency can be attained

with CBDC only with time and

gradual acceptance.

CONCLUSION