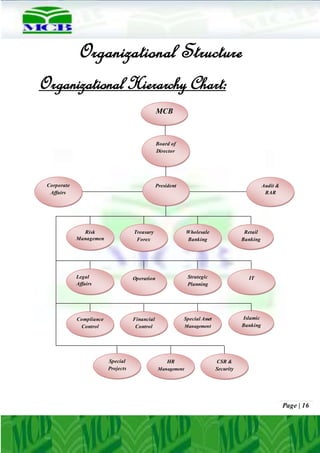

The document provides an overview of MCB Bank including its history, objectives, core values, management, products, clients and competitors. MCB was established in 1947 and was later nationalized and privatized, and it now has over 1,190 branches in Pakistan and abroad offering various banking services and products to retail and corporate customers. The management profiles and organizational structure are also outlined.