Downloaded 54 times

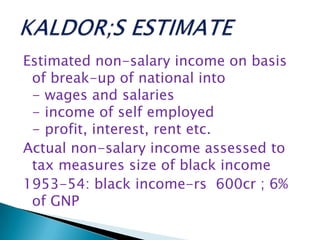

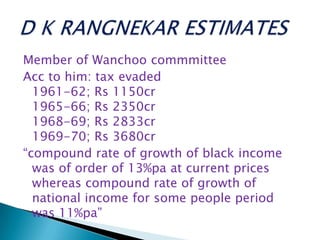

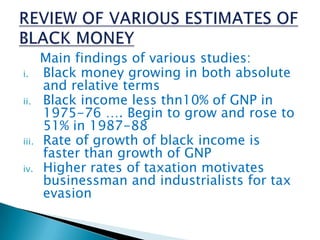

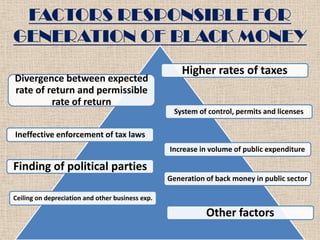

This document summarizes several studies on the parallel economy and black money in India from the 1950s to 1980s. Key findings include: - Estimates of black money as a percentage of GNP increased from under 10% in the 1970s to over 50% by the late 1980s, indicating black money was growing faster than the overall economy. - Different studies using variations of the Kaldor method produced generally consistent estimates of increasing black money over time, though actual amounts varied between studies. - Higher tax rates, controls on business activities, and ineffective tax enforcement were cited as primary drivers of black money generation. - Growth of black money was seen as distorting the economy and tax base with

![5G Explained! A High Level Overview [Introduction]](https://cdn.slidesharecdn.com/ss_thumbnails/5gexplainedahighleveloverview-260119165306-cc137a3e-thumbnail.jpg?width=640&height=640&fit=bounds)