Downloaded 17 times

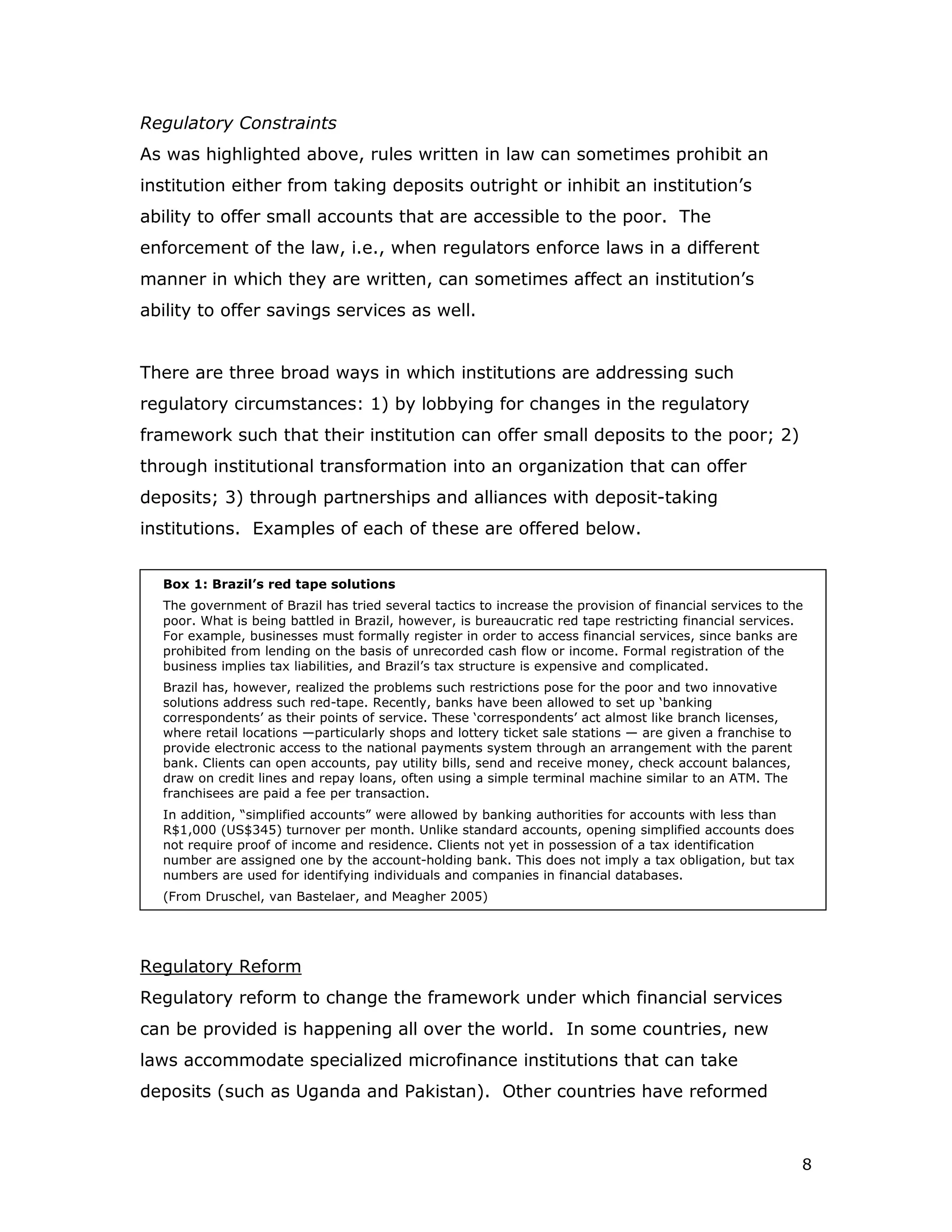

Regulatory constraints often limit microfinance institutions' ability to provide savings services. This document discusses three ways these constraints are being overcome: 1) Lobbying for changes to regulations to allow savings; 2) Transforming institutions into organizations allowed to take deposits; 3) Partnering with deposit-taking institutions. Examples from Brazil show allowing correspondents to provide banking services and simplified no-documentation accounts to expand access. Many countries are reforming regulations to develop microfinance-friendly frameworks.

![3[1]](https://cdn.slidesharecdn.com/ss_thumbnails/31-130204001051-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Podcasting Legal Guide[1]](https://cdn.slidesharecdn.com/ss_thumbnails/podcastinglegalguide1-1231408004989385-1-thumbnail.jpg?width=640&height=640&fit=bounds)