Bobby Katoli and Jonathan Startz are members of the management team at MassCatalyst. Their contact information is provided should readers wish to reach out to them.

Page | 2

CROWDFUNDING& JOBS ACT

Definition

Crowdsourcing is the collection of ideas, services, and content from a large group of people. Crowdfunding is an extension of this

concept focusing on the aggregate collection of capital with modern crowdfunding heavily relying on the connectivity of the

Internet. Crowdfunding leverages the Internet to take small amounts of money from multiple funders, pool them together, and give

an aggregate large sum of money to a project, concept, or business.

JOBS Act

The passage of the JOBS Act on April 5, 2012 made it legal for entrepreneurs to solve the obstacle of funding by selling equity to a

large number of investors online via the power of the Internet. The two main titles under the JOBS Act that pertain to MassCatalyst

are Title II and Title III. Title III is expected to be in full effect by the end of the year.

Targets accredited investors

No individual investment limit

No funding limit (i.e. businesses may ask to

receive an unlimited amount of money)

Title II Title III

Targets non-accredited (“ordinary”) investors

Individual investment limit based on

income

Businesses are limited to $1.0 million of

funding every 12 months.

Platform Structure

MassCatalyst will be structured to help all businesses receive funding regardless of investment limit (i.e. the platform will be legally

structured to fund businesses that need more than $1.0 million under Title II and fund businesses that need less than $1.0 million

under Title III).

3.

Page | 3

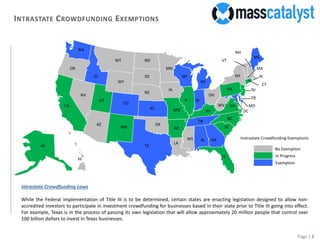

INTRASTATECROWDFUNDING EXEMPTIONS

Intrastate Crowdfunding Laws

While the Federal implementation of Title III is to be determined, certain states are enacting legislation designed to allow non-

accredited investors to participate in investment crowdfunding for businesses based in their state prior to Title III going into effect.

For example, Texas is in the process of passing its own legislation that will allow approximately 20 million people that control over

100 billion dollars to invest in Texas businesses.

In Progress

No Exemption

Instrastate Crowdfunding Exemptions

TX

NM

AZ

NV

UT

CA

OR

WA

MT

ID

WY

CO

ND

SD

NE

KS

OK

LA

AR

MO

IA

MN

MS

WI

MI

IL

AL GA

FL

SC

TN

NC

KY

VA

IN

OH

PA

WV

AK

HI

ME

NY

VT

NH

MA

RI

CT

NJ

DE

MD

DC

Exemption

4.

Page | 4

MASSCATALYST’SPLATFORM

Current Crowdfunding Models

MassCatalyst Model

MassCatalyst is the only investment crowdfunding platform in the United States that combines equity & lending business models

into an auction-based system. An auction platform gives businesses the opportunity to raise funding for less equity and better

investment terms. Other investment platforms do not allow for negotiations between investors who must accept the investment

terms as is or walk away from the deal altogether. MassCatalyst solves this problem by creating an auction system that inherently

creates a “negotiation” among potential investors. In turn, this creates a true marketplace for private placement investing.

Furthermore, MassCatalyst will implement a secondary market to create liquidity in otherwise illiquid investments.

Crowdfunding Models Source: “Crowdfunding’s Potential for the Developing World” published by the World Bank

Crowdfunding

Model

Business Model Features Pros Cons

Donation Donation based Philanthropic: funders donate without

expecting monetary compensation.

No risk. Donors do not acquire security interest. Entrepreneurs have

difficulty raising substantial capital.

Reward based Funders receive a token gift of

appreciation or pre-purchase of a service

or product.

Low risk (primarily fulfillment and

fraud risk). No real potential for

financial return.

Potential return is small. No security is acquired, and there

is no accountability mechanism. Most entrepreneurs may

have difficulty raising substantial capital without a product

with mass appeal to sell.

Investing Equity based Funders receive equity instruments or

profit sharing arrangements.

Potential to share in the

profitability of the venture.

Unlimited potential for financial

gain.

Potential loss of investment. Equity holder are subordinate

to creditors in the event of bankruptcy. Securities laws

related to crowdfund investing may be complex.

Lending based Funders receive a debt instrument that

pays a fixed rate of interest and returns

principal on a specified schedule.

Pre-determined rate of return

agreed upon between the lender

and borrower. Debt holder are

senior to equity holder in case of

bankruptcy.

May be subordinate to senior creditors. Start-ups high

failure rate presents similar risk of loss as an equity

investment, but with capped potential returns. Requires a

business already generating cash flow.

5.

Page | 5

DIFFERENTIATORS

Problem

Crowdfundingis striving to solve the funding gap for startups and businesses in early growth phases. By leveraging the JOBS Act,

crowdfunding is democratizing the investment process by allowing non-accredited investors to invest in business startups. However,

most crowdfunding platforms are very rigid and do not allow for negotiation between investors and businesses. The investors either

accept the terms of the offer set by the business or walk away from the deal altogether. This model does not consider the potential

market forces of supply and demand. To this extent, current investment crowdfunding in this country is failing to truly leverage the

Internet and the JOBS Act to positively benefit businesses and ordinary investors.

Auction Model

Combine equity & debt models (e.g.

auction convertible debt)

Secondary market to create liquidity in an

illiquid investment

Solution Benefit

Businesses can get overfunded for less

equity; early investing is incentivized

Access to a diverse range of financial

products

Investors may have an exit opportunity in

the secondary market

Overall Benefit

Creates a true marketplace to facilitate the flow of capital from investors to entrepreneurs. An auction system creates an inherent

“negotiation” between investors and businesses through the bidding process. Investors bid the value they believe shares in the

business are worth and if their value is high enough they receive equity ownership. Effectively, if bidding is high enough, the business

is issuing the same or less equity for more money than compared to traditional crowdfunding. In addition, a secondary market will

create liquidity and a potential exit opportunity for existing investors. MassCatalyst’s business model provides an effective solution

for the age-old problem of raising capital for a business, in a manner that is superior to all other current competitors.

6.

Page | 6

BENEFITSFOR INVESTORS

Benefits

Our platform wants to privately raise money before the auction goes live.

Auction Model

Combine equity & debt models (e.g.

auction convertible debt)

Secondary market to create liquidity in an

illiquid investment

Solution Benefit

Businesses can get overfunded for less

equity; early investing is incentivized

Access to a diverse range of financial

products

Investors may have an exit opportunity in

the secondary market

Overall Benefit

Creates a true marketplace to facilitate the flow of capital from investors to entrepreneurs. An auction system creates an inherent

“negotiation” between investors and businesses through the bidding process. Investors bid the value they believe shares in the

business are worth and if their value is high enough they receive equity ownership. Effectively, if bidding is high enough, the business

is issuing the same or less equity for more money than compared to traditional crowdfunding. In addition, a secondary market will

create liquidity and a potential exit opportunity for existing investors. MassCatalyst’s business model provides an effective solution

for the age-old problem of raising capital for a business, in a manner that is superior to all other current competitors.

7.

Page | 7

EQUITYAUCTION WALKTHROUGH

Auction vs. Traditional Crowdfunding

Traditional Crowdfunding

Funding Goal: $50,000

Shares Issued: 50,000

Price Per Share: $1.00

Final Price: $1.00

Equity Offered: 50%

Amount Funded: $50,000

Outcome:

The company can only raise $50,000 at

$1.00 per share. If the company were to

raise additional capital they must issue

additional shares which effectively

raises the amount of equity offered

above 50%.

Auction Crowdfunding Scenario 1

Funding Goal: $50,000

Shares Issued: 50,000

Price Per Share: $1.00

Winning Bid: $1.50

Equity Offered: 50%

Amount Funded: $75,000

Outcome:

The company has issued all of their

shares for $1.50 to raise a total amount

of $75,000. The company has already

raised more money for the same 50%

equity as compared to the same

scenario in traditional crowdfunding.

Auction Crowdfunding Scenario 2

Funding Goal: $50,000

Shares Issued: 33,333

Price Per Share: $1.00

Winning Bid: $1.50

Equity Offered: 33%

Amount Funded: $50,000

Outcome:

In a final bid of $1.50, the company may

be fully funded by only issuing 33% of

the equity for $50,000. The remaining

17% equity is returned to the business.

In effect, the company raised $50,000

by issuing less equity.

8.

Page | 8

EQUITYAUCTION WALKTHROUGH (CONTINUED)

Bidding Process

Investors bid on the price per share, and ultimately, the highest per share bids win the auction.

Investor A:

Investor Amount Invested: Bid:

Investor B:

Investor C:

$25,000

$25,000

$30,000

$2.00

$1.71

$1.50

Auction Information

Funding Goal: $50,000

Shares Issued: 50,000

Price Per Share: $1.00

Equity Offered: 50%

Winning Bid: $1.50

Amount Funded: $75,000

Shares Received:

10,000

23,333

16,667

Investor D: $30,000 $1.40 20,000

Bidding Process

The winning bidders are Investors A, B, & C because these investors were the highest bidders for the 50,000 shares issued by the

company. The total number of shares received by Investors A, B, & C are equal to the 50,000 shares the company offered. All

winning investors will pay the lowest winning price of $1.50. The lowest winning price means that since Investor C was the last

investor to win the auction and only paid $1.50, then it is only fair that all other winning investors pay the same amount of $1.50. In

this example, the company was able to raise $75,000 for the same 50% equity offering while initially seeking only $50,000.

Winning Price:

$1.50

$1.50

$1.50

9.

Page | 9

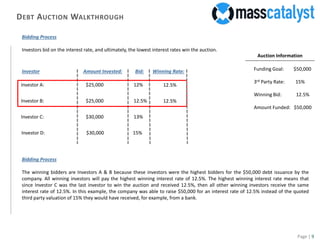

DEBTAUCTION WALKTHROUGH

Bidding Process

Investors bid on the interest rate, and ultimately, the lowest interest rates win the auction.

Investor A:

Investor Amount Invested: Bid:

Investor B:

Investor C:

$25,000

$25,000

$30,000

12%

12.5%

13%

Auction Information

Funding Goal: $50,000

3rd Party Rate: 15%

Winning Bid: 12.5%

Amount Funded: $50,000

Investor D: $30,000 15%

Bidding Process

The winning bidders are Investors A & B because these investors were the highest bidders for the $50,000 debt issuance by the

company. All winning investors will pay the highest winning interest rate of 12.5%. The highest winning interest rate means that

since Investor C was the last investor to win the auction and received 12.5%, then all other winning investors receive the same

interest rate of 12.5%. In this example, the company was able to raise $50,000 for an interest rate of 12.5% instead of the quoted

third party valuation of 15% they would have received, for example, from a bank.

Winning Rate:

12.5%

12.5%

10.

Page | 10

CONTACTUS

Management Team

Our executive team brings smart, stable, and trusted guidance to MassCatalyst. With experience ranging from wealth management

and hedge funds to healthcare and valuation, our management team brings the talent, vision, and knowledge necessary to ensure

MassCatalyst provides unparalleled value for our clients.

Bobby Katoli

Email: Bobbykatoli@masscatalyst.com

Direct: 817-308-4319

Office: 469-730-6026

Jonathan Startz

Email: Jonathanstartz@masscatalyst.com

Direct: 281-687-5112

Office: 469-730-6026

![Crowdfunding and it’s benefit for funding real estate 1 [autosaved]](https://cdn.slidesharecdn.com/ss_thumbnails/crowdfundinganditsbenefitforfundingrealestate1autosaved-170627144304-thumbnail.jpg?width=640&height=640&fit=bounds)