New lending caps to demolish unsecured lending industry in poland in 2017

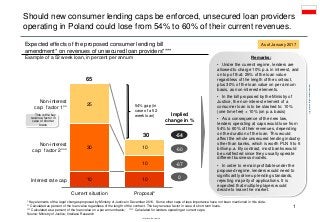

Unsecured lending providers in Poland prepare for a major regulatory overhaul in 2017. • Under the current regime, lenders operatin in Poland are allowed to charge 10% p.a. in interest, and on top of that: 25% of the loan value regardless of the length of the contract, plus 30% of the loan value on per annum basis, as non-interest elements. • In the bill proposed by the Ministry of Justice in Dec. 2016, the non-interest element of a consumer loan is to be slashed to: 10% (one time fee) + 10% (on p.a. basis) • As a consequence of the new law, lenders operating at caps would lose nearly 54% of their revenues. This would affect the whole unsecured lending industry other than banks, which is worth PLN 5 to 6 billion p.a. By contrast, most banks would be unaffected since they operate different business models. • In order to remain profitable under the proposed regime, lenders would need to significantly drive up lending standards, rejecting majority of applications. It is expected that multiple players would decide to leave the market.

Recommended

Recommended

More Related Content

Viewers also liked

More from Inteliace Research

More from Inteliace Research (12)

Recently uploaded

Recently uploaded (20)

New lending caps to demolish unsecured lending industry in poland in 2017

- 1. Inteliace Research UnsecuredconsumerlendinginPoland,2017 Should new consumer lending caps be enforced, unsecured loan providers operating in Poland could lose from 54% to 60% of their current revenues. 1 10 10 30 10 25 10 Current situation Proposal* Remarks: • Under the current regime, lenders are allowed to charge 10% p.a. in interest, and on top of that: 25% of the loan value regardless of the length of the contract, plus 30% of the loan value on per annum basis, as non-interest elements. • In the bill proposed by the Ministry of Justice, the non-interest element of a consumer loan is to be slashed to: 10% (one time fee) + 10% (on p.a. basis) • As a consequence of the new law, lenders operating at caps would lose from 54% to 60% of their revenues, depending on the duration of the loan. This would affect the whole unsecured lending industry other than banks, which is worth PLN 5 to 6 billion p.a. By contrast, most banks would be unaffected since they usually operate different business models. • In order to remain profitable under the proposed regime, lenders would need to significantly drive up lending standards, rejecting majority of applications. It is expected that multiple players would decide to leave the market. -54 Implied change in % -60 -67 0 30 65 * Key elements of the legal changes proposed by Ministry of Justice in December 2016. Some other caps of less importance have not been mentioned in this slide. ** Calculated as percent of the loan value regardless of the length of the contract. The key revenue factor in case of short term loans. *** Calculated as a percent of the loan value on a per annum basis; **** Calculated for lenders operating at current caps. Source: Ministry of Justice, Inteliace Research Expected effects of the proposed consumer lending bill amendment* on revenues of unsecured loan providers**** Example of a 52 week loan, in percent per annum Interest rate cap Non-interest cap: factor 2*** As of January 2017 54% gap (in case of a 52 week loan) Non-interest cap: factor 1** This is the key revenue factor in case of shorter loans