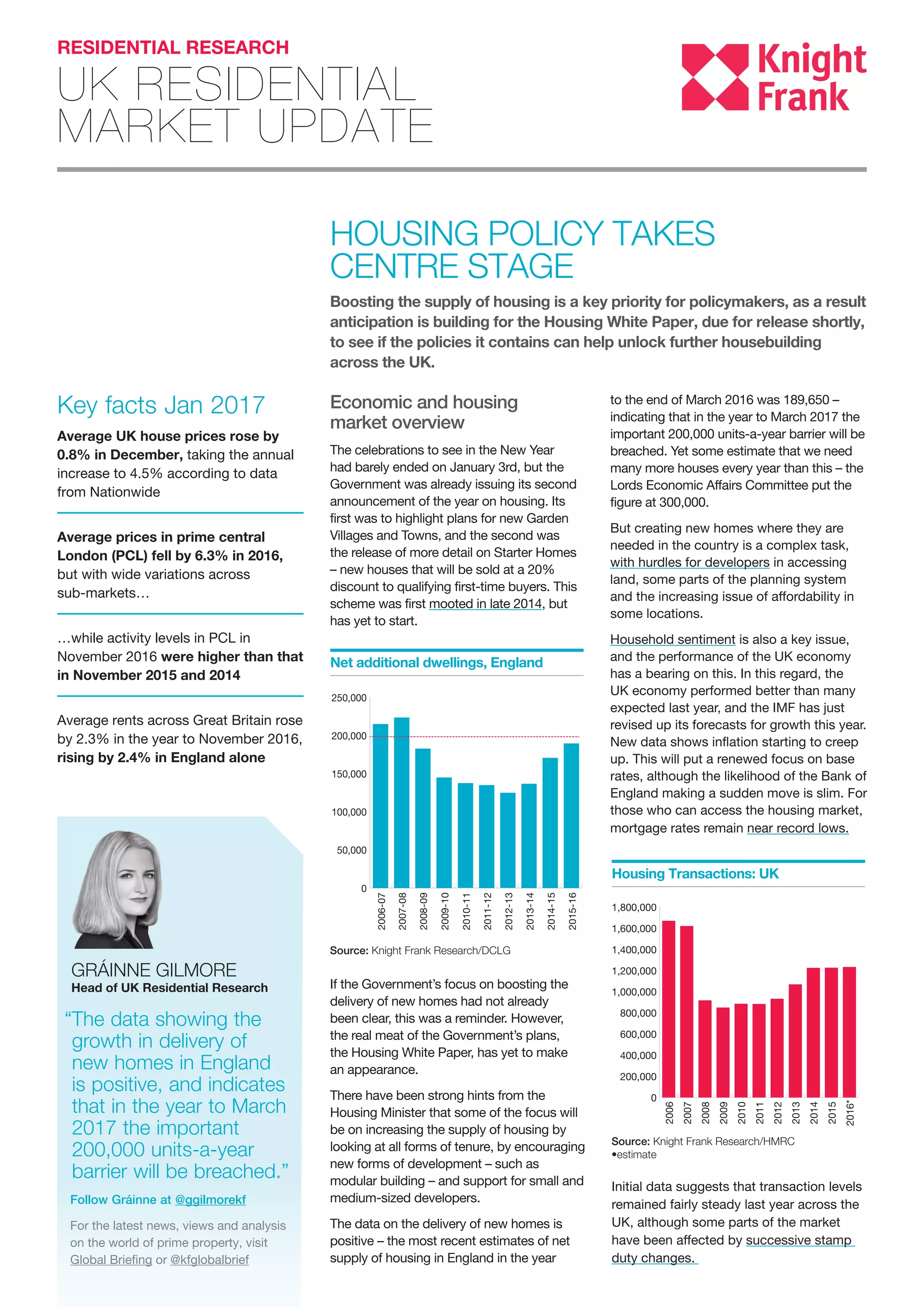

The document provides an economic and housing market overview from the UK. It discusses several recent announcements from the UK government around plans to boost housing, including new Garden Villages and Towns and a scheme to offer discounts to first-time buyers. Data shows that delivery of new homes in England is on track to surpass 200,000 units for the year, an important target. However, some estimates say more new homes are needed each year. The housing white paper is expected to outline further plans to increase supply.