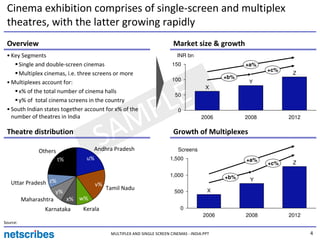

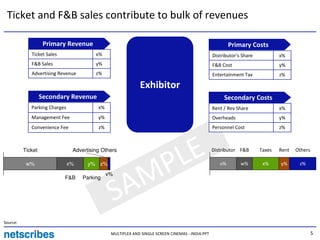

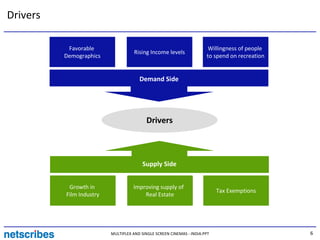

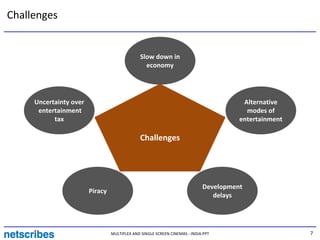

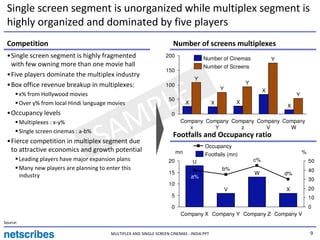

The document analyzes the cinema exhibition market in India, which comprises single screen and multiplex theaters. It estimates the market was worth INR XX billion in 2008 and is projected to reach INR YY billion in 2012. While the multiplex segment is growing, the single screen segment is declining. The multiplex segment is dominated by five major players and accounts for a growing share of screens and revenues. Key drivers of growth include rising incomes and willingness to spend on entertainment, while challenges include uncertainty over taxes and the rise of alternative entertainment options.

![Film4[1]](https://cdn.slidesharecdn.com/ss_thumbnails/film41-090329153540-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)