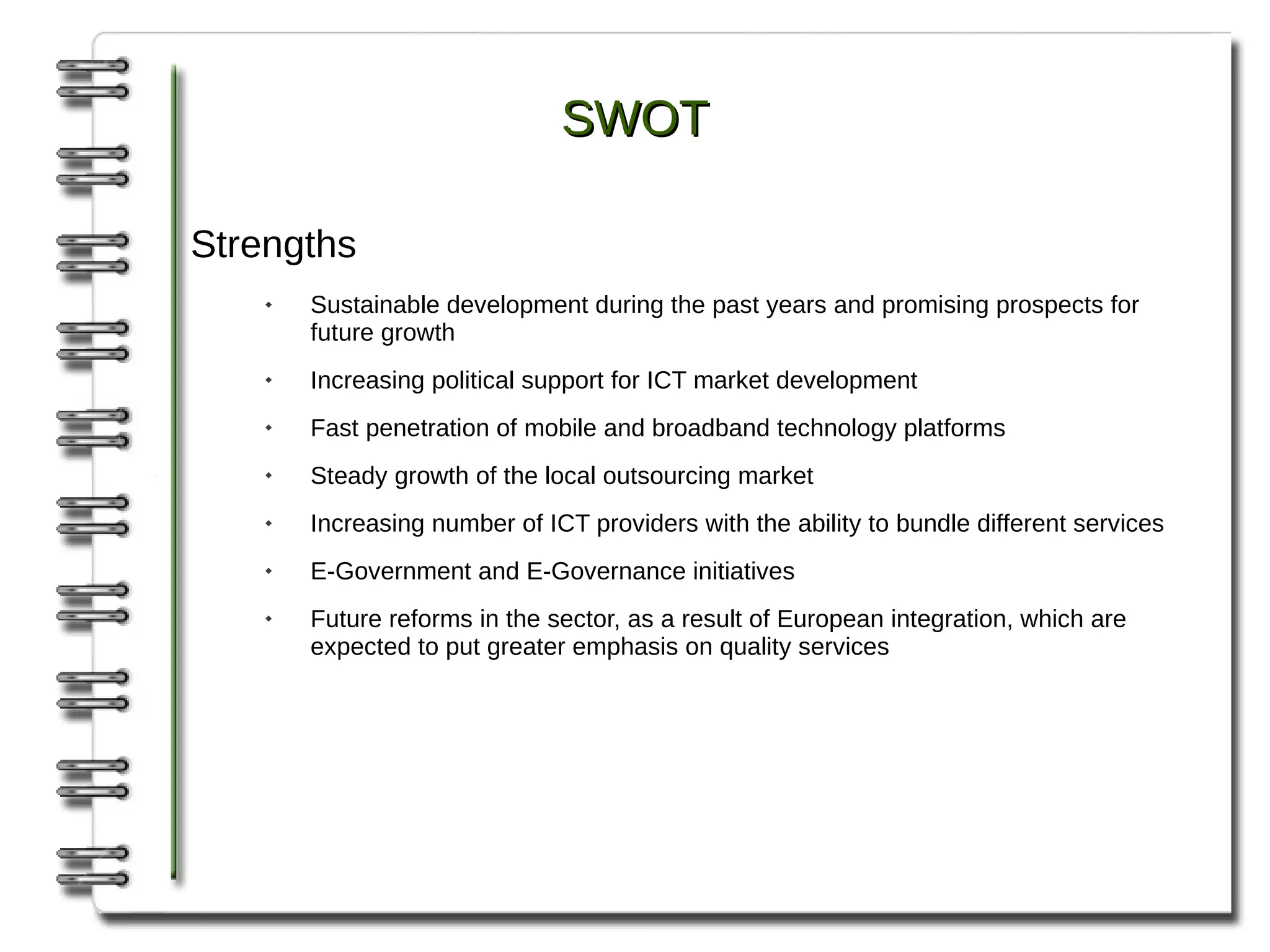

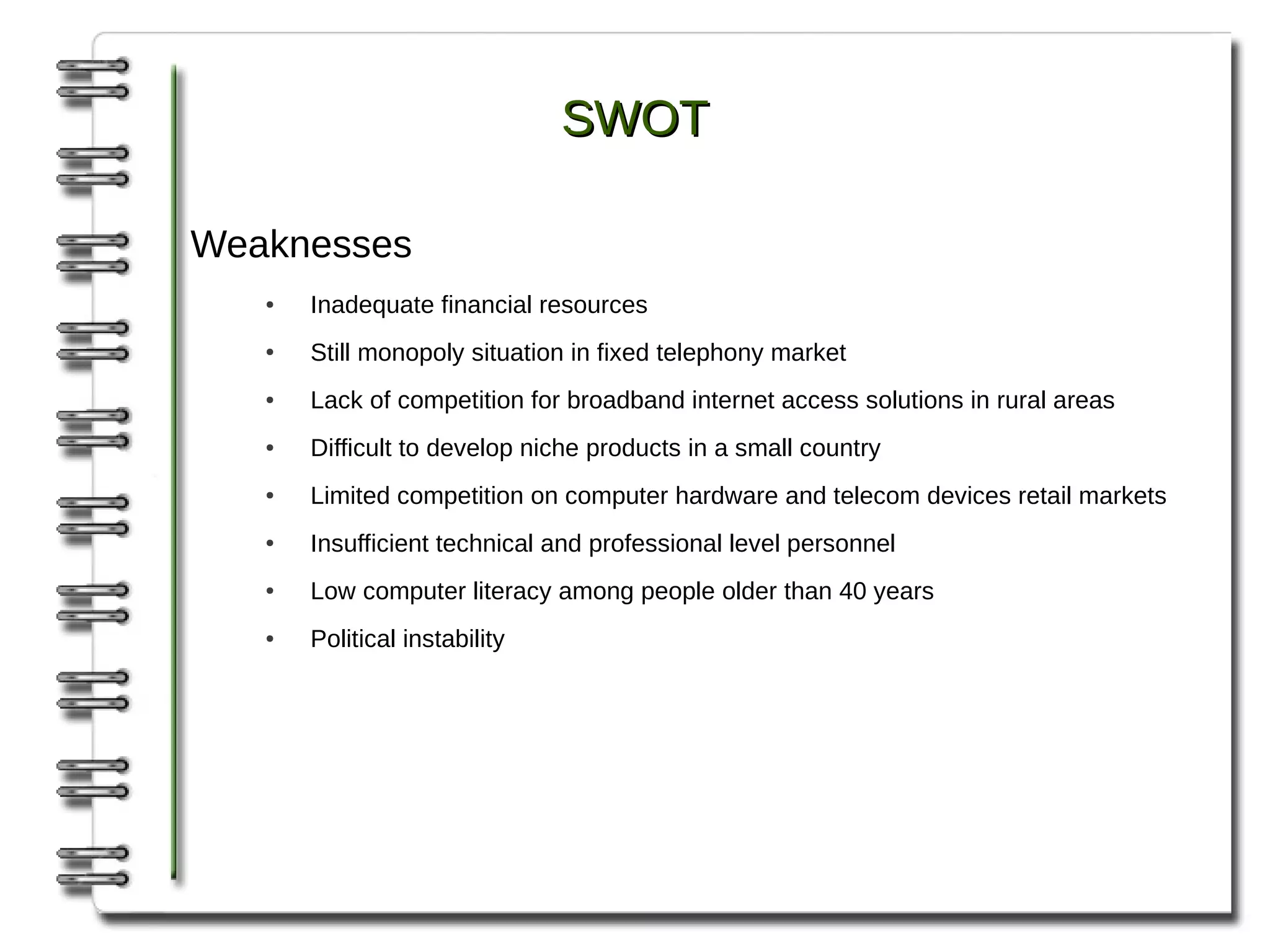

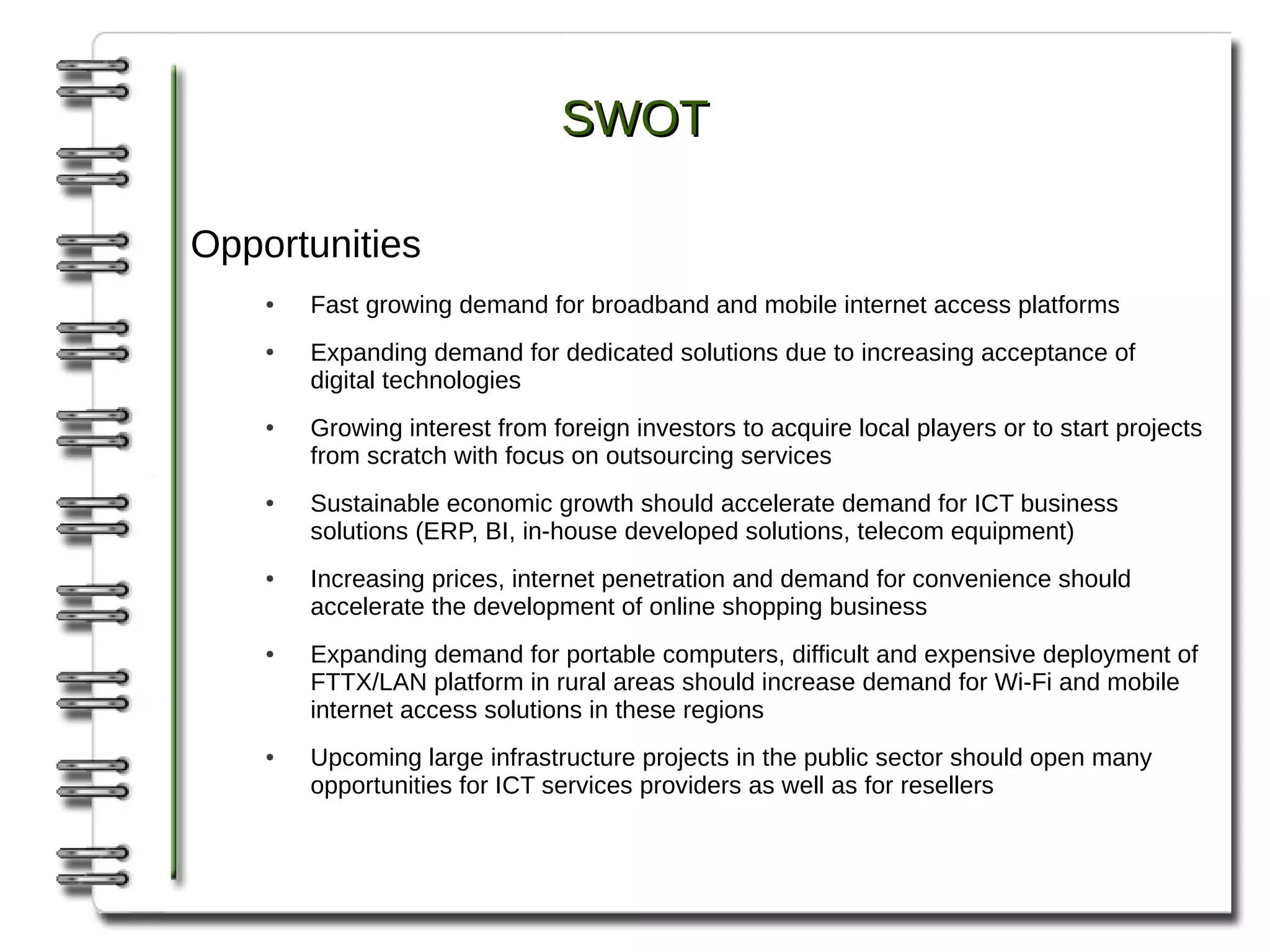

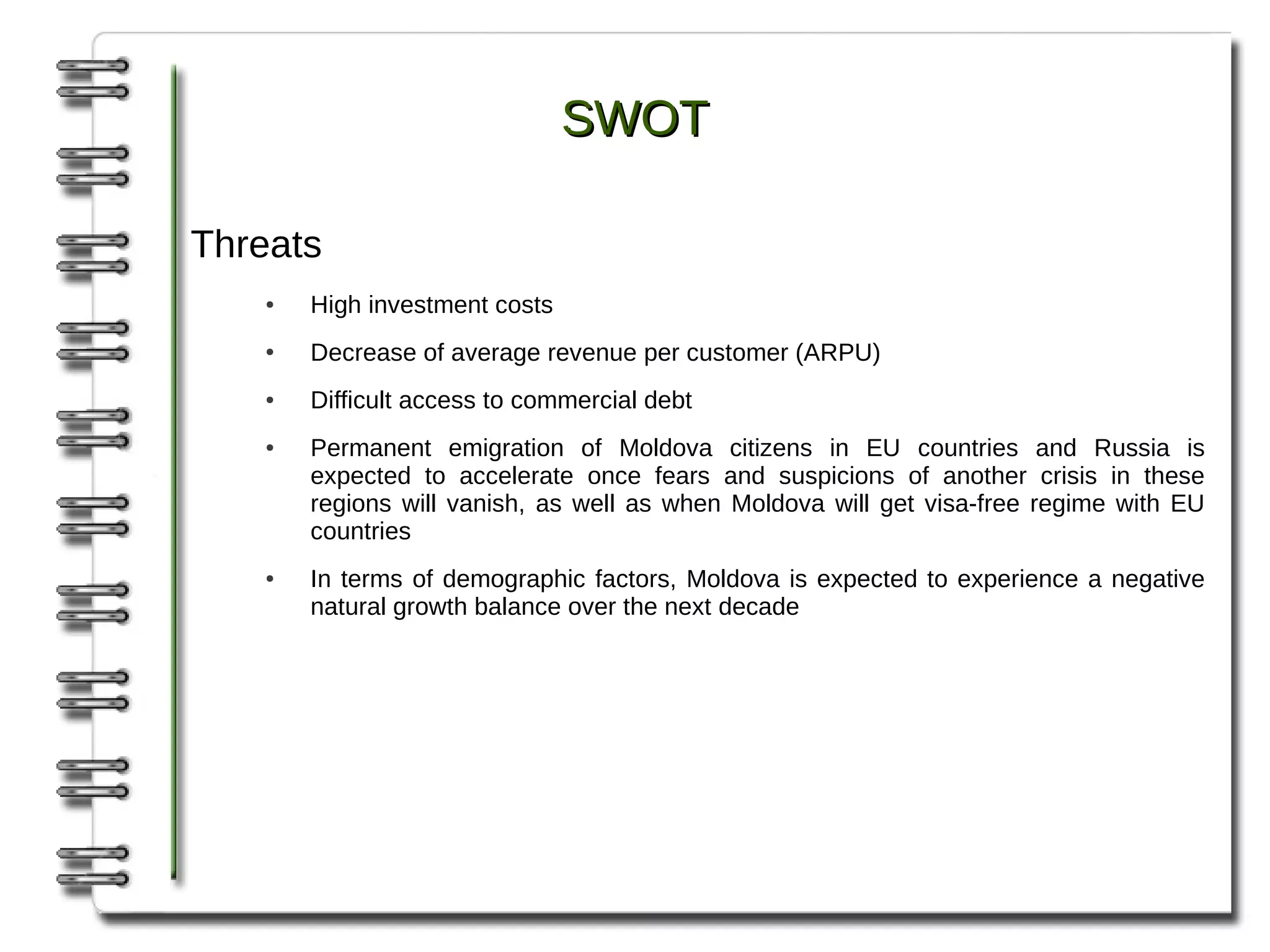

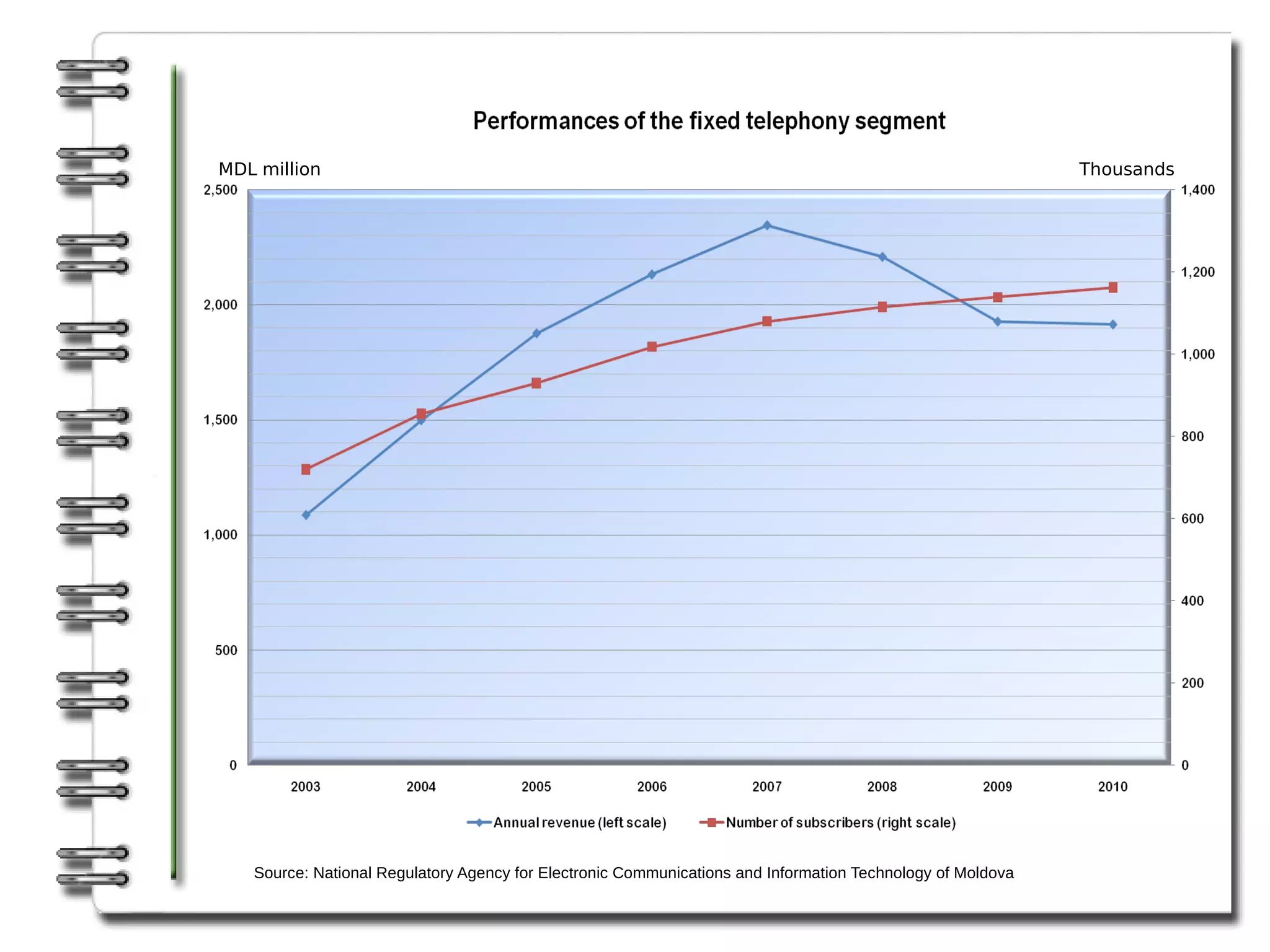

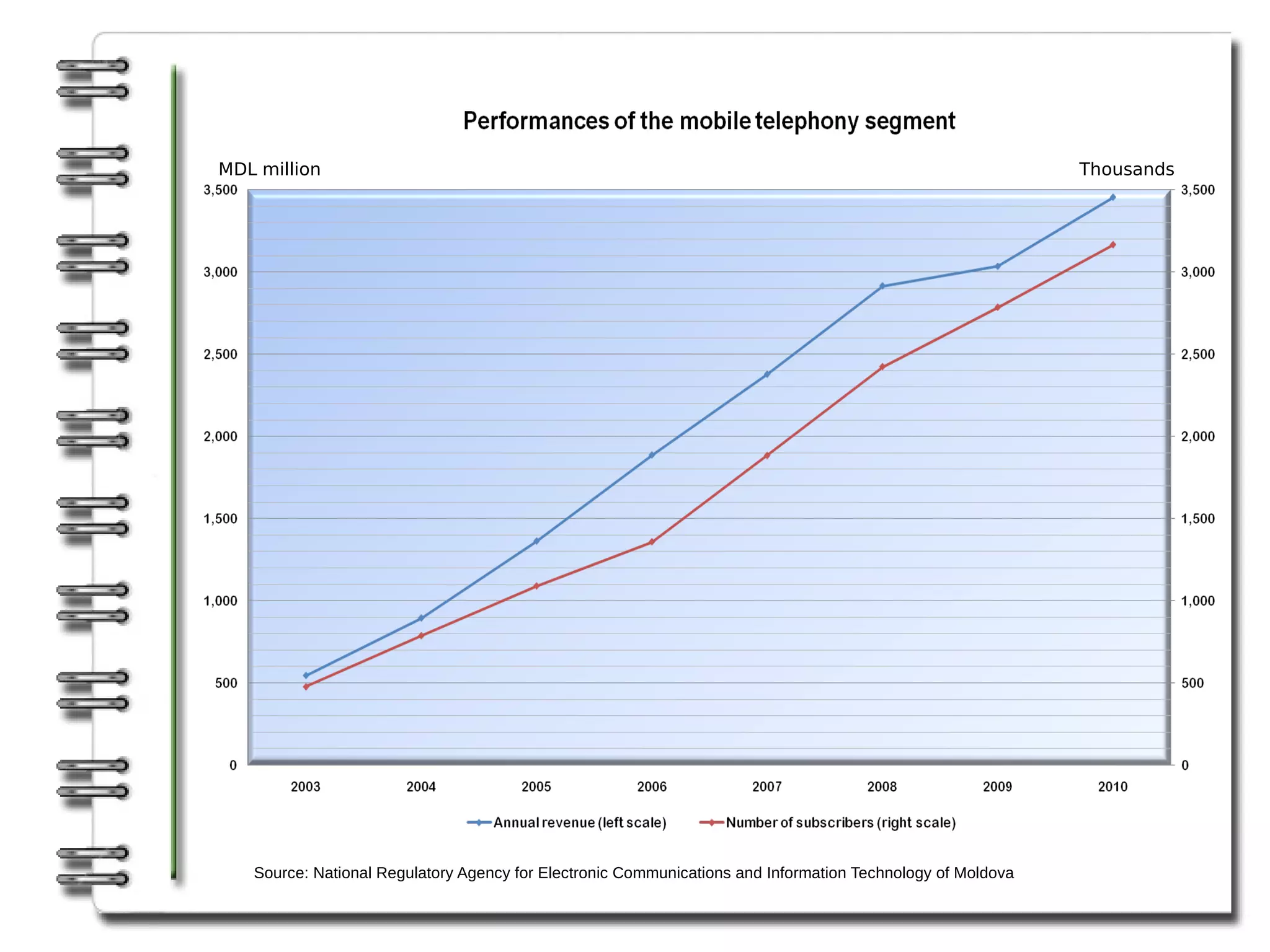

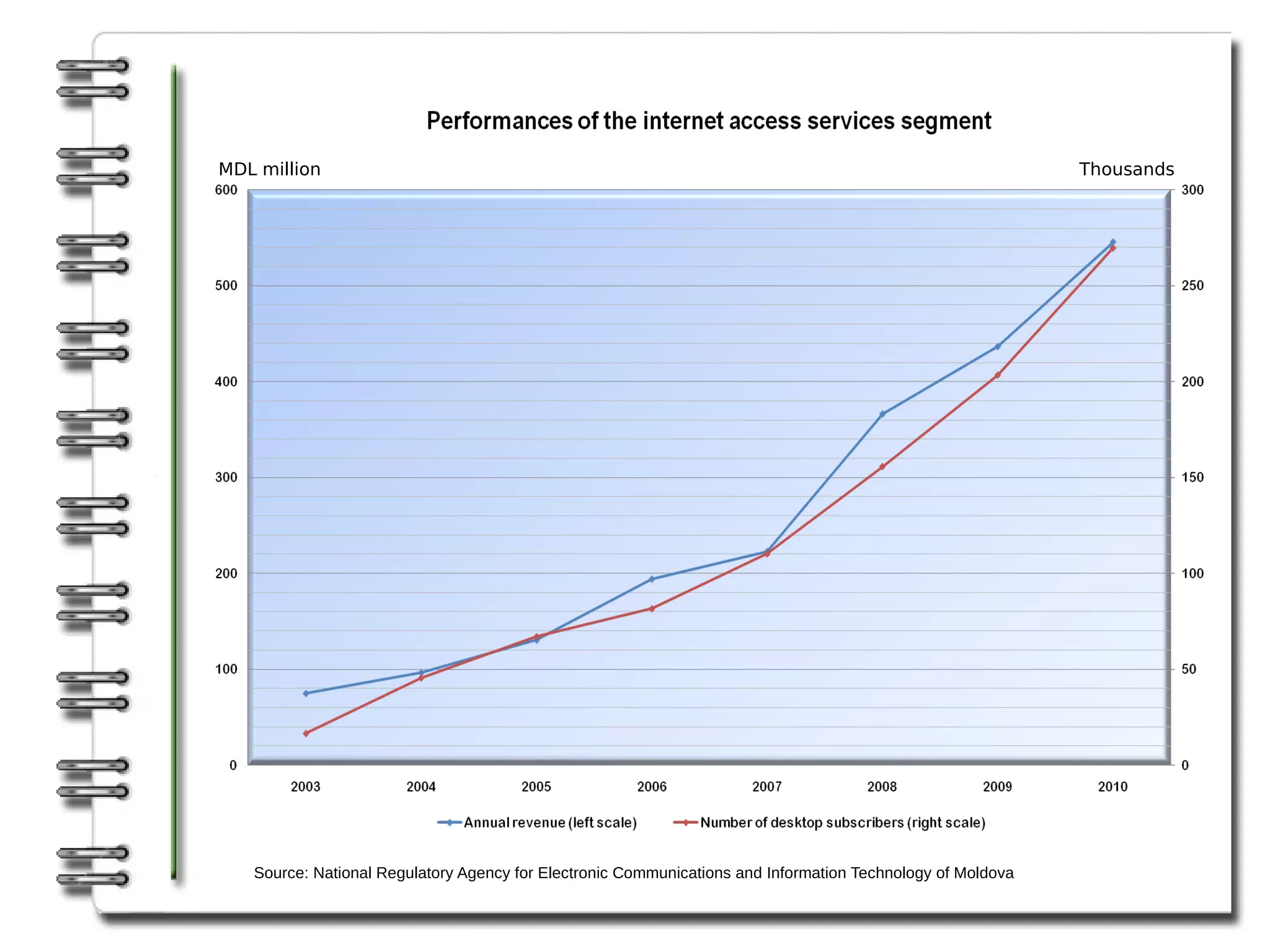

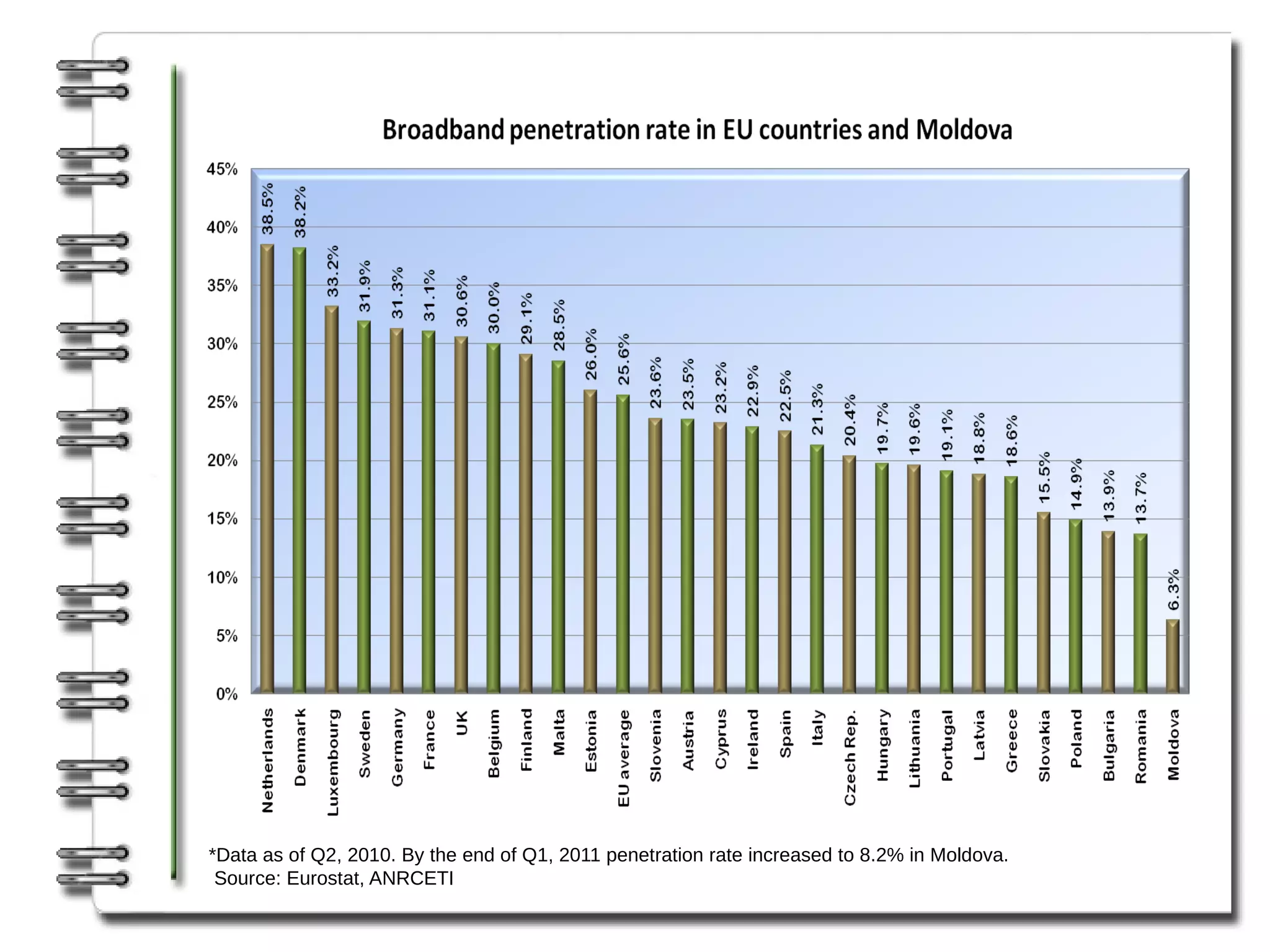

The telecommunication sector in Moldova has seen strong growth over the last decade. Mobile telephony has been the main driver of growth, while fixed telephony remains dominated by the incumbent provider Moldtelecom. Internet access services have also grown rapidly, with broadband penetration increasing significantly. Looking ahead, mobile and broadband services are expected to continue their expansion, while fixed telephony declines. New technologies like 3G and 4G may see limited adoption. Competition in broadband access outside of cities remains a challenge due to infrastructure costs. Overall the market remains promising but barriers like high investment needs, population migration, and monopoly control in some areas could hamper further development.