Download to read offline

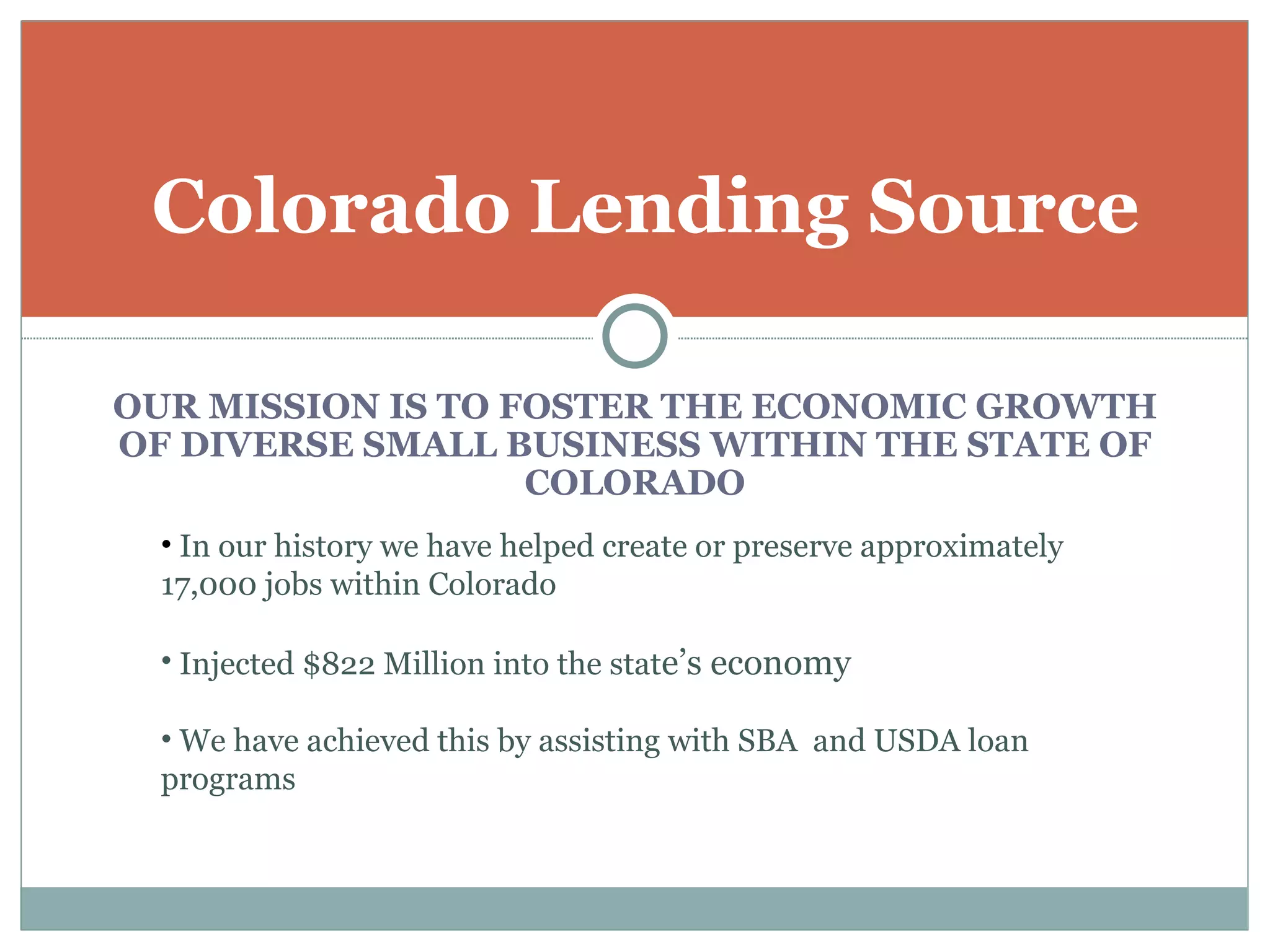

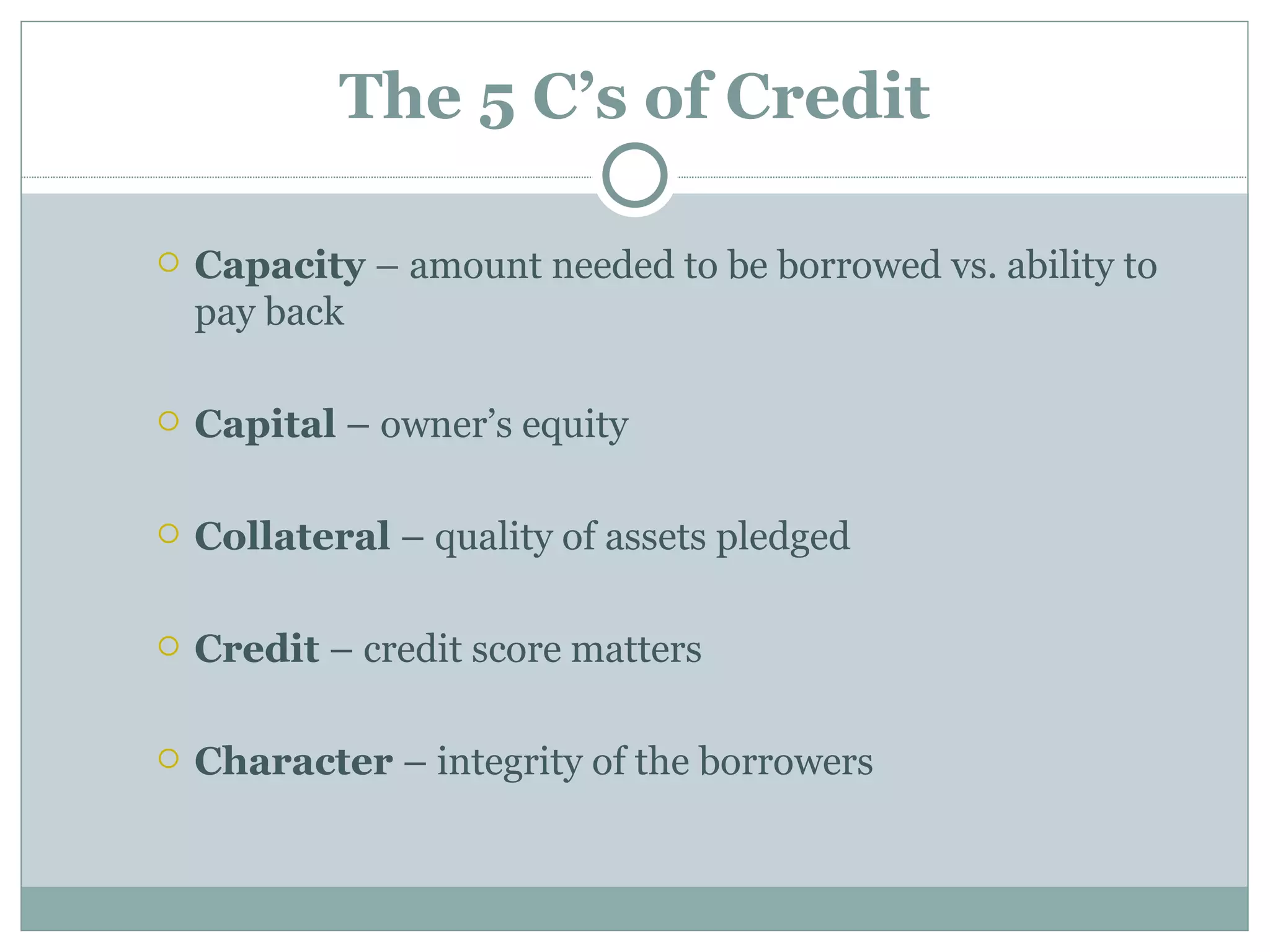

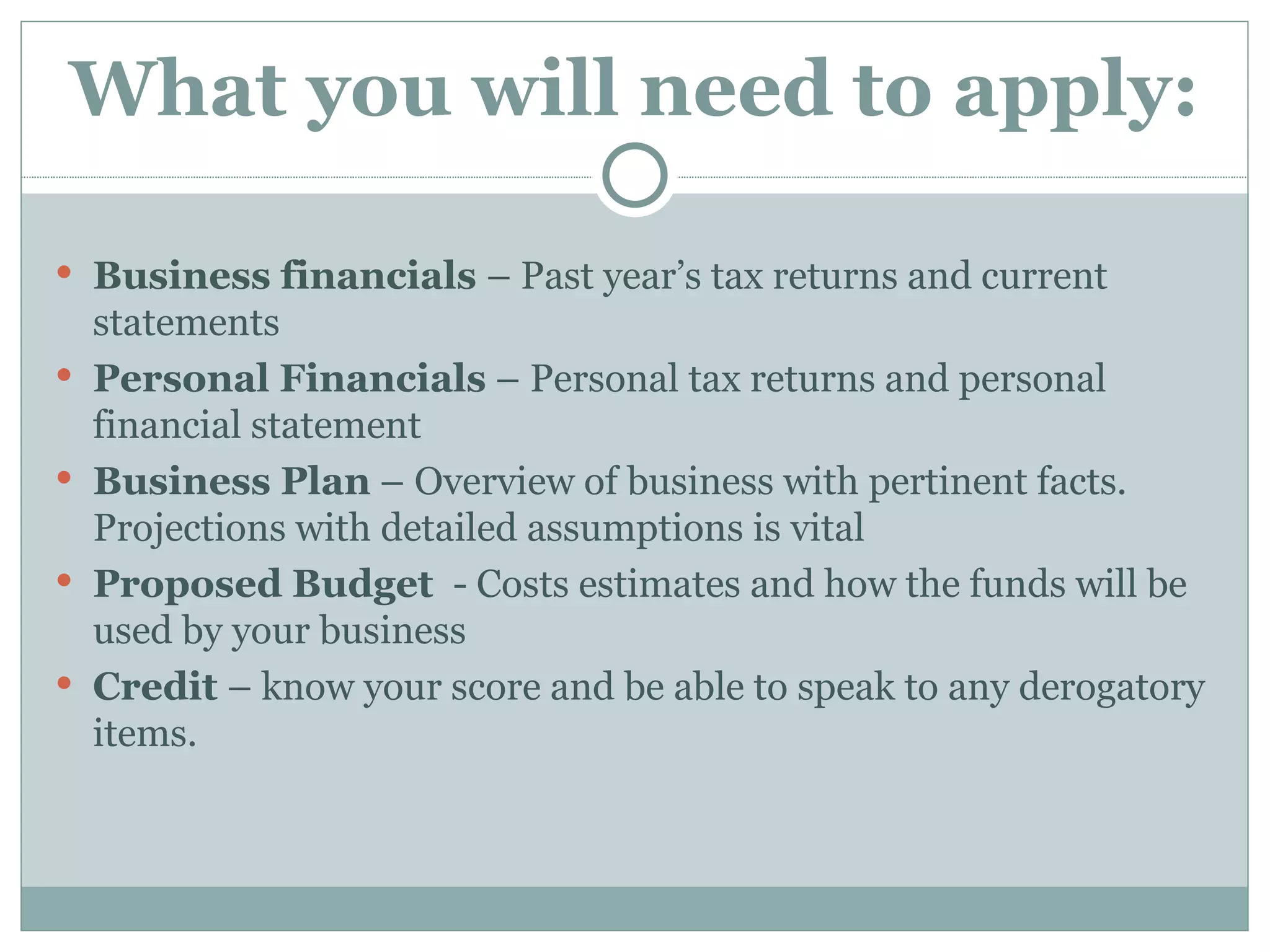

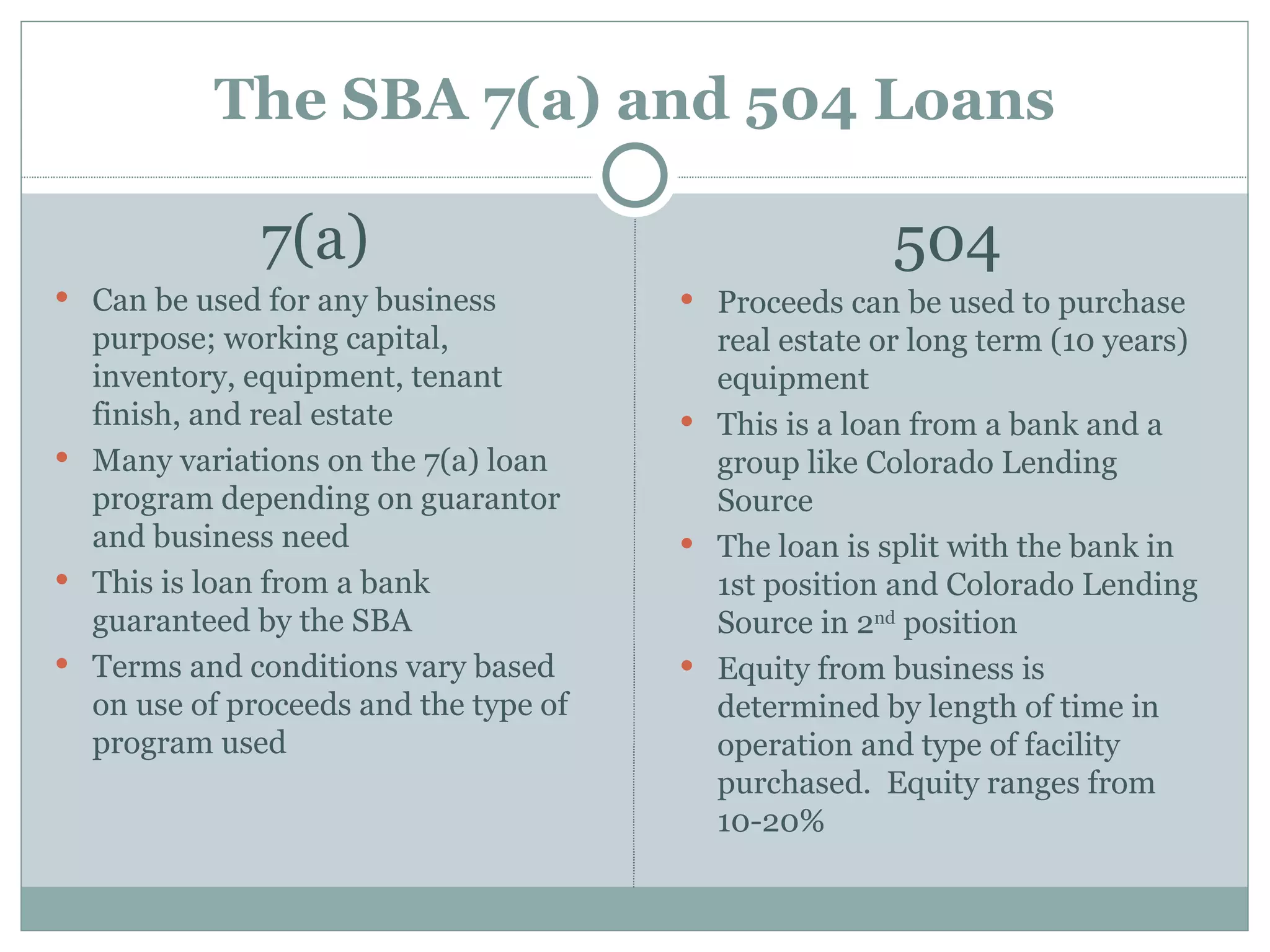

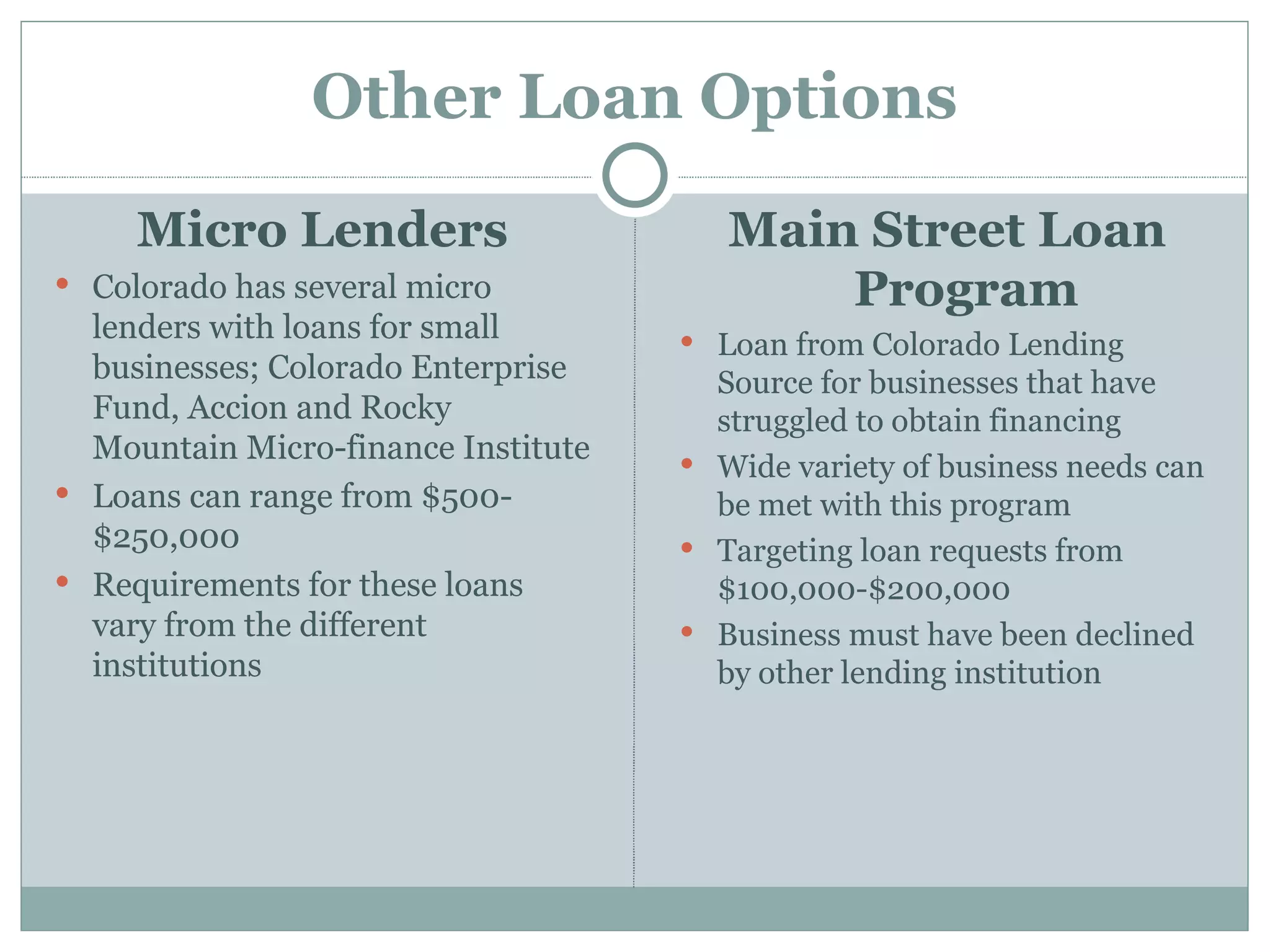

This document provides information about acquiring capital for small business growth through Colorado Lending Source. It discusses Colorado Lending Source's mission of fostering economic growth in Colorado by assisting with SBA and USDA loan programs. It outlines the 5 C's of credit that are considered in applications and the types of documentation required. It also describes the SBA 7(a) and 504 loan programs as well as other options like microloans and the Main Street loan program. Colorado Lending Source aims to inject capital into the state's economy by helping small businesses.

![SCED_SBA504_Roadmap_R2[2]](https://cdn.slidesharecdn.com/ss_thumbnails/61f461b2-f286-46c6-8777-25ad4793128a-160114164441-thumbnail.jpg?width=640&height=640&fit=bounds)