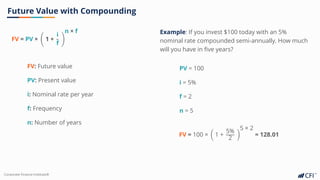

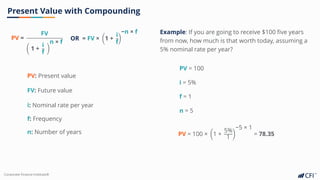

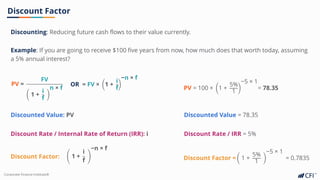

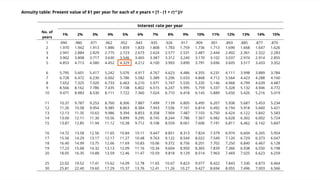

This document provides an overview of key math concepts for capital markets, including:

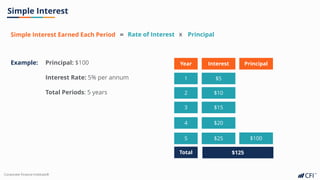

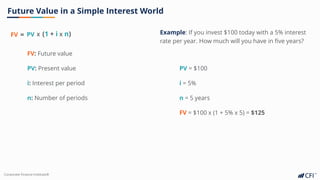

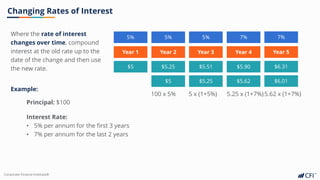

1) Calculating simple and compound interest rates, converting values to future and present value.

2) Understanding annuities and discounted cash flow analysis.

3) Examples of calculating simple and compound interest, future and present value, changing interest rates, and net present value.

4) Key terms like nominal vs effective interest rates, and discount factors.